From Turbines to Tokens

China’s energy-rich western frontier is poised to become the country’s next major AI compute hub

China’s westernmost region of Xinjiang is one of the country’s largest sources of energy. It has been exporting electricity for over fifteen years, delivering over 1 trillion kWh to 22 provinces across China, over 90% of it via three ultra-high-voltage DC transmission corridors that connect Xinjiang to power-hungry economic hubs from Anhui to Chongqing. The province is almost five times the size of Germany and generates around 6% of China’s total electricity.

A quarter of Xinjiang’s annual generation is exported east across transmission lines, capturing generation revenue but little else for the province. Much of the renewable surplus beyond that is curtailed: the transmission lines are at capacity and local demand is too low to absorb it.

Renewables account for over three-quarters of Xinjiang’s installed power capacity but only a quarter of its actual generation: wind and solar produce intermittently, and when they do, there is often nowhere for the power to go. Of what is exported east, less than a third is green.

A policy framework introduced in China’s 2026 government work report proposes capturing some of that surplus by converting electricity into AI compute. The framework is called 算电协同 (”compute-power coordination”) and Xinjiang is the first pilot region.

If all goes to plan, Xinjiang aims to reach 60 exaflops of compute capacity by the end of this year, with construction underway across four cities.

AI’s power problem

For most of the past few years, AI infrastructure headlines centered on chip supply, but that constraint is easing. Nvidia has scaled production, hyperscalers are deploying custom silicon, and China’s Huawei shipped the Ascend 950PR in Q1 2026 with roughly 2.8x the inference throughput of Nvidia’s H20 and its own domestically produced HBM. Government mandates require at least 80% domestic AI chips across the planned data center buildout.

Memory remains tight globally: SK Hynix and Samsung still control over 95% of HBM supply outside China, and Chinese memory maker CXMT’s placement on the Pentagon’s 1260H list has complicated supply chains enough that Apple is lobbying the White House for guarantees it can continue sourcing from the company. But the harder constraint is power.

In the US, new grid connections can take years. At the World Economic Forum in Davos in January, Elon Musk warned that the industry would soon be “producing more chips than we can turn on.” He put it bluntly: “The limiting factor for AI deployment is fundamentally electrical power.” He added: “except for China.”

In the US, over 2,000 GW of generation and storage capacity is waiting to connect to the grid. The median project that reached commercial operation in 2025 spent over five years in the queue. The International Energy Agency estimates that around 20% of planned data center projects could be at risk of delays. FERC responded in June with orders to fast-track data center grid connections, but new facilities may still need to bring their own power or pay for grid upgrades.

Pent-up energy

China generates more than twice as much electricity as the United States. BloombergNEF projects it will add almost six times US electricity generation capacity over the next five years. A lot of that will be renewables. In 2025 alone, China increased wind and solar capacity by over 430 GW, more than half of all global renewables additions that year.

