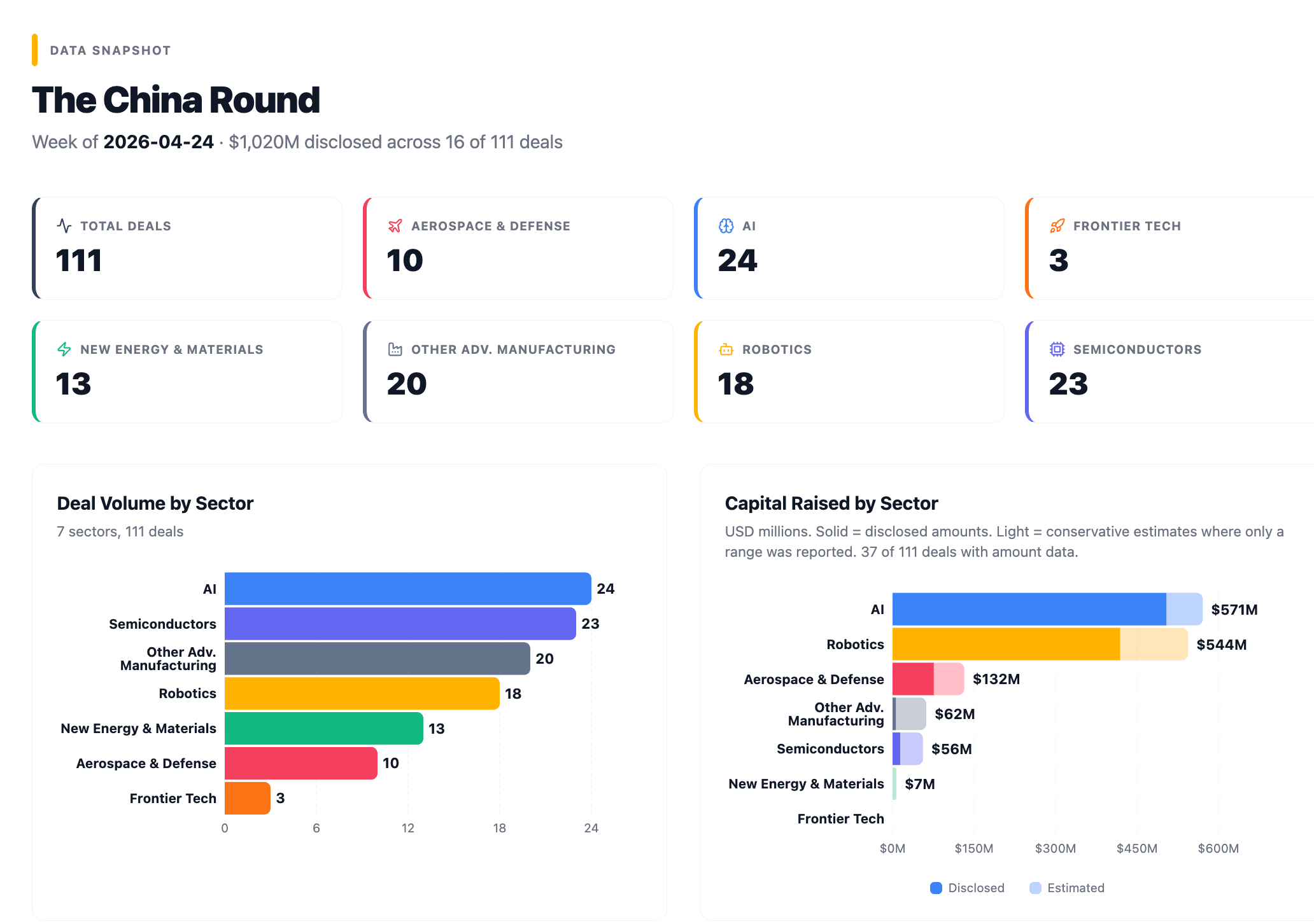

The China Round — April 24, 2026

Co-Owned Robots, a Pre-Revenue $2B Valuation, and Beijing's Coordinated Compute Bet

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

Where the Money Went

111 deals in seven days, $1,020M (~¥7.3B) in disclosed capital, and 95 of those 111 deals didn’t disclose. All the visible money concentrates in a handful of large rounds: robotics ($419M) and AI ($504M) collected 90% of the total while generating fewer than 40% of the deals. Semiconductors ran the highest deal count of any sector at 23, but almost none disclosed amounts, operating early-stage and quiet.

