The China Round — April 10, 2026

Fusion Bets, Brain Implants, and the Ma-Lei Signal

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

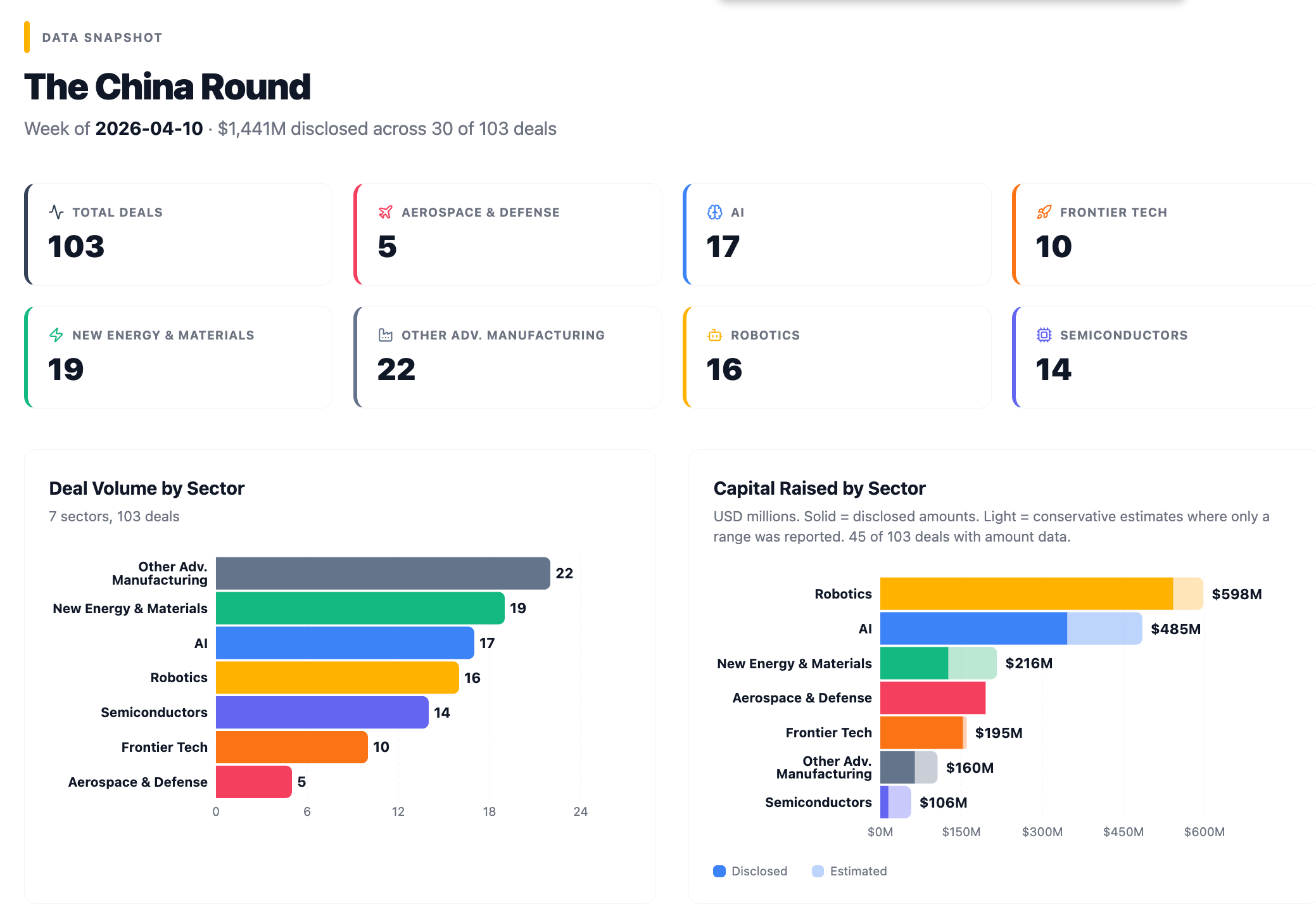

Where the Money Went

103 funding events across seven sectors. Over $1.4 billion (~¥10.1B) in disclosed capital, with the real total significantly higher given that 50+ deals went undisclosed. Alibaba led a ¥2 billion (~$293M) strategic round into video generation platform Shengshu (Vidu). Nova Fusion raised ¥700 million (~$97M) at angel+ stage for nuclear fusion, on top of a ¥500 million angel round last year. Jack Ma and Lei Jun made their first known co-investment in Spirit AI, a humanoid robot company now valued at ¥15 billion (~$2.1B).