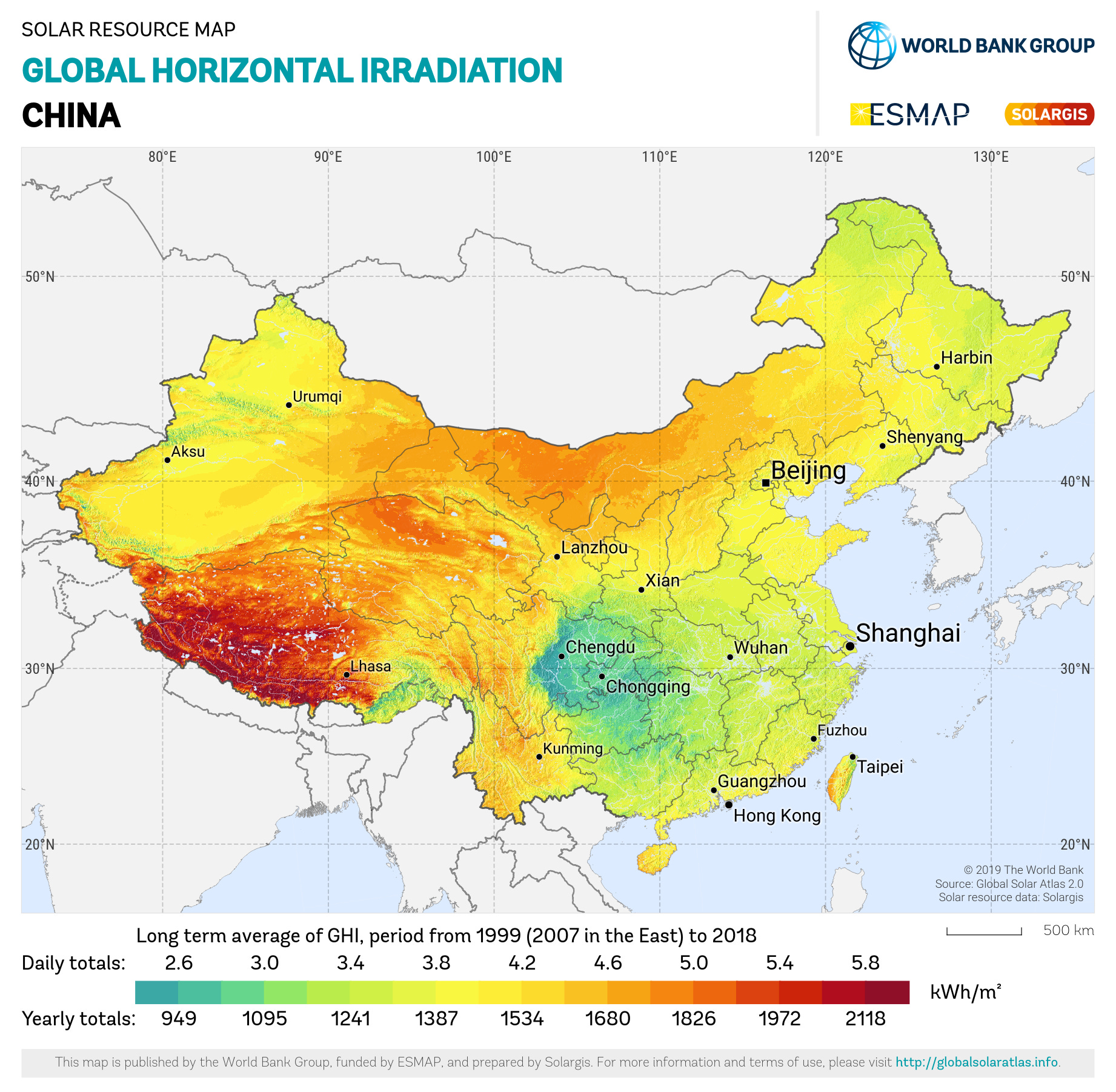

Much of this capacity is concentrated in western provinces, where land is vast, populations are sparse, and wind and solar resources are among the strongest in the country. Xinjiang’s geography makes the case: 1.66 million square kilometres of mostly arid basin and steppe, flanked by the Tianshan mountains, with some of China’s highest solar irradiance and wind corridors like Dabancheng that rank among the country’s best. There is plenty of room for turbines and panels, and plenty of wind and sun to power them. But local demand is thin.

Xinjiang crossed 100 GW of wind and solar installed capacity at the end of 2024, a first for Northwest China. Including hydro and other renewables, total clean energy capacity reached 173 GW within a total grid capacity of 219 GW by mid-2025. But the province’s ability to use all that power locally has lagged behind its ability to generate it. Conditions have improved from historical lows, but not enough: as of early 2025, only 67.6% of available renewable generation was actually used, meaning a third still went to waste.

