The China Round — April 17, 2026

The Supply Chain Strikes Back

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

Where the Money Went

102 deals from April 10 to 17. $1.63 billion (~¥11.7B) in disclosed capital across 27 of them — the other 75 went undisclosed. Robotics commanded $937 million (~¥6.75B) of that, across 23 deals. This week, though, the more interesting pattern runs underneath the headline numbers: listed companies and OEM customers are entering venture rounds not as passive financial investors but as strategic acquirers, buying equity positions in their key suppliers before commercial volumes arrive.

🤖 Robotics (23 deals)

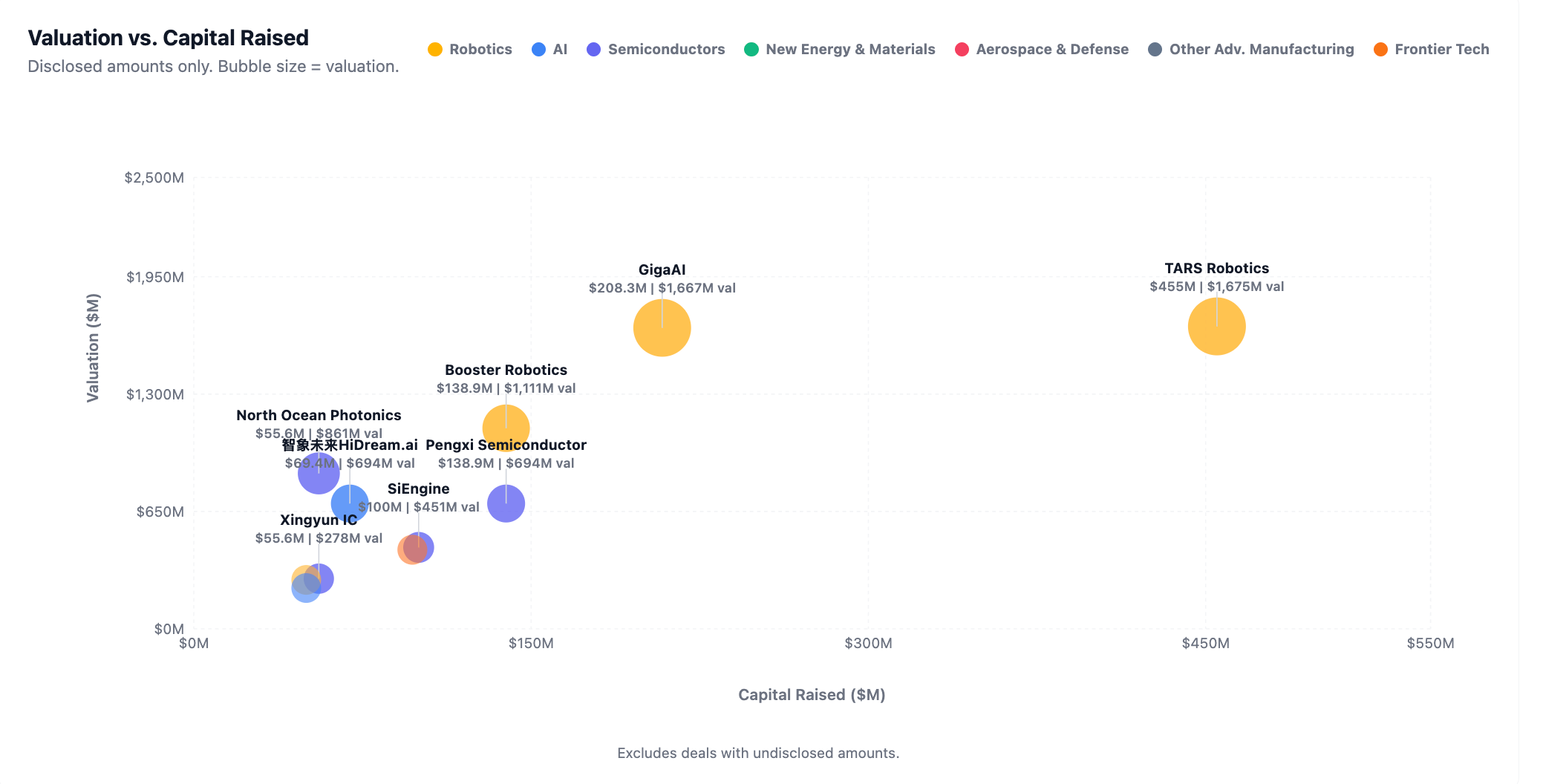

它石智航 (TARS Robotics) closed a $455 million (~¥32.8亿) Pre-A, reportedly the largest private embodied AI raise in Chinese history, with Hillhouse, HongShan, and Meituan co-leading 14 months after founding. The stage distribution across the batch forms a barbell: eight angel and Pre-A rounds ran alongside five B+ or strategic rounds, with almost nothing in between.

🧠 AI (17 deals)

The bulk of the disclosed capital — ¥5亿+ (~$70M+) — went into one company: 智象未来 (HiDream.ai), which released an MIT-licensed open-source image model before closing this round. The broader batch skews early, with Anhui, Hefei, and Beijing municipal capital prominent as co-investors.

🔬 Semiconductors (23 deals)

The sector’s headline event was not a venture round. 盛合晶微 (SJ Semiconductor, 688820.SH) listed on the STAR Market 2,700 times oversubscribed, reaching a ¥360亿 (~$5B) market cap at issue, with ¥47.79亿 (~$664M) in net proceeds. As the #1 domestic 12-inch chip bumping provider and holder of 85% share in mainland 2.5D advanced packaging, it controls a chokepoint that every Chinese AI chip designer needs to reach production. Among the private rounds, 芯擎科技 closed a B+ at approximately $100 million (~¥720M) for its automotive cockpit chip platform, pulling in Yutong Bus (600066.SH) as a strategic co-investor, extending the company’s addressable market beyond passenger EVs.

