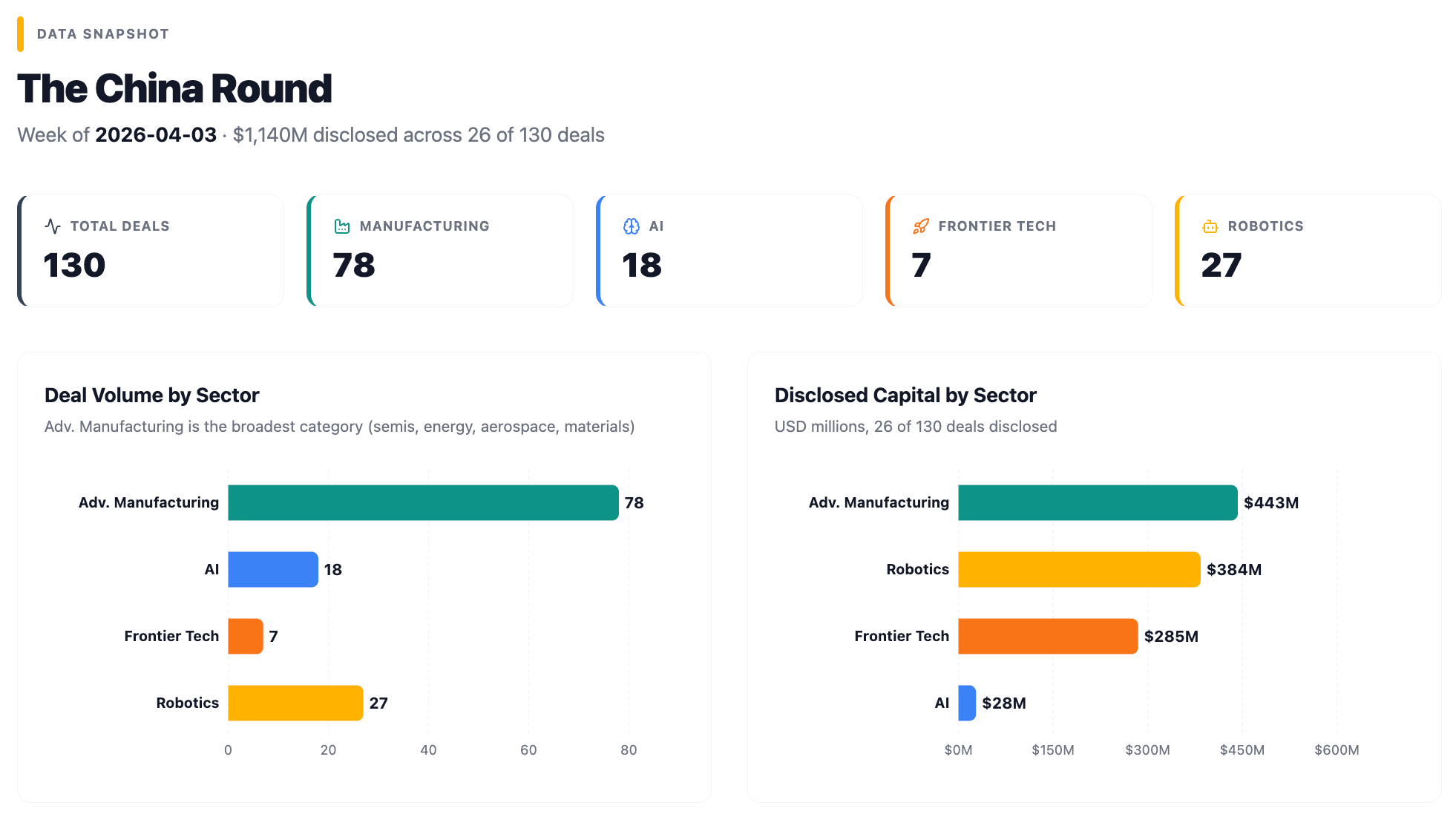

The China Round — April 3, 2026

Quantum, Cobots, and the Billion-Dollar Angels

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, advanced manufacturing, and frontier tech. These deals span semiconductors, autonomous driving, quantum computing, hydrogen and energy storage, eVTOL, brain-computer interfaces, synthetic biology, and more.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