The traditional solution has been to export the surplus east via ultra-high-voltage DC transmission lines: Hami-Zhengzhou (commissioned 2014), Changji-Guquan (2019, at 3,293 km and 12 GW capacity the world’s longest), and Hami-Chongqing (2025). Changji-Guquan alone has delivered 84 billion kWh of green electricity since commissioning, all consumed at the far end in Anhui.

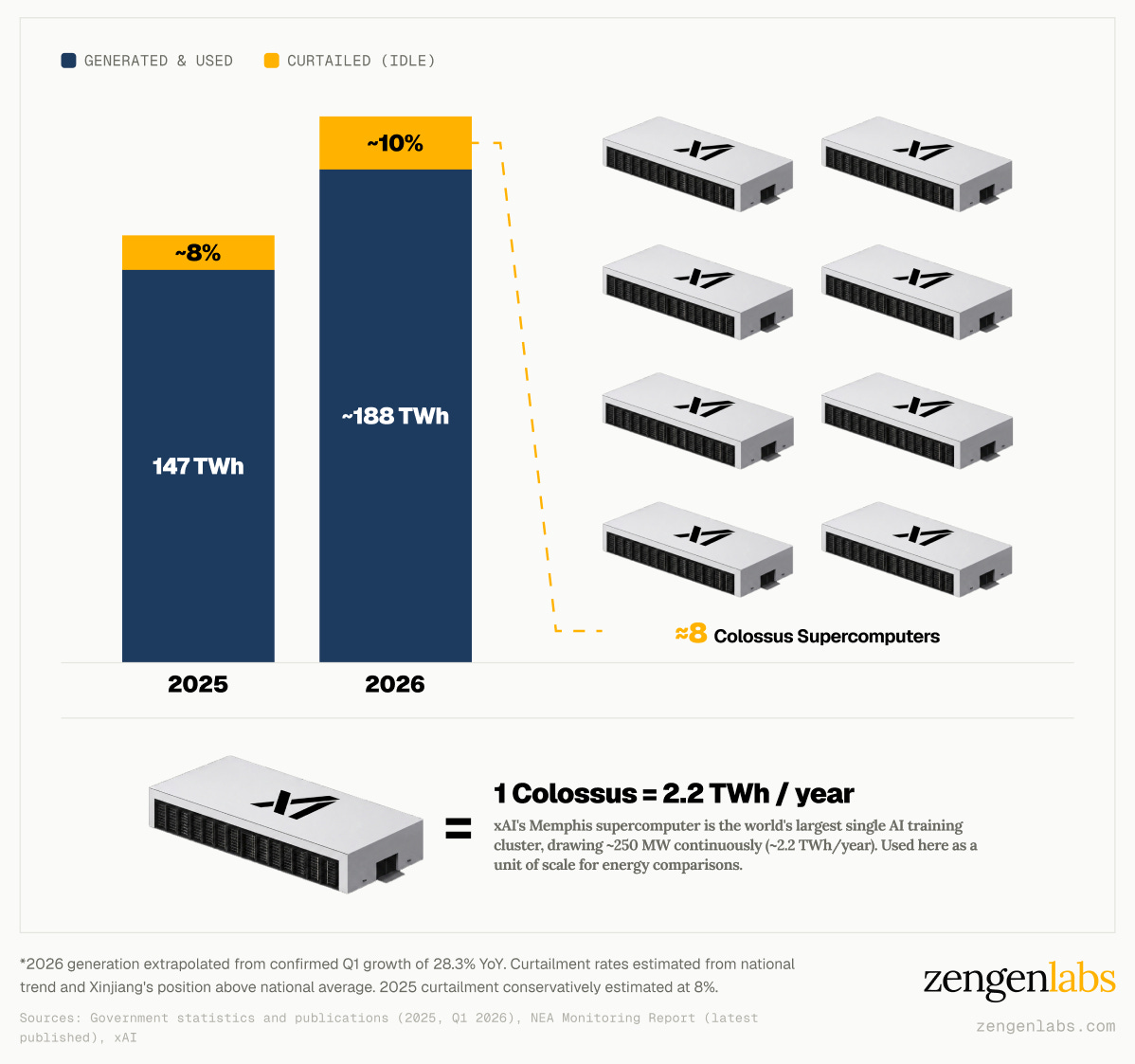

At projected 2026 curtailment rates, Xinjiang’s renewable fleet will leave untapped the equivalent of more than eight times the annual electricity consumption of Elon Musk’s xAI Colossus supercomputer.