⚡ New Energy & Materials (14 deals)

A quieter week for the sector. 疆海科技 (Zendure), which sells energy storage hardware across 63 countries and counts Europe and North America as its primary markets, raised a round led by domestic strategic investors. 顺铉新材, a specialty polyimide film producer with export relationships into South Korea, Japan, the US, and Russia, closed a materials round. Neither disclosed amounts.

🚀 Aerospace & Defense (9 deals)

边界智控 (Boundary.AI) closed a B-round for its eVTOL flight control systems — the only Chinese company to have cleared CAAC’s SOI#1 airworthiness review for eVTOL-specific FCS. The rest of the batch was light: several pre-A rounds for drone platforms and satellite sensor startups, mostly undisclosed.

⚙️ Other Advanced Manufacturing (12 deals)

Mixed batch with no standout cluster. 锐能科技 raised a B-round with 菱电电控 (688667.SH) acquiring 30% as a strategic lead. Several other industrial automation plays closed early-stage rounds with regional government funds, consistent with the ongoing manufacturing digitization push in non-coastal provinces.

💡 Frontier Tech (4 deals)

量旋科技 (SpinQ) — announced April 3, flagged in this week’s straggler batch — sells superconducting quantum computers commercially into 200+ institutions across 40+ countries and raised ¥6亿 (~$83M) in a C+, several months after closing its C-round, bringing the combined C-series total to approximately ¥10亿 (~$139M). The company is profitable and building out a pre-IPO syndicate with Guotai Junan Innovation and Chengdu state capital as new investors. NovaFusionX (诺瓦聚变) appears in this week’s data with its ¥7亿 (~$97M) 天使+ round but was covered in last week’s issue; refer to that report for the full analysis.

Spotlight

TARS Robotics (它石智航)

Pre-A, $455M (~¥32.8亿), valuation ¥120.58亿 (~$1.67B)

Humanoid robotics, 14 months old, betting against the VLA consensus.