Chart note: Light-shaded bars represent conservative estimates where only a vague range (e.g., “数亿人民币” / “hundreds of millions”) was reported.

🤖 Robotics (16 deals)

Fewer deals than last week’s 27, but the individual rounds run larger. Spirit AI (千寻智能) pulled in ¥1 billion (~$139M) for an A+ round, part of two rounds totalling ¥3 billion (~$417M) within 30 days. ENGINEAI (众擎机器人) closed $200 million (~¥1.44B) with Luxshare as strategic co-lead. D-Robotics (地瓜机器人) raised $150 million (~¥1.08B) for its robot OS platform, a Horizon Robotics spinout building the infrastructure layer for humanoid development. The early-stage pipeline remains active: five angel/seed rounds, including a Li Auto AI team spinout (斜跃智能) founded just two months ago.

🧠 AI (17 deals)

Alibaba led a ¥2 billion (~$293 million) strategic round into Shengshu Technology (生数科技), maker of the Vidu video generation platform. That single deal accounts for most of the sector’s disclosed capital. The distribution otherwise skews early: Synapx (章鱼动力), founded December 2025 by four ex-Horizon Robotics executives, raised hundreds of millions at a ¥3 billion (~$417M) angel valuation for “physical AGI.” Red Bear AI (红熊AI) closed Series A with ¥135 million (~$19M) in revenue and 13% margins, one of the few profitable Chinese AI agent companies at this stage. ModelBest (面壁智能) hit E-round unicorn status for edge-side foundation models.

🔬 Semiconductors (14 deals)

Deals span analog and mixed-signal IC, MEMS sensors, power semiconductors, and storage chips. Most rounds are Series A or earlier with government guidance fund participation, consistent with the ongoing self-sufficiency push. Lingdong Jiaxin (灵动佳芯) closed an A round backed by SMIC Capital (中芯聚源) and others.

⚡ New Energy & Materials (19 deals)

Zhide Battery (致德新能源) raised ¥600 million (~$83M) at Series E for silicon-carbon anode materials, with CATL as an existing investor. JNION (珈钠能源) appeared for the second consecutive week, raising an A+ round for sodium-ion cathode materials with EVE Energy (亿纬锂能) backing. New materials companies (安迈特科技 with Toray strategic, 环西汀新材, 方硕材料, 启烯材料) accounted for roughly a third of the sub-sector.

🚀 Aerospace & Defense (5 deals)

Spacety (天仪研究院) raised ¥1.3 billion (~$181M) in a pre-IPO round for its 28-satellite SAR constellation, the sub-sector’s standout. Dezhihangchuang (德知航创) closed an A+ round with Sichuan provincial defense-industry funds. Huanyuhaoxing (寰宇昊行) and Gongda Satellite (工大卫星) filled out a quiet but steady week for space and defense.

⚙️ Other Adv. Manufacturing (22 deals)

Optoelectronics and photonics accounted for roughly ten deals, including Aochuang Photonics (奥创光子) at Series D and Saifulesi (赛富乐斯) raising ¥300 million (~$42M) for micro-LED. Three deals covered the lithium niobate photonics value chain from substrate to chip design. The remainder spans industrial automation, precision control, smart manufacturing equipment, and a tail of companies where names alone do not reveal the sub-sector.

💡 Frontier Tech (10 deals)

Ten deals, with capital concentrated in a few large rounds. Nova Fusion (诺瓦聚变) leads the category with a ¥700 million (~$97M) angel+ round for FRC nuclear fusion targeting AI data center power. Four to five brain-computer interface deals (应和脑科学, 聚芯医疗, 脑次元, 曦嘉医疗, 瓦博科技) landed in the same week, following BCI’s first appearance in the Government Work Report. Juxin Medical (聚芯医疗) closed a ¥200 million (~$28M) C round for endovascular BCI.