Where the Money Went

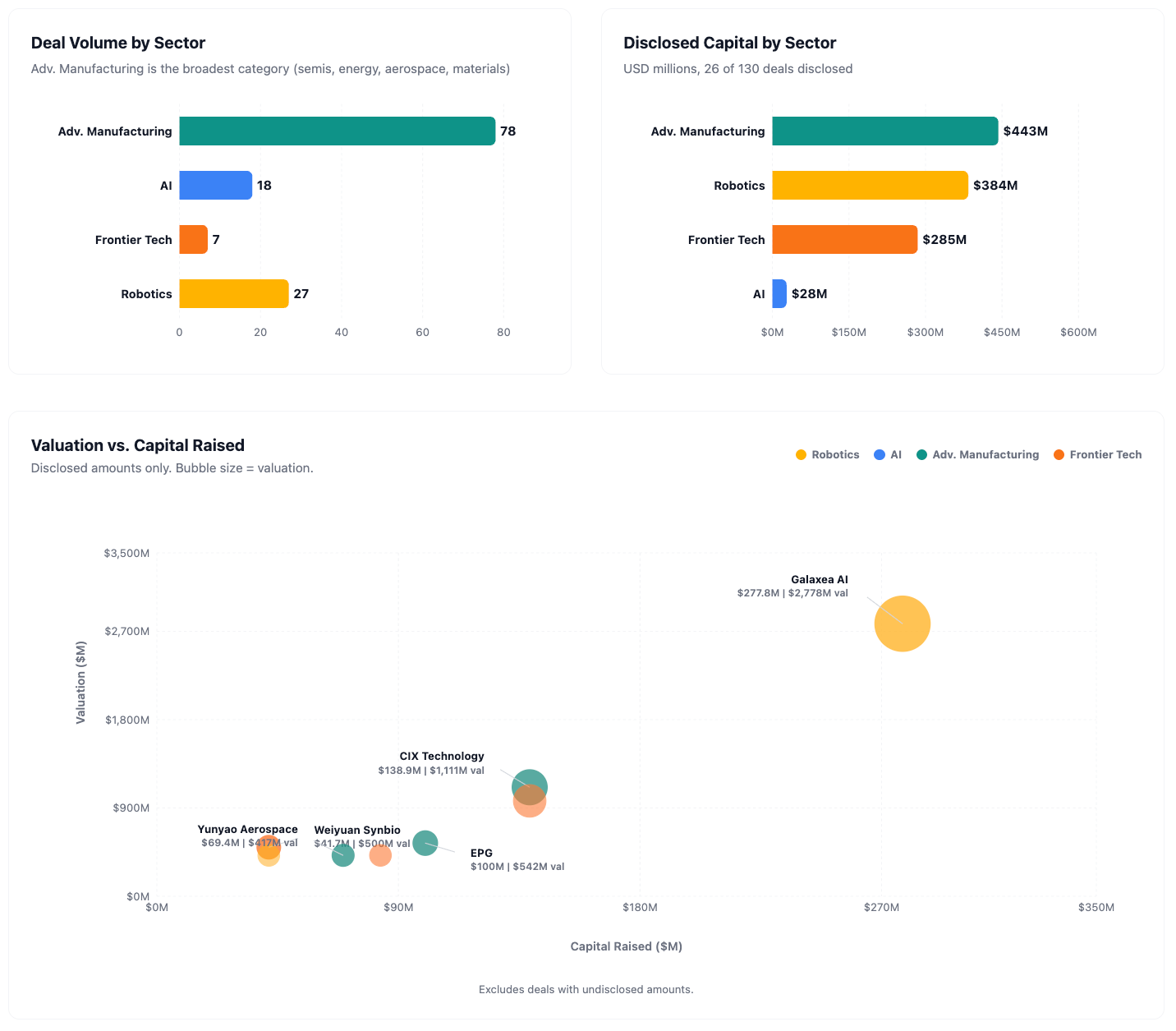

130 funding events across four sectors. Over $1.4 billion in disclosed capital. Three quantum computing raises totalling over ¥1.6 billion. Angel-stage valuations that would have been Series B territory two years ago. The A/A+ stage accounts for 38% of all deals, but the signal is loudest at the extremes.

🤖 Robotics (27 deals)

The busiest sector by narrative weight. 27 raises in seven days, at least eight of them embodied AI or humanoid plays. Galaxea AI (星海图) led with ¥2 billion (~$280M) for a B+ round, valuing the company at ¥20 billion. JAKA Robotics (节卡机器人) closed an E round at a ¥6 billion valuation, one of a handful of Chinese cobot companies with real international footprint. At the early end, multiple seed and angel rounds for companies building everything from cooking robots to ocean-floor inspection vehicles.

Stage breakdown: 11 angel/seed, 9 A/A+, 5 B+, 2 strategic. The early-stage density signals continued new entrant formation, not just incumbents scaling.

🧠 AI (18 deals)

18 deals, but the individual bets run larger than the count suggests. MOSI Intelligence (模思智能) pulled in hundreds of millions of RMB at angel stage for speech-first foundation models. Tsingwei (清微智能) hit Pre-IPO stage for AI inference chips. The rest skew early: lots of angel and Pre-A rounds for vertical AI applications (drug discovery, gaming, spatial reasoning, pet tech).

⚙️ Advanced Manufacturing (78 deals)

The largest category by volume, and the most diverse. Sub-sectors span semiconductors (~15 deals), hydrogen and energy storage (~10), aerospace and eVTOL (~6), lasers and photonics (~5), new materials (~8), and a long tail of sensors, drones, and industrial components. Headline deal: CIX Technology (此芯科技) raised ¥1 billion (~$140M) for ARM-compatible AI PC chips. EPG (易普集) closed $100M for modular data centers backed by Alibaba Cloud and BlackRock’s Decarbonization Partners.