TARS Robotics builds humanoid robots for industrial precision tasks — specifically the kinds of fine-motor assembly work that previous robot generations couldn’t reliably handle. The company’s A1 robot set a Guinness World Record in December 2025 for most wire harness insertions by a robot in an hour (105 valid sub-millimeter completions), a benchmark designed to prove capability for CATL-style battery assembly lines; the company was founded in February 2025.

The technology bet is explicit. TARS is building against the VLA (Vision-Language-Action) model orthodoxy that most Chinese and US humanoid companies are pursuing, arguing that large cross-embodiment models borrowed from language AI (”外来和尚” — literally “the foreign monk always chants best,” the Chinese idiom for assuming outside expertise is inherently superior) can’t deliver reliable industrial performance. Instead, TARS runs AWE3.0 (AI World Engine), a proprietary architecture with three components: OSD for panoramic sensorimotor decision-making, HTS for high-density tactile sensing, and LAS for smooth latent-space motion generation. The architecture debate has no settled answer, and TARS is the largest private bet on the non-VLA side.

Investors: Hillhouse (co-lead), HongShan (co-lead), Meituan (co-lead), Qiming Venture Partners (returning), and 15+ additional investors including Beijing municipal funds and state capital. The “$455M Pre-A = largest embodied AI private raise in Chinese history” claim is reported by multiple independent Chinese financial outlets and is unchallenged by competing data — treat it as plausible rather than certified.

HiDream.ai (智象未来)

New financing round, ¥5亿+ (~$70M+)

MIT-licensed image model, Q1 revenue already above full-year 2025.

HiDream.ai is a multimodal AI company that builds image generation models and related enterprise tools. Its HiDream-I1 — a 17-billion-parameter model released under an MIT license — scored at the top of HPSv2.1 benchmark testing across all four style categories (animation, concept art, painting, photo) ahead of Flux.1-dev, Stable Cascade, DALL-E 3, and Midjourney V6, per the company’s own technical benchmarking. The company says Q1 2026 revenue exceeded its full-year 2025 figure, with over 30 million registered professional users and 40,000+ enterprise clients including Huawei Cloud and TikTok Shop. Those are company-stated figures, not independently audited.

HiDream released a frontier model for free, built a global developer user base, and used that credibility to close institutional capital at a scale that enterprise SaaS revenue alone wouldn’t support at this stage. The same open-source-to-capital sequence runs across several companies in this batch — more on that in The Bigger Picture.

Founder Mei Tao was VP at JD.com and Senior Research Manager at Microsoft Research Asia; he is a foreign academician of the Canadian Academy of Engineering. The round brought in Oriental Rich Capital as a new investor alongside a state capital stack from Anhui and Hefei: Anhui Venture Capital, Hefei Industrial Investment, Hefei High-Tech Investment, and the Anhui Provincial AI Fund. Prior investors, including Anhui state capital from the previous A-round, are continuing. The round was described by media as a “new financing round” — no Series letter confirmed in the primary announcement.