Spotlight

Spirit AI (千寻智能)

A+ Round, ¥1 billion (~$139M), valuation ¥15 billion (~$2.1B)

Full-stack humanoid robotics.

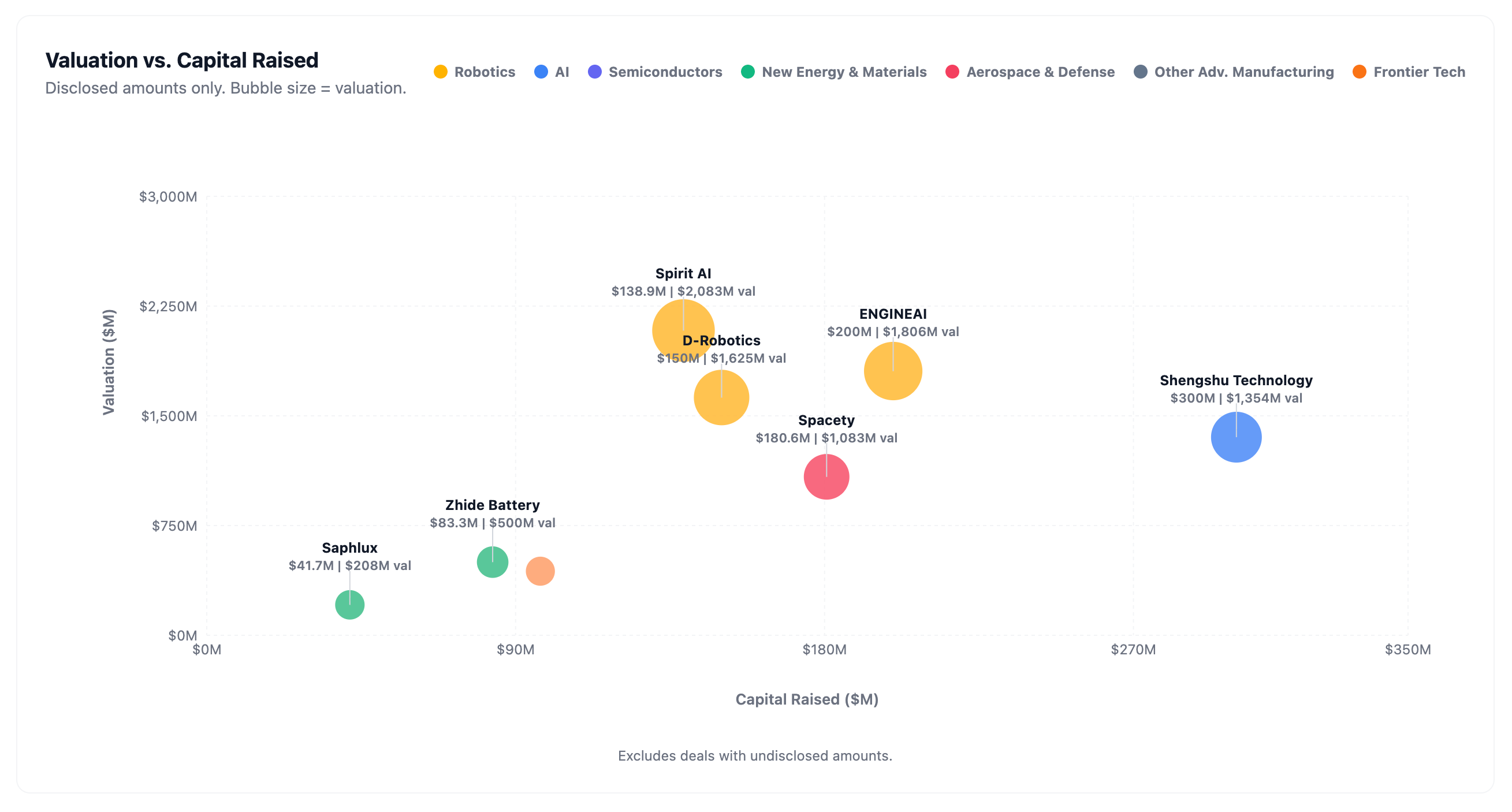

Spirit AI builds humanoid robots for manufacturing deployment. CEO Han Fengtao (韩峰涛) previously co-founded and served as CTO of Rokae Robotics (珞石机器人), where he oversaw delivery of 20,000+ industrial robots. Chief Scientist Gao Yang (高阳) is a Tsinghua assistant professor with a Berkeley PhD, supervised by Pieter Abbeel. Their Moz1 robot (26 degrees of freedom, full-body force control) is already deployed on CATL’s battery pack production line at the Zhongzhou base, running connector insertion at a 99%+ success rate and 3x human throughput. Bairui Capital (柏睿资本), founded by CATL co-founder Li Ping, invested at the angel stage, and the production-floor deployment followed.