🤖 Robotics (18 deals)

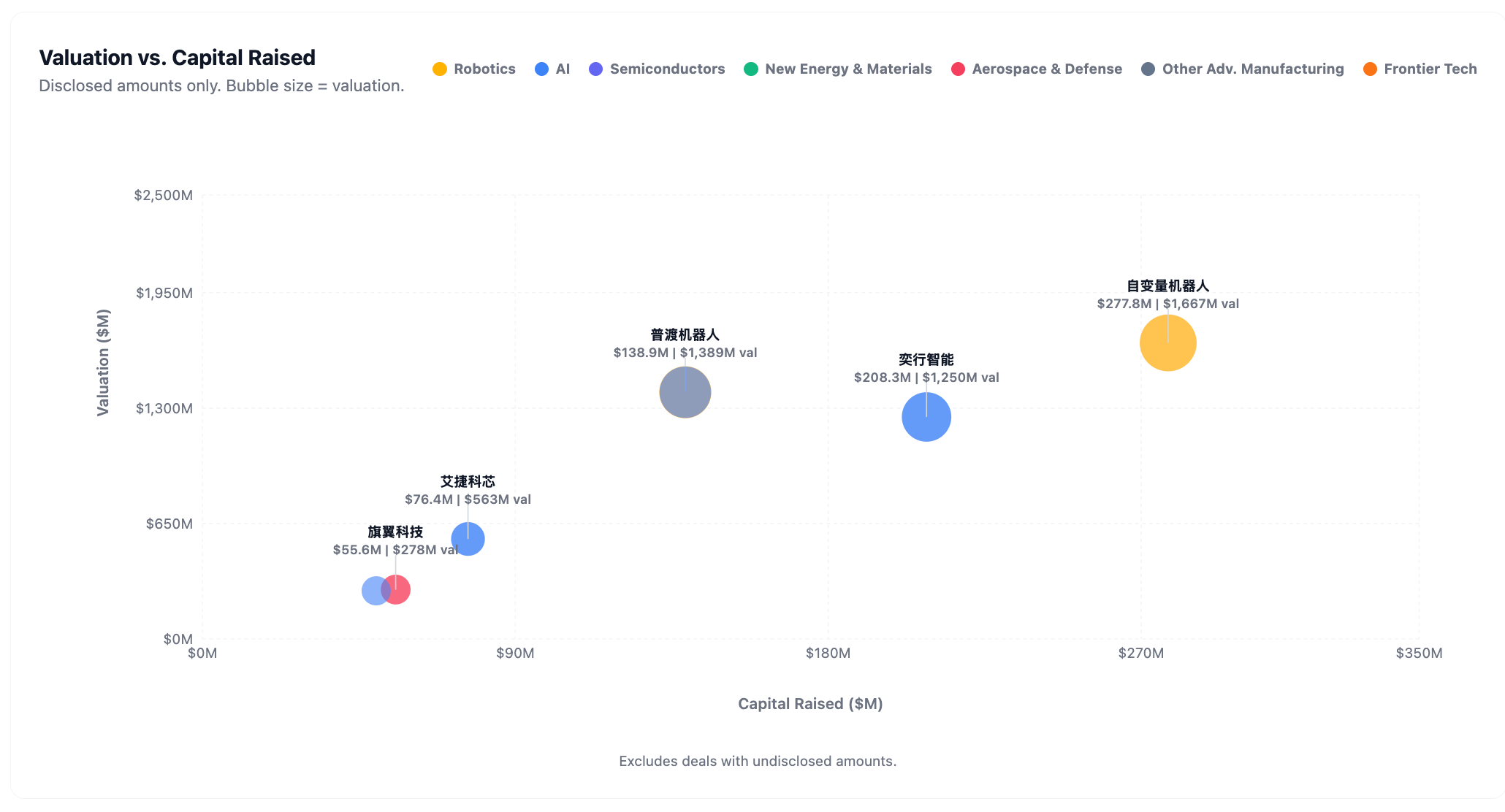

Sudu Technology came in at a reported $2B+ valuation at 11 months old and demo stage; X Square Robot collected all four of China’s internet giants on a single cap table at ¥2B (~$278M) Series B. The bottom of the distribution is a long tail of ~$690K seed rounds for pre-product startups building everything from dexterous hands to explosion-proof industrial quadrupeds. The component layer sits between them: Motorevo shipped 100,000+ joint modules in 2025 and is still valued at ¥1.6B (~$222M). The stage distribution skews to the extremes, with large late-stage rounds and a long tail of sub-¥10M seeds, but few companies in between.