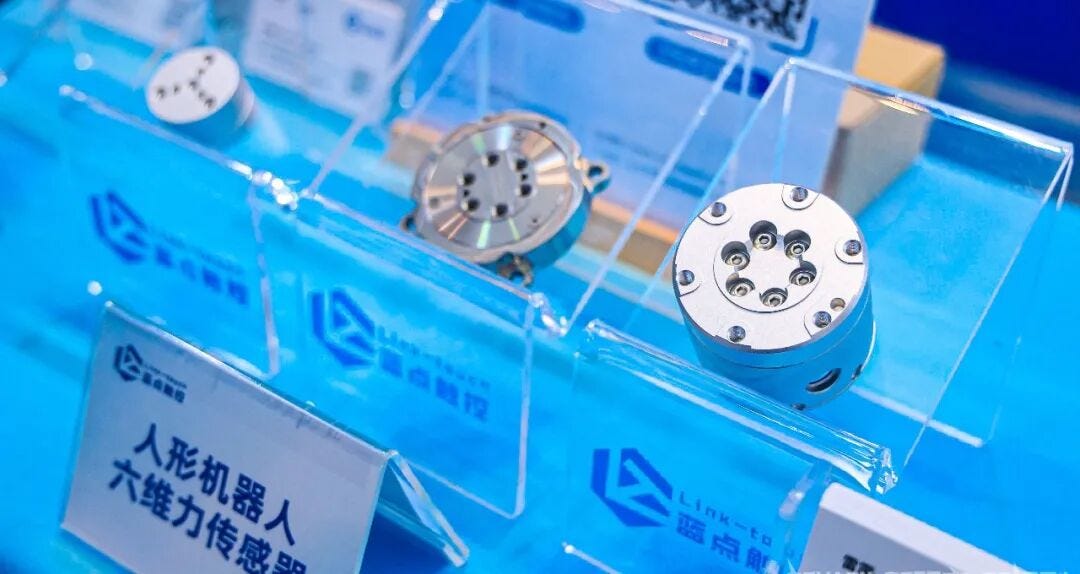

Link Touch (蓝点触控)

C+, 数亿人民币 (hundreds of millions of RMB)

72.6% humanoid six-axis force sensor market share. Customers are now shareholders.

Link Touch makes six-axis force/torque sensors and joint torque sensors for humanoid robots, with a 72.6% share of the humanoid six-axis force sensor market as of Q3 2025, according to GGII industry research. The company has doubled its revenue every year for three consecutive years, is on a confirmed IPO track per the CEO’s statement, and has shipped over 100,000 units. The C+ round came approximately five months after the November 2025 C-round led by HongShan — the company has now raised a new round three times in under a year.

The investor composition tells the supply chain story more clearly than any market share figure. The C+ brought in CATL (via its CVC arm Puquan Capital), AgiBot, and Galaxy General Robotics as new co-investors — the latter two being two of Link Touch’s largest humanoid robot customers. Two customers converted to shareholders in the same transaction, locking in supply alignment before humanoid volumes actually arrive. Autoptic and Galaxy Yuanhui rounded out the round. The structure echoes what Huawei did with semiconductor suppliers between 2019 and 2022: equity plus procurement logic, with the supplier gaining committed demand and the customer securing component access.

The valuation was not disclosed in any primary announcement.

Investors: CATL (via Puquan Capital), AgiBot, Galaxy General Robotics, Autoptic, Galaxy Yuanhui.

Also on the Radar

极佳视界 (GigaAI) — Series B1, ¥15亿 (~$208M), ¥120亿 (~$1.67B) val. ¥25亿 (~$347M) raised in 30 days: ¥10亿 (~$139M) Pre-B in March, then this B1 in April. The company claims GigaWorld-1 ranks at the top of the WorldArena live leaderboard above Google and NVIDIA models — note that the published WorldArena paper (February 2026) evaluated GigaWorld-0, which did not place first; the #1 claim refers to a subsequent live-leaderboard submission. The Maker H01 humanoid is targeting 1,000 units in 2026. Huawei Habo invested in the A1-round; the B1 added state funds from Wuhan, Guiyang, Shandong, and Shanghai alongside an unnamed tech giant as strategic.

PsiBot (灵初智能) — Series A, undisclosed, ¥90亿 (~$1.25B) val. Embodied intelligence company whose Psi-R2 manipulation model tops the MolmoSpace benchmark — an Allen Institute for AI robotics evaluation platform — above Physical Intelligence and other international teams, per QbitAI reporting. SDIC Pioneer (national-level industrial fund) and a Beijing municipal fund co-led the A-round; Hillhouse was the angel. A ¥90亿 valuation on an undisclosed amount, in a government-anchored round, is the investor composition doing the talking.

BOTINKIT (不停科技) — B+/B++ combined ~$50M (~¥360M), ¥19.5亿 (~$271M) val. AI kitchen robots deployed across 29 countries at Disneyland, Jollibee, Walmart, Rewe, Foodstuffs, and LSG Sky Chefs (Lufthansa catering). The most internationally distributed robotics company in this batch, and one of the least covered in Western tech media. Investors include ZeroOne Ventures and Genesis Capital, with SSC Capital as FA. HKUST robotics faculty (Li Zexiang, Gao Bingqiang, Gan Jie) remain on the cap table from the angel round.