Spirit raised ¥3 billion (~$417M) across two rounds in roughly 30 days in early 2026, on top of seed and angel rounds that had already brought total funding past ¥4 billion (~$556M). This A+ round was co-led by Shunwei Capital (顺为资本, Xiaomi founder & CEO Lei Jun’s fund) and Yunfeng Fund (云锋基金, Jack Ma’s fund), their first known co-investment in the embodied AI sector. Dachen Venture Capital (达晨财智), Turing Fund (图灵基金), and others joined. The February round had brought in Chaos Investment (混沌投资, hedge fund manager Ge Weidong), Sequoia China, and TCL Ventures.

In January 2026, Spirit open-sourced its VLA foundation model Spirit v1.5, which ranked first on the RoboChallenge global embodied AI benchmark, surpassing Pi0.5. The company claims its integrated force-control joints have 15% higher power density than Tesla Optimus, though no third party has independently verified this.

The company was founded in January 2024 and reached a ¥15 billion (~$2.1B) valuation within fourteen months.

Shunwei Capital (顺为资本, co-lead), Yunfeng Fund (云锋基金, co-lead), Dachen Venture Capital (达晨财智), Turing Fund (图灵基金), Xinding Capital (新鼎资本), Yinhe Yuanhui (银河源汇), and others. Gaohu Capital (高鹄资本) and Gengxin Capital (庚辛资本) as financial advisors.

Nova Fusion (诺瓦聚变)

Angel+ Round, ¥700 million (~$97M), valuation ¥3.15 billion (~$438M)

FRC nuclear fusion for AI data center power.

Nova Fusion is building compact modular fusion reactors using field-reversed configuration (FRC) magnetic compression, a linear (not toroidal) design that requires smaller magnetic fields and produces more compact systems than traditional tokamaks. The target application is AI data center power, where training cluster power demand is outpacing grid capacity. The company’s roadmap runs from 100 million degree ion temperature through Q>1 (net energy gain) to 50MW commercial output.

Founder Guo Houyang (郭后扬) co-founded Energy Singularity (能量奇点), China’s other prominent fusion startup, and served as its CTO before departing to start Nova Fusion in April 2025. He holds a PhD from Université du Québec (1993) and has over 30 years in magnetic confinement fusion research across Canadian and US institutions. He currently serves as Deputy Director of Shanghai’s Future Industry Advanced Nuclear Energy Expert Committee. At Energy Singularity, he built the team that produced the Honghuang 70, a high-temperature superconducting tokamak. Nova Fusion’s FRC approach diverges from the tokamak design he worked on previously.

¥700 million (~$97M) at angel+ stage, on top of a ¥500 million (~$69M) angel round closed in August 2025, bringing total funding past ¥1.2 billion (~$167M) for a company founded just over a year ago. ENN Fusion (星环聚能) raised ¥1 billion (~$139M) in a January 2026 A round using a different magnetic reconnection approach, taking the sector’s single-round record. Chinese private fusion is entering what 21st Century Business Herald called “密集砸钱时代” (”intensive money-throwing era”), with policy tailwinds from both the 14th and 15th Five-Year Plans including commercial fusion in national industrial planning.

Meituan Longzhu (美团龙珠), Hillhouse Capital (高瓴资本), Shangqi Capital (尚颀资本), Huichuan Venture Capital (汇川产投), Jiukun Ventures (九坤创投), with Legend Capital (君联资本), Gaorong Capital (高榕创投), and Lightspeed China (光合创投) following on from the angel round. Per ITJuzi, Guangzhou Industrial Investment (广州产投) and Xiamen C&D (厦门建发) also participated.