Building compute where the power is

China’s first attempt to build compute in the west was 东数西算 (”East Data, West Compute”), launched in 2022. The program designated 8 national compute hub nodes, including Inner Mongolia, Guizhou, Gansu, and Ningxia, and built real infrastructure: 633 hyperscale and large data centers delivering 268 exaflops of national computing power by 2024.

The program built real capacity, but utilization lagged. The Oxford Institute for Energy Studies found energy savings of 4 to 12% from moving data centers west, though western centers often lacked the fiber infrastructure to serve eastern clients in real time, and the companies, talent, and customers remained concentrated on the coast. Western data center utilization rates settled at 20-30%. Over 100 data center projects have been scrapped nationally in the last 18 months, and the government imposed a moratorium on new large-scale facilities in cities where existing centers operate below 50% utilization.

Compute-power coordination, the successor framework, takes a more focused approach. Rather than trying to solve those demand-side problems directly, it asks whether energy economics alone can pull enough latency-tolerant AI workloads west. It bypasses the moratorium by granting energy-rich provinces the same policy benefits as the original 8 hub nodes based on their power resources, not administrative designation. All new data centers in hub regions must source at least 80% of their electricity from renewables, a target western provinces already meet by default.

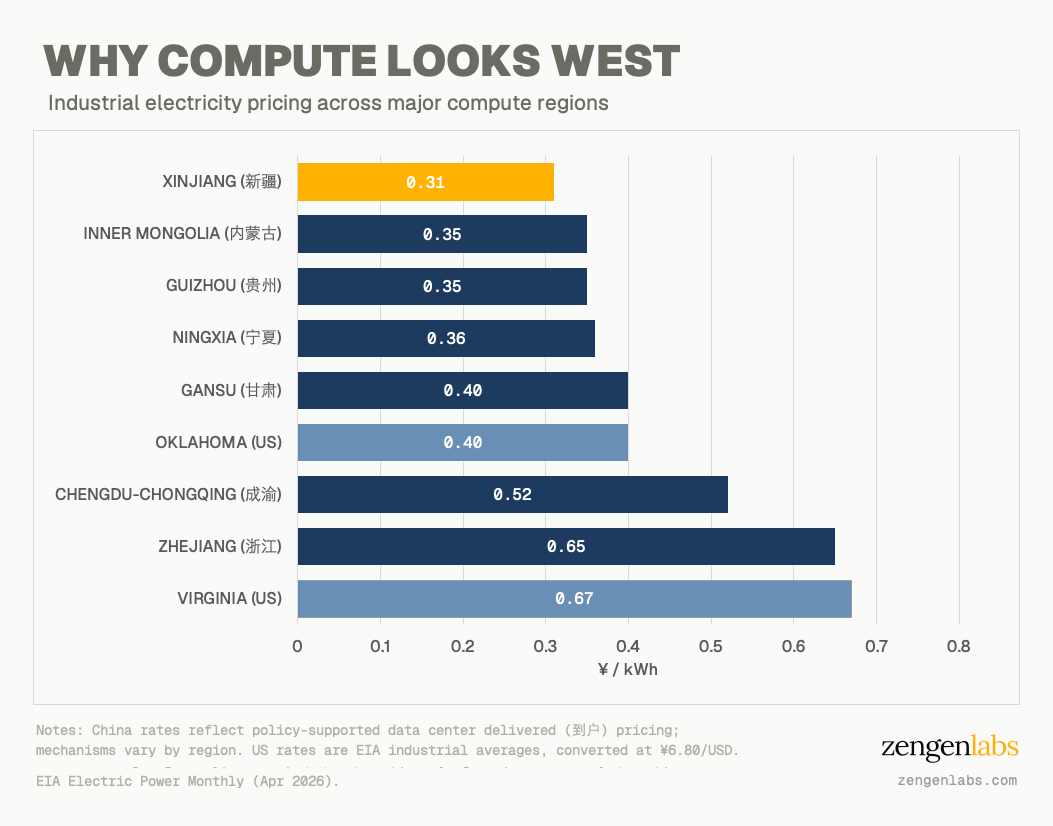

Xinjiang, which was not one of the original 8 nodes, was granted the same pilot status. It then launched what its authorities describe as China’s first multi-user 绿电直连 (”green electricity direct connection”) pricing, bypassing the traditional grid to connect power generation directly to the data center at 0.31 yuan per kWh (~$0.045/kWh). That is 0.04 to 0.07 yuan below the standard grid-delivered tariff and cheaper than Inner Mongolia’s 0.35 yuan per kWh (~$0.051/kWh), which Xinhua describes as one of the lowest among the national data center clusters.

Despite frequent claims that China has an energy cost advantage over the West, the Oxford study found that China’s industrial electricity prices are broadly comparable to those in the US. A data center in Guangdong or Jiangsu faces delivered costs of RMB 0.60-0.75 per kWh (~$0.08-0.14/kWh), near or above industrial rates in Virginia, the largest US data center market, because coastal Chinese provinces layer grid charges, capacity fees, and cross-subsidy surcharges on top of generation costs. Western green direct connection pricing at 0.31 yuan is roughly half the eastern rate, which is the real incentive for moving workloads west.