💡 Frontier Tech (7 deals)

Small by count, massive by capital. Three quantum computing raises (see theme below). One invasive BCI company. Two synthetic biology startups. One display chip maker.

Spotlight

QBoson (玻色量子)

Series B, ¥1 billion (~$140M), ¥7 billion valuation (~$970M)

Photonic quantum computing.

QBoson builds photonic quantum computers for commercial deployment. CEO Wen Kai holds a Stanford PhD in quantum computing; the founding team includes researchers from Stanford, Tsinghua, and the Chinese Academy of Sciences. They have already shipped China’s first commercial photonic quantum computer, with 10+ units delivered to clients including the National Supercomputing Center in Chengdu and China Mobile. Their current system runs 550 qubits, with a 1,000-qubit model on the roadmap. QBoson broke ground on the world’s first dedicated photonic quantum computer manufacturing facility in Shenzhen last year.

Most quantum computers (IBM’s, Google’s, the ones generating the headlines) run on superconducting qubits that require cooling to near absolute zero, which means expensive dilution refrigerators and lab-scale infrastructure. Photonic quantum computers use particles of light instead, operate at room temperature, and are significantly easier to manufacture and deploy. The trade-off has historically been lower qubit fidelity, but photonics opens a path to commercial deployment that superconducting systems don’t. China has largely ceded the superconducting race to the US; photonics is the bet that there’s a different lane worth winning.

ICBC Capital (工银资本) and Shunxi Fund (顺禧基金) co-led, alongside Beijing Financial Holdings and others.

Galaxea AI (星海图)

Series B+, ¥2 billion (~$280M), ¥20 billion valuation (~$2.8B)

Embodied AI humanoid robot platform.