Spacety (天仪研究院)

Strategic Round, ¥1.3 billion (~$181M) cumulative, valuation ¥7.8 billion (~$1.08B)

Commercial SAR satellite constellation.

Spacety operates China’s first commercial SAR (synthetic aperture radar) satellite constellation, with 28 satellites in orbit and a planned build-out to 120. The constellation targets 0.5-meter resolution imagery with an average revisit cycle of 11 minutes for any point between 60°N and 60°S. The company’s millimeter-level surface deformation monitoring serves construction, transportation, power grid, and mining sectors.

Founded in 2015 in Changsha, Spacety has deployed its SAR data in 62 disaster response operations across Bangladesh, Indonesia, Turkey, and other countries, making it one of the few Chinese commercial space companies with meaningful international operations. The company started IPO preparation in February 2026, filing for A-share listing.

This latest strategic round brings cumulative funding to ¥1.3 billion (~$181M) across multiple rounds, with a reported valuation of ¥7.8 billion (~$1.08B). The capital will fund scaled satellite manufacturing, commercialization of data services, and building an integrated develop-manage-use chain.

Bohua Capital (博华资本), Puhua Capital (普华资本), Turing Capital (图灵创投), Guoxin Guozheng (国新国证), Xiangjiang State Investment (湘江国投), and others. Yibai Capital (义柏资本) as financial advisor.

ENGINEAI (众擎机器人)

Series B, $200 million (~¥1.44B), valuation ¥13 billion (~$1.8B)

Full-stack humanoid robots at consumer price points.

ENGINEAI ships three humanoid robot models. The SE01 (170cm, 55kg, 32 degrees of freedom, 330 N·m max joint torque, 2m/s walking speed) opened for global sales in December 2024 at $20,000-30,000. The PM01 is lighter and cheaper, currently listed at $13,700, and gained attention for what the company says was the first humanoid front flip, a stunt covered by New Atlas, Interesting Engineering, and other Western tech outlets. The T800 (173cm, 75kg, 450 N·m peak torque, NVIDIA Jetson Thor, 2,000 TOPS), unveiled at CES 2026 at a $25,000 starting price, targets heavy industrial deployment with first shipments planned for mid-2026. Founded October 2023 in Shenzhen by Zhao Tongyang (赵同阳).

The PM01 at $13,700 sits near Unitree’s G1 base model ($13,500) and well below current pricing estimates for Western humanoids like Figure AI’s commercial deployments. Luxshare Precision (立讯精密), which assembles Apple’s iPhones and AirPods, co-led this round as a strategic investor, bringing the same supply chain engineering that drove consumer electronics cost curves downward into humanoid manufacturing. Henan Investment Group (河南投资集团) co-led through its Huirong Fund (汇融基金). Cornerstone Capital (基石资本), Longgang Jinkong (龙岗金控), Duolun Technology (多伦科技), and others participated.

The company has described its commercialization strategy as deliberately slow, prioritizing technical depth over a rush to scale, though $200 million (~¥1.44B) of fresh capital and Luxshare on the cap table may test that approach.

Henan Investment Group / Huirong Fund (河南投资集团/汇融基金, co-lead), Luxshare Precision (立讯精密, co-lead/strategic), Cornerstone Capital (基石资本), and others.

Shengshu Technology / Vidu (生数科技)

Strategic Round, ¥2 billion (~$293M)

Video generation AI.

Shengshu Technology builds Vidu, a video generation platform built on U-ViT (Universal Vision Transformer), an architecture the team published in September 2022 that predates OpenAI’s DiT architecture used in Sora. Chief Scientist Zhu Jun (朱军) is a Tsinghua University computer science professor who co-launched the company in partnership with the university’s AI Research Institute. The platform hit 10 million users within 100 days of its July 2024 global launch. Vidu Q3 Pro currently sits 7th on the Artificial Analysis text-to-video leaderboard, behind ByteDance Seed, Kling, and several others. Vidu 2.0 (January 2025) generates 4-second clips in under 10 seconds at roughly $0.04 per second, 55% below the industry average. The platform has generated over 100 million video clips to date.