In April 2026, four central agencies led by the National Energy Administration jointly published a 29-item action plan targeting a “safe, green, economical energy guarantee system” by 2027 and “world-leading” clean energy supply for AI compute by 2030. The plan calls for million-kW-scale AI compute facilities with coordinated energy systems, multi-year green power contracts, and infrastructure REITs as a financing vehicle for compute facilities.

The NDRC is drafting a plan to spend 2 trillion yuan (~$295 billion) over 5 years on a nationwide AI data center grid, funded by sovereign debt and ultra-long special government bonds, with China Mobile and China Telecom as primary operators. The total could exceed 5 trillion yuan (~$740 billion) if power grid upgrades are included. Compute-power coordination is one of the frameworks that determines how energy-rich provinces participate in this nationwide buildout.

The demand wave

The infrastructure is being built to meet a compute demand curve that is still steepening. Deloitte estimates that global demand for AI compute is rising four to five times per year through 2030, driven primarily by inference rather than training. Inference workloads now account for roughly two-thirds of all AI compute, up from a third in 2023 and half in 2025. The market for inference-optimized chips alone is projected to exceed $50 billion in 2026. In China, computing-related electricity consumption rose from 82.4 billion kWh in 2019 to 196 billion kWh in 2025. The China Academy of Information and Communications Technology projects it could reach 500 to 700 billion kWh by 2030, up to 5.3% of total national demand.

China’s domestic AI ecosystem is generating much of that demand. Chinese platforms processed 140 trillion tokens per day in Q1 2026, a more than 1,000-fold increase from 100 billion per day in early 2024. Chinese open-source models surged from 1.2% of global usage in late 2024 to nearly 30% by mid-2025, and by June 2026 accounted for roughly 48% of token usage on OpenRouter, overtaking US models, with DeepSeek, Qwen, and Zhipu’s GLM leading the expansion.

Goldman Sachs estimates that China’s top internet firms will invest over $70 billion in data center capital expenditure in 2026, and reports that Chinese data center power demand rose 25% in 2025.