Sand.ai — B-round, reportedly ~$50M (~¥360M). Sub-30 people, $10M+ ARR reported. CEO Cao Yue is the lead author of Swin Transformer (ICCV 2021 Best Paper, 30,000+ citations). The company open-sourced MAGI-1, its video generation model.

SiEngine (芯擎科技) — Series B+, ~$100M (~¥720M), ¥32.5亿 (~$451M) val. The DragonEagle-1 (龙鹰一号) is a 7nm automotive cockpit SoC (TSMC-fabbed), #1 domestic automotive cockpit chip by 2024 shipments with 1M+ units shipped and ASIL-D certification. Yutong Bus (600066.SH) joined as strategic co-investor, extending the addressable market beyond passenger EVs. Jingming Capital led.

Xingyun IC (行云集成电路) — Pre-A, ¥4亿 (~$56M), ¥20亿 (~$278M) val. LLM inference-first GPU with CUDA compatibility, targeting AI server mass production in 2026. Tsinghua founders (CEO Ji Yu), Zhipu AI as angel strategic investor, 5Y Capital and Primavera Capital co-leading the Pre-A. The post-DeepSeek inference demand story (where local GPU alternatives become competitive precisely on inference cost rather than training throughput) makes this the most coherent domestic GPU pitch in the current batch.

Boundary.AI (边界智控) — Series B, over ¥100M (~$14M+), ¥5亿 (~$69M) val. The only Chinese eVTOL-specific flight control company to clear CAAC’s SOI#1 airworthiness review, with a triple-redundant dual-channel architecture meeting DO-178C/DO-254/DO-160G compliance — the certification stack that maps to FAA/EASA requirements. That’s the regulatory moat for any non-Chinese eVTOL program needing a redundant FCS supplier. Customers include several Chinese eVTOL manufacturers. Xiamen Jianfa (Xiamen SOE) and Zhangjiang Group (Shanghai science park) co-invested, reflecting geographic positioning across two low-altitude economy pilot zones.

Simple AI (深朴智能) — Pre-A, hundreds of millions of RMB, ¥20亿 (~$278M) val. General-purpose embodied AI humanoid targeting home, hotel, and eldercare environments. Linear Capital and Puhua Capital co-led, with Shunwei Capital (Lei Jun / Xiaomi’s venture fund) participating as a strategic investor. Chief Scientist Wang Jiawei is ex-MSRA, ex-DeepSeek, and ex-ByteDance Seed with 10,000+ Scholar citations; Product VP Zhang Di brings 10+ years in robotics and 100,000+ units shipped. The Xiaomi ecosystem extending a bet on home humanoids without building in-house.

EncoSmart (享刻智能) — Series A, ¥1.5亿 (~$21M), ¥7.5亿 (~$104M) val. Commercial kitchen robots for fried chicken shop back-kitchens via its LAVA multi-task embodied operation system. Ninebot/Segway (689009.SH) acquired approximately 20% as strategic lead, contributing supply chain manufacturing access, platform technology, and distribution channels alongside the capital — not a passive financial stake. YiBo Capital acted as FA.

The Bigger Picture

Open code, closed rounds: how Chinese AI labs turned open-source into a capital strategy

HiDream released HiDream-I1 under an MIT license, built 30 million users on it (per company figures), and closed what Anhui and Hefei state capital joined as a major financing round on the strength of that user base. Q1 2026 revenue already exceeded the full year of 2025.

This is the same sequence running across several companies in this week’s batch. 极佳视界 (GigaAI) released GigaBrain-0.1 to Hugging Face (16,000+ downloads in two weeks), positioned it as the baseline for the CVPR 2026 GigaBrain Challenge, and is closing a ¥15亿 (~$208M) B1-round while targeting 1,000 Maker H01 humanoid units this year. 灵初智能 (PsiBot) published Psi-R2 as a manipulation foundation model before its A-round — both investors and the benchmark community evaluated the model before the company raised. Sand.ai open-sourced MAGI-1 while running $10M+ ARR on enterprise video generation. CEO Cao Yue’s authorship of Swin Transformer — an ICCV Best Paper with 30,000+ citations — is part of the credibility stack that precedes the round, not a credential that appears afterward.