🧠 AI (24 deals)

EVAS closed the week’s largest AI round at ¥1.5B (~$208M) with four Beijing municipal funds co-leading simultaneously, one day after Beijing formally established the ¥20B (~$2.8B) four-fund structure that backed the round. Sunrise AI (曦望) extended its run to seven financing rounds in ~16 months, crossing ¥10B (~$1.4B) valuation as China’s first inference-GPU unicorn. Loopit’s $50M (~¥360M) round (Garena lead) follows the app reaching #1 on the global Google Play Entertainment chart.

🔬 Semiconductors (23 deals)

The highest deal count of any sector, but almost none disclosed. The sector’s early-stage density is running well ahead of its public capital story. Two companies warrant attention regardless: NanoLN (晶正电子) is raising Pre-IPO financing as the holder of approximately 78% of global lithium niobate thin-film wafer supply, a material foundational to 5G filters and photonic chips. Wendun Juxin (稳顿聚芯) shipped China’s first domestic high-precision compound-semiconductor stepper in September 2025 and is already profitable. Neither has significant English-language coverage.

⚡ New Energy & Materials (13 deals)

Zero disclosed capital across 13 deals. Sodium battery, flow battery, and advanced materials companies raising without announcing terms. Luquos Energy (易池新能, CUHK spinout) is the exception, a Hong Kong-registered flow battery company with international backing (Towngas + Gobi Partners) that chose to disclose.

🚀 Aerospace & Defense (10 deals)

The National Strategic Emerging Industry Investment Fund (国调基金) made a strategic investment in Chang Guang Satellite that accounts for most of the sector’s visible capital, a state-capital substitute for the financial and foreign investors who exited after Chang Guang was placed on the US Treasury’s SDN (Specially Designated Nationals) sanctions list. FAW Group’s eVTOL spinout Qiyi Technology (旗翼科技) added the week’s largest angel-stage aerospace deal at ¥400M (~$55M).

⚙️ Other Advanced Manufacturing (20 deals) · 💡 Frontier Tech (3 deals)

Audfly (清听声学) stands out in Other Adv. Manufacturing with a Series B+ at ¥2B (~$278M), a directional audio company backed by Lenovo Ventures. Frontier Tech had just three deals: a synthetic biology Series A from PAML Biotechnologies (柏垠生物, Hillhouse-adjacent capital) and a fusion-wire JV from Juneng Superconducting (聚能超导).

Spotlight

EVAS (奕行智能)

Series B, ¥1.5B (~$208M)

China’s first reportedly mass-produced RISC-V AI chip, now backed by Beijing’s four-fund industrial apparatus.

EVAS makes AI chips built on RISC-V, an open-source chip architecture that carries no US intellectual property. Every Chinese chip company designing on Arm or x86 carries licensing risk: a single US policy change could cut access to the architecture itself. RISC-V removes that dependency entirely. EVAS’s Epoch series entered mass production in early 2025 for data center, internet, and automotive AI customers, reportedly making it the first Chinese company to ship RISC-V AI chips at scale. CEO Liu Hui (刘珲) is a semiconductor veteran from Socionext, STMicroelectronics, and Fujitsu.

The timing of this round is worth noting. Beijing formally launched a ¥20B (~$2.8B) four-fund structure on April 21. All four funds co-led EVAS’s Series B the next day. That sequencing was almost certainly pre-arranged, but the public choreography is the point: the government is signaling that RISC-V is the chosen path for compute independence, and converting that signal into capital allocation immediately. Eight Chinese ministries coordinated a national RISC-V push in 2025. If RISC-V AI chips reach performance parity with Arm-based alternatives, China’s entire inference stack could eventually run on architecture that no export control can touch. The investor line here is entirely government capital with no commercial VCs, which tells you Beijing is treating RISC-V compute as public infrastructure.