The growing dominance of inference might seem to work against Xinjiang’s case, since inference typically runs close to the end user. But much of the fastest-growing inference demand is not real-time. User-facing inference (search, voice assistants) needs to run close to the user and will stay in eastern cities. Training is less latency-sensitive but faces its own constraint: as one executive told Caixin, the datasets are so large that “companies sometimes have to physically transport hard drives” rather than transmit them east to west. Planned network infrastructure investment aims to close that bandwidth gap. But once the data arrives, training runs are exactly the kind of sustained, power-hungry workload that suits cheap western electricity. The same is true of batch processing, agent workflows, and offline industrial analytics, and these workloads are growing fastest. In January 2026, eight ministries set a target of 1,000 industrial AI agents deployed across manufacturing, logistics, and public services by 2027. Some of these, like real-time robotics control, need to run locally. But many, like logistics optimization, demand forecasting, and document processing, are batch workloads that need cheap, reliable power and a network connection, not proximity to the end user. That is the market compute-power coordination is designed to serve.

The funding landscape

In April 2025, China launched a ¥60 billion (~$8.3 billion) state-backed AI fund to invest across the full AI industrial chain, with its first-year focus on semiconductors and computing infrastructure. ByteDance’s 2026 capital expenditure alone is ¥160 billion, over half of it on AI chips. Alibaba has committed ¥380 billion over three years to cloud and AI hardware infrastructure.

Below the hyperscalers, venture capital is filling the infrastructure stack. Some notable raises this year across the energy and cooling layers of AI compute:

Qingqi Power (清启动力): micro gas turbines for distributed data center power. Pre-A round, nearly ¥100 million (~$14 million), ¥500 million valuation. Facilities that cannot wait on the grid use on-site turbines to generate power where the connection has not yet arrived.

Xinhan Intelligence (芯寒智能): cooling systems for AI compute clusters. Pre-A round, hundreds of millions of yuan, ¥1.5 billion valuation. AI accelerators run hot and pack tightly, and at cluster scale the heat load outstrips what air cooling can handle. Cooling also sets PUE, the main lever on a facility’s operating cost.

Afalight (埃尔法光电): co-packaged optics. D round (sixth total), ~¥100 million, ¥1.2 billion valuation. Supplies a 2.4 Tbps optical engine to Alibaba’s AI data centers. As clusters scale, the copper links between racks and the network become the bottleneck on data movement, and co-packaged optics moves the transceiver onto the switch package to push interconnect bandwidth past that limit.

MetaPWR (沛塬电子): power modules for AI compute. Strategic round, undisclosed amount, ¥500 million valuation. AI racks pull very high current at low voltage, and the rack’s power conversion stage has to deliver that cleanly and reliably. Generic modules are not rated for the load profile.