This is Alibaba’s second AI video bet, following a $60 million+ (~¥432M+) round into PixVerse in January. The Shengshu investment sits within Alibaba’s ¥380 billion ($53 billion) three-year AI and cloud infrastructure commitment. Alibaba Cloud revenue grew 26% to a three-year high, with AI product revenue posting triple-digit growth for eight consecutive quarters. The company frames its interest in Shengshu around “general world models” for sensory simulation toward AGI in physical environments, a broader bet than video content creation alone.

Alibaba Cloud (阿里巴巴, lead), Andon Haitang (安东海棠), China Internet Investment Fund (中国互联网投资基金), TAL Education Group (好未来), and Luminous Ventures.

Also on the Radar

Red Bear AI (红熊AI) — Series A, ¥210 million (~$29M), ¥1.5 billion (~$208M) valuation. AI agent interactive platform with episodic memory architecture. ¥135 million (~$19M) in revenue at 13% net margin, making it one of the few profitable Chinese AI agent companies at this stage. CEO Wen De (ex-Alibaba, Fosun). Plans to expand internationally. Huayu Venture Capital (华禹创投, lead), Jiaming Haochun (嘉铭浩春), Jiawo Capital (稼沃资本), and others.

AWOL Vision (海高特) — Series B, close to ¥100 million (~$14M), ¥500 million (~$69M) valuation. Ultra-short-throw laser projectors. Two Kickstarter campaigns exceeding $10 million each under the Valerion brand. Miami office, US retail distribution, $1,899-5,999 price range. Western go-to-market further developed than any other company in this week’s data. Tiantang Silicon Valley (天堂硅谷), Huichang Technology (会畅科技), and Jinpeng Jia (金鹏佳).

Mizzen Insight (觅深科技) — Angel, close to $10 million (~¥72M), ¥260 million (~$36M) valuation. AI-powered user research platform that automates deep-dive customer interviews. 300 customers in four months, already deployed with overseas e-commerce and EV companies. Founded by Dr. Sun Keqiang (Tsinghua CS, CityU HK PhD). Sequoia Seed Fund (红杉种子基金, lead), Dachen Venture Capital (达晨财智), Jiacheng Capital (嘉程资本), and others.

ModelBest (面壁智能) — Series E, hundreds of millions of RMB, ¥9.5 billion (~$1.32B) valuation. Edge-side general foundation models. Tsinghua-origin unicorn partnered with China Telecom for AIPC deployment. Shenzhen Capital Group (深创投, co-lead), Huichuan Venture Capital (汇川产投, co-lead), and others. Huaxing Securities (华兴证券) as FA.

Synapx (章鱼动力) — Angel, hundreds of millions of RMB, ¥3 billion (~$417M) valuation. “Physical AGI” targeting the “Physical AI Turing Test.” Founded December 2025 by four ex-Horizon Robotics executives: Du Dalong (ex-CTO Jianzhi), Liang Zhujin (ex-VP), Pan Yangjia (ex-CFO), Fan Qingyuan (ex-VP). K3 Ventures (lead), Shunwei Capital (顺为资本), Xiaomi Group (小米集团), and others.

Holistic (霍里思特) — Series C, ¥200 million (~$28M), ¥1 billion (~$139M) valuation. X-ray AI ore sorting with 30%+ domestic market share across five ore types. All-Tsinghua founding team, founded 2010. China Merchants Capital (招商局资本, lead), Beichuang Investment (北创投), and others.

Enlight Medical (应和脑科学) — Strategic, undisclosed amount, ¥500 million (~$69M) valuation. Full proprietary neuromodulation and BCI platform covering electrodes, chips, signal decoding, and algorithms. Spun out from Yingmai Medical. Eli Lilly Asia Ventures reportedly co-led (per press; ITJuzi lists only Jiangxia Sci-Tech Investment (江夏科投)).

LEAPTIC (光子跃迁) — Angel, undisclosed. Corporate spinout from Dreame Technology (追觅科技, $2.8 billion valuation), building an 8K AI action camera at 55 grams, shipping at $440 versus GoPro at $400. Won a GMarks Design Award in Japan. Over 100 staff, already shipping. Sky Workshop Ventures (天空工场创投).

JNION (珈钠能源) — Series A+, hundreds of millions of RMB, ¥1.5 billion (~$208M) valuation. Sodium-ion battery cathode materials. Built the world’s first 10,000-tonne polyanionic cathode production line (December 2024). Founded by Prof. Cao Yuliang (Wuhan University). Shenzhen Capital (深圳资本) and EVE Energy (亿纬锂能).