Four Beijing municipal funds co-led: the E-Town Industry Upgrade Fund (亦庄国投), the Beijing High-Precision Industries Development Fund, the Beijing Information Industries Fund, and the Beijing AI Industry Fund. And/Li Capital, Bolly Ventures, Sayi Industries Fund, Longjiang Fund, Qingtan Capital, and Jiukun Ventures participate.

Sudu Technology (苏度科技)

New financing round, amount undisclosed, valuation reported at $2B+ (~¥14.4B+)

Eleven months old, demo-stage, and reportedly valued above $2 billion (~¥14.4B), the most extreme pre-revenue ratio in this week’s cohort.

Sudu Technology builds what it calls a universal embodied AI platform: a “robot brain” that uses 3D world models with reinforcement learning to handle manipulation tasks involving transparent, reflective, and flexible objects, categories where most robotic vision systems still fail. Picking up a glass, folding a towel, handling a bag of chips without crushing it. These are trivially easy for humans but remain unsolved at scale in robotics because the objects deform, reflect, or transmit light in ways that break standard computer vision. Sudu’s approach trains its system to build a 3D understanding of the world and learn through trial and error rather than following pre-programmed routines. Its flagship Sudo R1 has been demonstrated in 60-minute unedited real-world testing footage released publicly. CEO Han Zheng (韩铮) co-founded the company in May 2025. The company is 11 months old.

Chief Technical Advisor Su Hao (苏昊) is the credentialing anchor for the valuation. He co-created ImageNet in 2009 with Fei-Fei Li at Stanford, the massive labeled image database that effectively launched modern deep learning. Before ImageNet, AI systems struggled to reliably distinguish a cat from a dog; by giving researchers millions of labeled images to train on, the project enabled the breakthroughs in computer vision that now power everything from autonomous driving to facial recognition. Su also pioneered PointNet, the foundational architecture for processing 3D point cloud data, which is how robots understand spatial environments. He concurrently leads Fudan University’s Institute of General Physical Intelligence. The investor bet is that embodied AI could follow a similar path from academic foundation to commercial platform, and that whoever controls the software layer of the robot stack controls the platform.

The investor line reflects that bet across sectors: CATL positioning for the robot power stack, Alibaba, Tencent, and Ant Group as platform companies that would distribute robots through their ecosystems, and IDG, Hillhouse, and China Life as financial conviction. Whether $2B for a demo-stage product is early-stage pricing for a future platform or the clearest evidence of capital running ahead of commercial reality is the open question. The amount raised in this round has not been publicly disclosed.

CATL, Alibaba, Tencent, Ant Group, IDG Capital, Hillhouse, China Life Equity, BlueRun Ventures, Futen Capital (孚腾资本), Digital Future (数字未来), Fudan Innovation (复旦科创), and Yunhui Capital (云晖资本). Financial advisor: Gaogul Capital (高鹄资本).

X Square Robot (自变量机器人)

Series B, ¥2B (~$278M) @ ¥12B (~$1.67B) val

Humanoid robot butlers deployed in Chinese homes, and the first time all four of China’s internet giants are on one cap table.

X Square Robot builds general-purpose humanoid robots on its proprietary WALL-A foundation model, a unified architecture processing vision, language, touch, and motion through a single system. The Quanta X2 humanoid stands 172cm with a 6kg payload per arm. In March 2026, the company launched a commercial home-cleaning service via 58 Daojia, China’s largest home services platform, making it the first Chinese company to deploy humanoid robots into homes at commercial scale. The company also unveiled WALL-B, a home-environment AI model, the same week as this round closed. Founded December 2023, it has raised nine rounds totalling over ¥3B (~$417M) in under two and a half years.

ByteDance, Meituan, Alibaba, and Xiaomi are now simultaneously on the cap table, the first time China’s four largest internet platforms have co-invested in the same embodied AI company. Each came in at a different round: Meituan led the Series A in May 2025 as sole investor; Alibaba Cloud co-led the A+ in September; ByteDance co-led the A++ in January 2026; Xiaomi co-leads this B. In the 2015 bike-sharing era, these same companies funded competing startups against each other. Here they are all on the same cap table, which is either a sign of X Square’s dominance or a sign that each platform wants guaranteed access to whatever the home robot deployment layer becomes. Each brings different distribution: Xiaomi’s consumer hardware retail, Meituan’s home services network, Alibaba’s cloud and logistics, ByteDance’s content discovery.