Galaxea AI builds universal dual-arm humanoid robot platforms (R1 Pro, R1 Lite) targeting factory-floor deployment and, eventually, general-purpose use. Founded September 2023 by Jiyang Gao (born 1992), Tsinghua to USC to Waymo to Momenta. Co-founded with Tsinghua robotics professor Huazhe Xu, who left in February 2026 to start Breaking Shell Robotics (see below). Meituan has been a major strategic investor since 2023. Per 36kr, the B round and this B+ round closed within a single month of each other. ¥20 billion valuation for a company two and a half years old. Target: 1,000 units shipped by end of 2026.

The wider bet is on becoming the platform layer for embodied AI: a robot learning to navigate and manipulate the real world will develop capabilities that a language model running in a data center never can. In the US, Figure, Physical Intelligence, and Apptronik are the main funded challengers. In China the serious platform plays are fewer: Unitree (already at 5,500 units per year at consumer price points), Agibot, and Galaxea. Chinese manufacturers have factory floors willing to deploy right now, giving China a training data advantage that’s hard to replicate from a US lab.

Lens Technology (蓝思科技), Silicon Core Ventures (矽芯投资), and 10 others; Huaxing Capital (华兴资本) as financial advisor.

MOSI Intelligence (模思智能)

Angel, hundreds of millions of RMB, ¥1.5 billion valuation (~$210M)

Speech-first foundation models.

MOSI Intelligence builds speech-first foundation models with a unified token structure across voice, video, text, and image. Founded November 2024 by Fudan professor Qiu Xipeng, who won the CCF-ACM AI Award and built MOSS, China’s first open-source ChatGPT alternative, in February 2023. Hundreds of millions of RMB at angel stage, ¥1.5 billion valuation, for a company founded 16 months ago by an academic.

Most Chinese AI labs started with text and added speech later. Qiu is going the other direction: voice as the primary modality. The product lineage (SpeechGPT, AnyGPT, MOSS-TTS series) is academic but credible. Target applications include consumer electronics, autonomous vehicles, and embodied AI, all domains where voice interaction matters more than text. The commercial question is whether speech-first is a genuine architectural advantage or a differentiated pitch, especially against established Chinese frontier models like Kimi and Minimax.

IDG Capital (IDG资本) led, with Yuanhe Holdings (元禾控股), MiraclePlus (奇绩创坛), Shanghai Future Industry Fund (上海未来产业基金), and others.

CIX Technology (此芯科技)

Series B, ¥1 billion (~$140M), ¥8 billion valuation (~$1.1B)

ARM-compatible AI chips for PCs and edge devices.

CIX Technology builds ARM-compatible AI chips for PCs and edge devices. CEO Hank Sun was AMD’s SOC director and head of AMD’s China semiconductor business. CTO Fang Liu spent 11 years at Apple on CPU/GPU architecture, then SOC work at Meta and AMD. That concentration of semiconductor talent in a single founding team is rare. Their CIX P1 chip (6nm, 12-core ARM CPU, 30 TOPS NPU, 45 TOPS combined with CPU and GPU) is already in Minisforum mini PCs shipping to consumers.

China’s semiconductor conversation has been dominated by datacenter GPUs, the race to replace Nvidia H100s. CIX is playing a different field: the billions of edge devices that need local AI inference without a data center connection. Qualcomm’s Snapdragon X competes in the same space globally; the P1 is one of the first Chinese-designed chips to reach commercial production with OEM partnerships.

Shanghai Integrated Circuit Industry Investment Fund (上海集成电路产业投资基金) and Pudong Venture Capital (浦东创投) co-led, with Oriza Ventures (元禾璞华), Lenovo Ventures, and others.

Breaking Shell Robotics (破壳机器人)

Angel, tens of millions of USD, ¥2.6 billion valuation (~$360M)

Home robots. That is nearly everything publicly known about this company.