Zhide Battery (致德新能源) — Series E, ¥600 million (~$83M), ¥3.6 billion (~$500M) valuation. Silicon-carbon anode materials for lithium batteries, solving the silicon swelling problem through carbon coating. CATL is an existing investor. Chaoxi Capital (朝希资本, co-lead), Dachen Venture Capital (达晨财智, co-lead), and others.

The Bigger Picture

Five BCI deals in one week

Brain-computer interface appeared in the 2026 NPC Government Work Report (政府工作报告) for the first time, listed alongside quantum technology and embodied intelligence as a priority future industry. Five neuro/BCI deals followed in the same week.

The deals cover different layers of the stack. Juxin Medical (聚芯医疗) raised ¥200 million (~$28M) at Series C for minimally invasive endovascular BCI and neuro-intervention devices, with Zhongshan Jinkong (中山金控) leading and Guangdong Finance (粤财创投) participating. Enlight Medical (应和脑科学) took a strategic round at a ¥500 million (~$69M) valuation for a full proprietary neuromodulation platform covering electrodes, chips, signal decoding, and algorithms, reportedly with Eli Lilly Asia Ventures involvement alongside Jiangxia Sci-Tech Investment (江夏科投). Xijia Medical (曦嘉医疗) raised an angel round for brain connectomics AI, with its NuraSurgical platform deployed in 120+ overseas hospitals across 10,000+ neurosurgery cases. Brain Dimension (脑次元) closed a ¥60 million (~$8.3M) strategic round for brain-science health services. WABO Technology (瓦博科技) took seed funding for consumer non-invasive BCI wearables.

The five deals this week follow a regulatory milestone: in March, Neuracle Medical Technology (博睿康) secured China’s first-ever approval for an implantable BCI system, a coin-sized wireless device placed on the brain’s surface to restore hand motor function in spinal cord injury patients. Per the National Medical Products Administration, it was the first globally approved invasive BCI available as a commercial product. Separately, StairMed (阶梯医疗) raised ¥500 million (~$69M) led by Alibaba in March, bringing its past-year total past ¥1.1 billion (~$153M), with plans to implant ~40 patients by end of 2026 — approaching Neuralink’s 21 reported trial cases.

In China’s industrial development pattern, explicit inclusion in the Government Work Report signals state and private capital to move. New energy vehicles, AI, and commercial spaceflight all followed the same sequence: government endorsement, then a capital surge within 12-18 months. BCI now has both the policy endorsement and the first commercial product approval. The Eli Lilly involvement in Enlight Medical, if confirmed, adds an international pharma dimension: a global company optioning access to Chinese neuromodulation through a minority stake.

Lithium niobate: The crystal that AI data centers will need next

AI training clusters are running into a physical bottleneck: the cables connecting GPUs inside data centers can’t move data fast enough. The current solution is silicon-based optical components that convert electrical signals to light and back. But as connection speeds push past 1.6 terabits per second, silicon hits its physical limits. The leading replacement is a crystal called lithium niobate, which can switch light signals roughly 10x faster. Whoever controls the supply chain for lithium niobate photonics controls a chokepoint in next-generation AI infrastructure.

Three deals this week cover that entire supply chain in China, from raw material to finished chip. Weima Semiconductor Materials (威迈芯材) raised a strategic round for the chemical precursors used to pattern photonic circuits — the company operates two production plants in Korea and claims to be China’s first commercial producer in this category. New Silicon Convergence (新硅聚合), spun out of the Chinese Academy of Sciences, raised a strategic round backed by Shenzhen Capital (深创投) and the National Innovation Fund (国新科创基金) for the crystal wafers themselves — the physical substrate that chips are built on, already sold to 200+ customers globally. Precision Photonics Core (极刻光核) closed a B+ round for the finished product: photonic chips that go into data center interconnects. Founder Liang Hanxiao holds a PhD from the University of Rochester.

Raw materials, wafer substrates, and chip design, all funded in the same week, all domestic. China is building the full stack for a technology that doesn’t matter much today but will matter enormously once AI clusters outgrow current optical infrastructure.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.