Sequoia China and Xiaomi Strategic Investment co-lead. ByteDance, Meituan, Alibaba Cloud.

Loopit (涌跃智能)

Third round in 2026, $50M (~¥360M)

Global #1 on Google Play Entertainment, $50M from Garena, and a distribution play into Southeast Asia.

Loopit is an AI interactive content platform. Users type a prompt and the app generates a rich mobile experience combining images, audio, video, and 3D elements that responds to the phone’s sensors (microphone, gyroscope, camera) in real time. Instead of scrolling past a video, you’re inside it, tilting your phone to explore, speaking to change the scene. CEO Chen Weipeng (陈炜鹏) co-founded and led the large-model team at Baichuan AI, previously building products at Sogou and Soul. The app launched in February 2026, hit #1 in the Google Play Entertainment category globally and #8 overall within two months, and in February Elon Musk reposted a user-generated Loopit video on X.

A Chinese consumer AI app reaching #1 globally on Google Play is still rare (TikTok remains the only real precedent at that scale), and that traction is what brought Garena to the table. Sea Group’s gaming arm operates across Southeast Asia (Indonesia, the Philippines, Thailand, Vietnam, Malaysia, Taiwan) in markets where Loopit’s interactive content format travels naturally among mobile-first, gaming-native users. Garena gets a position in the content format before Instagram Reels or TikTok can copy the interactivity layer; Loopit gets SE Asia distribution that a Beijing startup would take years to build independently. Chen built the large language model team at Baichuan AI (one of China’s leading foundation model companies), which suggests the AI generation engine underneath is purpose-built rather than an API wrapper around someone else’s model.

Garena (lead), Jingwei China (经纬中国, fourth check into the company), BlueRun Ventures, Yingce Capital (渶策资本), Bairui Capital (柏睿资本). Financial advisor: Gaogul Capital (高鹄资本).

Chang Guang Satellite (长光卫星)

Strategic investment, hundreds of millions RMB, valuation ~¥16B (~$2.2B)

The US Treasury listed it as a sanctioned entity. China’s sovereign development fund just became its anchor investor.

Chang Guang Satellite operates the Jilin-1 constellation, the world’s largest sub-meter resolution commercial remote sensing satellite constellation, with 144–152 satellites in orbit delivering optical imagery to government, enterprise, and international customers. The company was founded in 2014 as a spinout from the Changchun Institute of Optics, Fine Mechanics and Physics, and had been building toward a STAR Market IPO since a 2022 filing. In December 2023, the US Treasury placed it on the SDN (Specially Designated Nationals) sanctions list for selling satellite imagery to Wagner Group proxy entities, covering Ukrainian battlefields and Wagner’s operational areas in Africa. Foreign investors exited. The IPO was withdrawn in late 2024

In January 2026, Chang Guang re-filed for a STAR Market IPO under new rules that extend the exchange’s fifth listing standard to commercial aerospace companies, removing strict profit requirements for companies whose value is in technology rather than current earnings. This week, the National Strategic Emerging Industry Investment Fund (国调基金), managed by China Chengtong, one of two state-owned capital operating companies that deploy sovereign investment on behalf of the State Council, completed a strategic Pre-IPO investment at a valuation reported by deal databases at around ¥16B (~$2.2B). The capital the SDN designation drove away, foreign investors and commercial VCs with compliance exposure, has been replaced by a sovereign fund whose mandate is national strategic interest rather than financial return.

National Strategic Emerging Industry Investment Fund (国调基金), managed by Chengtong Fund Management under China Chengtong Holdings (中国诚通).