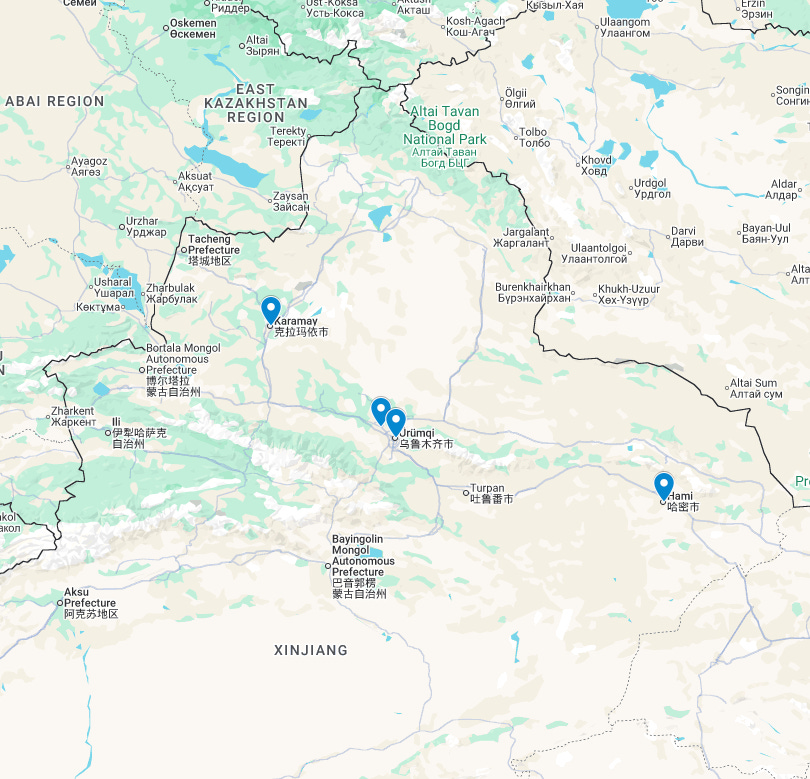

Four cities, one value chain

Four cities are dividing the work: Karamay runs the most efficient facilities, Changji is building new capacity with major tech partners, Hami dispatches compute to Chongqing, and Urumqi connects westward to Central Asia.

1. Karamay (克拉玛依) has some of the most energy-efficient data center infrastructure in China. Carbon and Network Tech runs facilities with a PUE under 1.1 (PUE measures how much energy goes to compute vs. cooling and overhead; a perfect score is 1.0, and typical facilities run 1.3-1.5), with cooling and overhead energy one-fifth that of a conventional data center thanks to liquid cooling and Xinjiang’s cold, dry climate. The company has used 100% green power via green electricity certificates since 2024 and was listed on the 2025 National Green Compute Facilities roster. Karamay dispatches compute to Shanghai under a cross-regional framework.

2. Changji (昌吉) broke ground in May 2026 on a green direct-connect photovoltaic project paired with a China Unicom 16,000P intelligent compute infrastructure build at the Xinjiang Information Industry Park. Alibaba, ByteDance, and Zhipu have all reached cooperation agreements, with scheduled completion in November 2026.

3. Hami (哈密) has been designated by the National Data Bureau as an implementation city for both the Xinjiang-to-Chongqing compute corridor and compute-power coordination. A dedicated all-optical network link delivers under 20 ms one-way latency to Chongqing across 4,000 km, with 20,000P of compute already operational and a target of 40,000P by year-end.

4. Urumqi (乌鲁木齐) is building a national-level internet backbone direct connection point alongside a BRICS digital industry cooperation network city node, positioning itself as a compute hub serving Central Asia and Europe. Xinjiang borders Kazakhstan, Kyrgyzstan, Tajikistan, Pakistan, and Mongolia, and has more than 20 cross-border international fiber cables connecting to those neighbors, recently upgraded to 1.2 terabits (China-Kazakhstan) and 800 gigabits (China-Pakistan). The provincial government describes its cross-border compute services as “算力出海” (”compute going overseas”). So far, the only confirmed services crossing these borders are satellite remote sensing and smart agriculture from Xinjiang’s Space-Air-Ground Integration Lab. The fiber infrastructure exists; commercial AI compute demand from Central Asian markets has yet to materialize. Eight intelligent compute center projects are under construction, and companies including Beijing Wanjie Data and Hefei-based Leinao have established operations. The Xinjiang Daily describes Leinao’s facility here as the first compute center using domestically produced chips. Leinao’s Bitahub platform aggregates self-built and external compute resources and reports a utilization rate above 90%, but that is a platform-level figure, the result of a marketplace that resells compute across multiple facilities. Facility-level utilization in western hubs remains at 20-30%. Whether a platform model can close that gap at scale beyond a single marketplace is untested.

Electricity to compute to tokens

Jin Qian, president of Carbon and Network Tech in Karamay, told the Xinjiang Daily: “Xinjiang is thinking about how to convert electricity into compute, compute into tokens, and serve the world via the internet.”