The pattern is not the same as 2023-era open-source gestures, when Chinese labs published models partly to signal parity with US counterparts. In 2026, releasing a frontier model is functioning as a distribution mechanism: it acquires global developer users before products exist and converts that user base into institutional funding at valuation multiples that pure enterprise software can’t reach at comparable revenue stages. The model is the top-of-funnel, and the round is the conversion event. As MIT Technology Review documented in February 2026, Chinese labs from Alibaba Qwen to MiniMax have made open-weight releases central to their global positioning, with Qwen already overtaking Meta’s Llama in HuggingFace downloads. The same logic now runs inside robotics and embodied AI rounds.

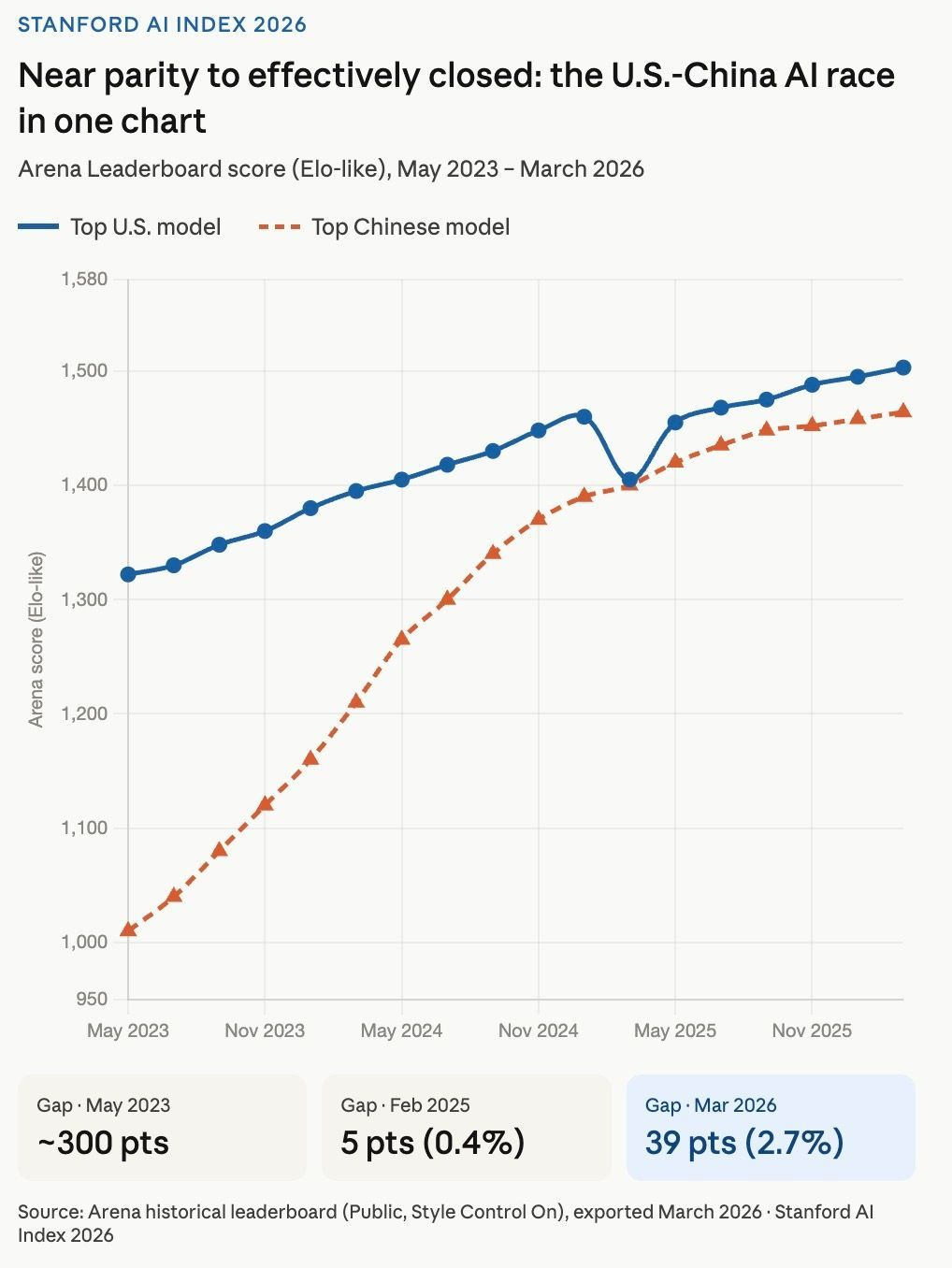

The structural context for why this works: the Stanford AI Index 2026 found the Arena Leaderboard gap between the top US and top Chinese model had closed from roughly 300 points in May 2023 to 39 points — 2.7% — by March 2026, with DeepSeek-R1 briefly matching the leading US model in February 2025. China produced 30 notable AI models in 2025, holds 74.2% of global AI patents granted in 2024, and accounts for 20.6% of global AI research citations. Open-source distribution only works as a capital formation strategy if the models are good enough to earn genuine global adoption. The data says they are.

One complication worth naming: the benchmark claims are not all equally clean. HiDream’s HPSv2.1 result comes from the company’s own technical paper — applying the HPSv2.1 scoring model to a comparison set they selected. On Artificial Analysis, an independent aggregator, HiDream-I1 ranked second in April 2026. GigaWorld-1’s WorldArena #1 claim refers to a self-submission on the live leaderboard; the published WorldArena paper (February 2026) evaluated GigaWorld-0, which did not place first. PsiBot’s Psi-R2 MolmoSpace ranking is confirmed by QbitAI reporting and is the cleanest of the three claims. The pattern holds; some of the evidence supporting it is more self-reported than independent.

Customers becoming shareholders