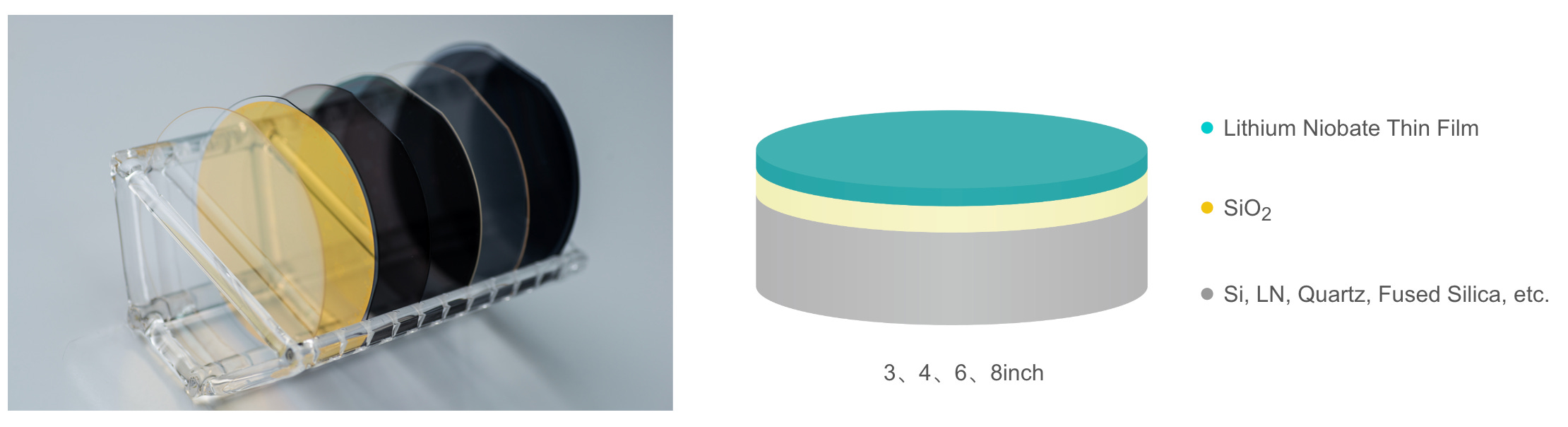

NanoLN (晶正电子)

Pre-IPO round, amount undisclosed

The company that holds approximately 78% of global lithium niobate thin-film wafer supply is heading for a public listing.

NanoLN makes lithium niobate thin-film (LNOI) and lithium tantalate thin-film (LTOI) wafers. These are nanometer-thick crystalline films that manipulate light and radio signals, and they sit inside a surprising range of critical hardware: the RF filters in every 5G base station, the electro-optic modulators that move data through fiber optic connections in AI data centers, LiDAR ranging systems, and quantum communication devices. Founded in 2010 in Jinan, the capital of Shandong province on China’s east coast by returnee entrepreneur Hu Wen, NanoLN was the first company globally to achieve industrialized production of these films and the first to produce 8-inch LNOI wafers. Huawei Hubble is an early investor. The company serves 200+ customers across China, the US, Japan, and Europe.

NanoLN holds approximately 78% of global LNOI wafer supply per Yole (2023Q3), with the remainder split between NTT Advanced Technology and SCIOCS (both Japan). That near-monopoly feeds two accelerating demand curves: 5G infrastructure buildout and AI data center photonics, where the optical interconnects between GPU clusters increasingly rely on LNOI-based modulators. In practice, a significant share of the world’s 5G filters and data center photonic links depend on wafers from a single Chinese company, a supply chain concentration comparable to TSMC’s position in advanced logic chips, though at a much earlier stage of geopolitical visibility. The Pre-IPO round is the step before a listing that will ask Chinese capital markets to price a deep-tech materials monopolist with a global customer base for the first time.

Leading Investment, Shandong Expressway, Jiantou Investment, and reportedly 10 additional investors.

Also on the Radar

Motorevo (泉智博) — A+ round, hundreds of millions RMB @ ¥1.6B (~$222M) val

100,000+ joint actuator modules (the motorized joints that make robot limbs move) shipped in 2025 to MIT, Tencent RoboticsX, Leju Robotics, and Peking University. Building million-unit annual capacity online now. At ¥1.6B (~$222M) valuation for a company with institutional customers and real revenue, it trades at a fraction of the multiple applied to software-first humanoid peers.

Investors: Shenzhen Investment Holdings leads.

AnnouncementPudu Robotics (普渡机器人) — New round, approximately ¥1B (~$139M) @ ¥10B (~$1.4B) val

120,000 commercial service robots across 80+ countries, 23% global market share, 100% revenue growth in 2025. First disclosed raise in three years; opened a Dallas headquarters the same week. A three-year fundraising gap followed by ¥1B and a US headquarters in the same week points to IPO preparation, not growth financing.