China does not need to export chips, models, or hardware to serve AI demand beyond its borders. It can deliver tokens over fiber, keeping the infrastructure, energy, and jobs domestic. Each step retains more value locally than the last: raw electricity captures generation revenue, compute adds infrastructure and operations, tokens add the service layer. Geopolitical and data-sovereignty constraints will shape which markets those tokens can realistically reach, but the economic logic of the conversion chain holds regardless.

The electricity-to-tokens framing has taken hold in other compute hubs too. Inner Mongolia’s Ulanqab, just over 200 km from Beijing with 4.2 ms fiber latency, has branded itself China’s “Token之都” (Token Capital) under a three-year action plan (2026-2028), with over 5 million standard server racks signed and 165,000P of running compute. But Ulanqab’s success leans on proximity to Beijing. Xinjiang’s pitch is different: the cheapest green power in the country, direct-connect pricing that undercuts even Inner Mongolia, and cross-border fiber to Central Asia that no eastern hub can match.

What has to go right

SMIC’s co-CEO Zhao Haijun warned on the company’s Q4 earnings call that rushed AI data center capacity could sit idle, describing the pace as “10 years of capacity crammed into two.”

Caixin, citing expert sources, describes compute-power coordination as being in an “early exploration period,” and draws a technical distinction between 电量 (”electricity volume”), the total energy available, and 电力 (”electrical power”), managing instantaneous demand. Xinjiang has plenty of 电量, but the real challenge is 电力. AI training clusters draw power in sharp, irregular spikes that solar and wind cannot match on demand. The green direct connection model that bypasses the grid also bypasses this buffer, so facilities need either substantial battery storage or a robust grid fallback. Some are already building this: a State Power Investment Corporation facility in Xinjiang operates entirely off-grid with on-site solar, wind, and battery storage, and CATL committed over $1.5 billion to data center energy infrastructure in two months, including $577 million into data center power supplier Zhongheng Electric in April and up to $942 million into data center operator VNET Group in May.

Data centers still account for only 1.68% of China’s total electricity consumption, projected to reach 3% by 2030, a narrower scope than CAICT’s broader “computing-related” estimate of up to 5.3%, which includes telecom and edge infrastructure. Compute-power coordination will not solve the curtailment problem in volume terms. The case rests on value density: a kilowatt-hour converted into AI tokens captures far more economic value than one exported as raw electricity, even if the total kilowatt-hours consumed remain a sliver of the surplus.

The timeline mismatch compounds the challenge: large computing centers can be built in 8 to 24 months, but traditional power substations require 3 to 5 years for planning, approval, and construction. Green direct connection lets data centers start operating before the substation arrives, but the grid fallback they will eventually need still takes 3 to 5 years to build.

The Xinjiang Daily itself acknowledges the challenges: “算力基础设施投资大、回报周期长” (”compute infrastructure investment is large, payback period is long”), along with the need for better cross-regional networks and talent.

Conclusion

The question this framework has to answer is the same one East Data, West Compute could not: whether workloads will actually move. Compute-power coordination addresses the cost side of that equation with 0.31 yuan/kWh green direct-connect pricing and equivalent hub-node status. What it does not address is the commercial gravity of the eastern seaboard, the dense concentration of developers, customers, and corporate headquarters that resisted the first wave of westward migration.

If the framework succeeds, it establishes a model with implications well beyond Xinjiang: that energy-rich, compute-poor regions can compete for AI workloads on electricity price rather than proximity, provided they target latency-tolerant workloads, whether training or batch inference, rather than real-time services. That would reframe western China’s renewable surplus as upstream infrastructure for a national or even global AI services layer. The energy still reaches demand, but as tokens over fiber rather than electrons over high-voltage lines, and the bottleneck shifts from the rigid capacity of a transmission corridor to the elasticity of a network. At the token layer, remoteness stops being the obstacle and becomes the advantage: stranded power converted into tokens, carried over fiber to markets the grid was never built to reach.