Five deals this week share a structure: a listed company or OEM customer takes a direct equity stake in a key supplier, typically with commercial commitments bundled into the transaction. OneRobotics (06600.HK) acquired 21% of HITBOT — China’s #1 robot dexterous hand company by 2025 shipments — for ¥2.41亿 (~$33M) in a deal implying a ¥11.46亿 (~$159M) total valuation, which represents strategic pricing rather than market rate for a sector leader. Ninebot/Segway (689009.SH) led EncoSmart’s A-round with a strategic equity position, contributing supply chain access alongside capital. Link Touch’s C+ converted AgiBot and Galaxy General — two of its largest humanoid customers — directly into co-investors alongside CATL’s CVC. Lincontrol (688667.SH) acquired 30% of RNTECH, and Yutong Bus (600066.SH) joined SiEngine’s B+ as a strategic co-investor, expanding the automotive chip company’s exposure to commercial vehicles.

The clearest historical precedent is Huawei’s Habo investment program, which between 2019 and 2022 built equity stakes in approximately 40 semiconductor suppliers using a product-plus-orders-plus-capital model: equity paired with procurement commitments, at below-market valuations, creating strategic lock-in before demand outpaced supply. Several Habo portfolio companies saw Huawei account for 70–90% of their revenue post-investment, which turned out to be a structural vulnerability when Huawei’s own position came under pressure. The robotics version of this pattern is more distributed, with no single OEM running it: Ninebot, Yutong, OneRobotics, CATL, and Lincontrol each making independent moves with the same underlying logic — buy supply chain security before commercial volumes make those positions expensive to acquire.

Some of this week’s strategic commitments may involve circular logic. Where the customer-investor is also the company’s primary revenue source and the investment is structured to validate a valuation that pure financial investors wouldn’t support, the “strategic validation” can be self-referential. The cleaner cases — Ninebot’s platform and channel commitments to a commercial kitchen robot company, CATL’s material interest in sensor supply for humanoid assembly — are ones where the strategic rationale exists independently of the deal structure. The sector is producing enough volume now to tell those cases apart.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.