Investors: Longgang Financial Holdings and Asia Investment Capital co-lead.FAW Qiyi Technology (旗翼科技) — Angel round, ¥400M (~$55M) @ ¥2B (~$278M) val

China’s largest angel-stage eVTOL investment. FAW Group’s Tier-1 suppliers Fu’ao Auto Parts (thermal management) and Fuwei Auto Components (interiors) each invested ¥150M (~$21M) to lock in parts contracts before the aircraft finishes development. These are ICE-era automotive suppliers using equity to secure roles in the eVTOL supply chain before the commercial market exists, the same pattern that played out in EVs a decade ago.

Investors: FAW Group, Fu’ao Auto Parts, Fuwei Auto Components, Cornerstone Capital.Sunrise AI (曦望) — Strategic round, ¥1B+ (~$139M+) @ ¥10B+ (~$1.4B+) val

SenseTime’s inference GPU spinoff closes its seventh financing in ~16 months, crossing ¥10B (~$1.4B) valuation. S3 chip targets 90% cost reduction and 300%+ performance gain per token, a ¥0.01 (~$0.0014) per million token price floor for inference compute in China. 150 total engineers; capital-efficient by the standards of peers with 3–5x the headcount.

Investors: Hangzhou Capital leads; Puhua Capital co-invests.Juwei Technology (具微科技) — A+ round, hundreds of millions RMB @ ¥1.8B (~$250M) val

Fourth financing round in approximately two months. Builds explosion-proof wheeled quadruped robots for hazardous industrial environments, China’s first combined explosion-proof and increased-safety certification. Every lead investor (Weiqiao Group, Binhua Chemical, Binzhou SOE) operates the exact facilities the robot is designed to enter, effectively locking in anchor deployments before the product ships at scale.

Investors: Binzhou SOE Investment, Weiqiao Group, Binhua Chemical co-lead.CheeChips (奇世智能) — Angel round, tens of millions RMB

Silicon Valley-incorporated (Mountain View HQ) with a Shenzhen global R&D center, targeting a 59-product AI-powered maternal and infant care platform. The company structure and roadmap are designed for international distribution from inception.Xteink (阅星曈) — Series A, tens of millions RMB (Shunwei + Jingwei + Xiaohongshu)

Ultra-portable e-ink smartphone attachment with 2M+ global users before this institutional round. Xiaomi’s Shunwei Capital, Jingwei China, and Xiaohongshu join as investors, three platforms with overlapping consumer demographics and distribution value.

Investors: Shunwei Capital, Jingwei China, Xiaohongshu.Wendun Juxin (稳顶聚芯) — Strategic investment @ ¥500M (~$69M) val

China’s first domestic high-precision stepper (the lithography machine that prints circuit patterns onto wafers) for compound semiconductors like gallium nitride and silicon carbide, the wide-bandgap materials used in EV power electronics, 5G, and renewable energy. Shipping since September 2025 against Nikon and Canon incumbents. Projected ¥140M (~$19M) revenue for 2025 at roughly 32% net margin, profitable in its first year of shipment. Listed company Sudaweige (300331.SZ) already holds equity; the stock hit limit-up on the machine’s launch announcement.

Investors: Yigao Capital leads; Sudaweige (300331.SZ) confirmed strategic shareholder.Audfly (清听声学) — Series B+, hundreds of millions RMB @ ¥2B (~$278M) val

Parametric speaker tech that focuses sound into a directional beam, backed by Lenovo Ventures. Directional audio has no dominant commercial-scale incumbent, which puts OEM integration into consumer hardware as the likely route to scale.

Investors: Lenovo Ventures leads; Suchang Capital, Sugao Xinjin Holdings, and others follow.Luquos Energy (易池新能) — Pre-A, hundreds of millions RMB

Hong Kong-registered CUHK spinout building sulfur-iodine flow batteries, a type of large-scale energy storage where liquid electrolytes are pumped through cells, at 2x the energy density of the vanadium redox systems that currently dominate the market. Utility-scale storage targeting Southeast Asia, backed by Towngas (00003.HK) for strategic distribution and Gobi Partners for regional reach. The sulfur-iodine chemistry differentiates from vanadium incumbents, and the SE Asia focus avoids China’s crowded domestic storage market.

Investors: Oriza Holdings and Wuxi Guolian Xizhou Fund co-lead; Towngas (00003.HK) strategic; Gobi Partners.

Stragglers

萝博派对 (RoboParty) — Angel, amount undisclosed @ ~$4.5M (~¥32.5M) val

A small humanoid robot startup where the investors matter more than the amount. Shunwei Capital (Xiaomi’s fund) and Xiaomi co-invest, making this Xiaomi’s third robotics placement in a single week (leading X Square’s ¥2B Series B, backing RoboParty at angel, joining Xteink’s consumer AI hardware Series A). Xiaomi doesn’t place three hardware bets at Series B, angel, and Series A in a single week by accident. The spread from foundation-model humanoid to pre-product startup to consumer AI device looks like deliberate stack coverage.

The Bigger Picture

Why China’s Giants Are Backing the Same Robots

X Square Robot now has ByteDance, Meituan, Alibaba, and Xiaomi on a single cap table, the end state of a systematic accumulation across four rounds from May 2025 to April 2026. Sudu Technology closed a round this week at a reported $2B+ valuation, backed simultaneously by CATL, Alibaba, Tencent, Ant Group, IDG, Hillhouse, and China Life.

The logic has inverted from the shared-bike era of 2015–2016, when Alibaba and Tencent hedged across rivals, each backing different companies to ensure platform presence regardless of outcome. This week, multiple giants co-own the same company, concentrating upside rather than spreading risk. If whoever controls the robot “brain” layer controls the platform, the rational move is to own the leading candidate outright before commercial scale makes that position expensive to acquire.

The Sudu round is the stress-test of that logic taken to its limit. A company that was incorporated in May 2025 has attracted China’s most credentialed institutional investors simultaneously, at a price that values it above most Series C enterprise software companies with real revenue. Chief Technical Advisor Su Hao (苏昊) co-created ImageNet in 2009 and pioneered PointNet at Stanford, and his academic pedigree seeds the thesis that Sudu could do for robot manipulation what ImageNet did for computer vision. Either that analogy holds and $2B (~¥14.4B) underprices the eventual platform, or it doesn’t and the week’s robotics valuations are the clearest current evidence of capital running ahead of commercial reality.

X Square B round via 36kr · Sudu announcement via TMTPost · US/China humanoid valuation divergence via CNBC

Beijing’s Compute Bet Gets Coordinated

On April 21, 2026, Pedaily reported that Beijing’s Economic-Technological Development Area was formally establishing four new industrial guidance funds with a combined scale of ¥20B (~$2.8B). The four funds (covering integrated circuits and AI, robotics, biotech, and future industries) are jointly capitalized by the district’s fiscal budget and E-Town Capital (亦庄国投) as LP. On April 22, EVAS announced a ¥1.5B (~$208M) Series B led by all four of those funds simultaneously.

Beijing’s four-fund quartet didn’t evaluate EVAS and happen to co-invest. The round was the first deployed capital from a structure announced the previous day. The target is RISC-V AI chips. Arm and x86 carry US intellectual property; chip companies designing on them remain exposed to licensing dependencies that export controls can sever. RISC-V is royalty-free and carries no US IP. Eight Chinese government ministries coordinated a national RISC-V adoption push in 2025; EVAS becoming reportedly the first domestic company to mass-produce on the architecture is what Beijing’s capital apparatus is backing.

The compute coordination runs wider than EVAS. CXMT, China’s only domestic DRAM producer, took a 3.7% equity stake in AI inference chip startup AiJie Core (艾捷科芯) this week, acquiring it for ¥150M (~$21M). CXMT is targeting HBM3 production by end-2026, and an equity position in a downstream compute startup creates an anchor customer and co-development relationship before the memory market opens. Inference GPU unicorn Sunrise AI (曦望) simultaneously closed its seventh round in ~16 months at ¥10B (~$1.4B) valuation, led by Hangzhou state capital.

Three AI compute plays in one week, all with state-adjacent capital at the center. Taken together (fund structure announced April 21, EVAS round April 22, CXMT stake confirmed, Sunrise AI round closed), they show state capital coordinating across the compute stack simultaneously: RISC-V as the architecture, CXMT building the memory-plus-logic vertical, and inference efficiency as the commercial application layer.

Beijing four-fund structure via Pedaily · EVAS round via National Business Daily · RISC-V China policy via TrendForce

That’s it for this week. More next week.