The founder is Xu Huazhe (许华哲), a Tsinghua assistant professor who co-founded Galaxea AI and served as its Chief Scientist before leaving in February 2026. Galaxea provided the seed investment. That pedigree explains the ¥2.6 billion valuation at angel stage with almost no public information: investors are backing the person, not a product.

Xu laid out his thesis at the Zhongguancun Forum on March 29. Breaking Shell will build its own hardware (vertical integration, not outsourced bodies) and focus on a narrow set of household tasks rather than chasing full generalization. Object passing and tidying first, then storage and cleaning. Cooking will appear as demos but not as a product. No physical contact tasks (elderly care, childcare) for now. The bet is that defining 10 tasks precisely and collecting targeted data will scale faster than building a 21-degree-of-freedom generalist that can’t do any single task reliably.

Also on the Radar

Unitary Quantum (幺正量子) — Pre-A, hundreds of millions of RMB, ¥1.5 billion valuation. Ion trap quantum computing out of Hefei. Geely (automaker) and Ant Group (fintech) co-led. An unusual investor pairing that suggests quantum is entering the strategic planning of companies far outside the usual deep tech investor base.

SpinQ (量旋科技) — Series C+, ¥600 million (~$83M), ¥3 billion valuation. Superconducting and NMR quantum computers already shipping to 200+ institutions across 40+ countries. Revenue hit ¥50 million in 2024. The most commercially mature quantum company in China, possibly in Asia.

JAKA Robotics (节卡机器人) — Series E, ¥6 billion valuation. Collaborative robots deployed in 100+ countries with offices in Japan, Germany, the US, Malaysia, and Singapore. Customers include Toyota and Schneider Electric. 21.9% of China’s cobot market. Shanghai-based.

EPG (易普集) — Series B+, $100 million, ¥3.9 billion valuation. Prefabricated modular data centers. Alibaba Cloud and Decarbonization Partners (BlackRock/Temasek JV) co-invested. Offices across Southeast Asia, the Middle East, and Europe. One of the few companies in this dataset already operating globally.

Mingshi BCI (明视脑机) — Angel, ¥150 million (~$21M), ¥750 million valuation. Invasive brain-computer interface for neural applications. Backed by 中科创星 (CASSTAR). China approved its first commercial BCI implant in March 2026 (Neuracle Technology, for paralysis patients), and capital is following.

Bowintec (博银合创) — Series A, undisclosed amount. Dexterous robotics. The sole investor: Bosch China. A sole bet from a German industrial giant on a Chinese dexterous robotics startup.

RoboParty (萝博派对) — Angel, $20 million, ¥715 million valuation. Humanoid bipedal robots. Guoxiang Capital (国香资本) and Matrix Partners China (经纬创投) co-led. Limited public information, but top-tier VC confidence at angel stage.

Lingravity (零重力飞机工业) — Pre-B, ¥150 million (~$21M), ¥4.5 billion valuation. eVTOL aircraft plus electric fixed-wing (RX1E, already certified for commercial delivery). Led by Xiang Jinwu, a Chinese Academy of Engineering academician. Team from AVIC and COMAC. Xichuang Investment (锡创投), Huikai Investment (惠开投资), and Jinpu Investment (金浦投资) among investors. Based in Hefei with R&D in Nanjing, Shenzhen, and Wuhu.

快酷创新 — Series A, undisclosed. Smart self-service haircutting devices. Investors: Hillhouse Capital (高瓴创投) and MiraclePlus (奇绩创坛). Hillhouse backing an automated barber is the most unexpected bet in a dataset dominated by chips and humanoids.

Differential Robotics (微分智飞) — Series A, hundreds of millions of RMB, ¥2.6 billion valuation. Intelligent drone swarm systems for industrial and urban inspection. Founded July 2024. Huakong Fund (华控基金) led, with Baidu Ventures and others. Nine months from founding to a ¥2.6 billion valuation.

The Bigger Picture

China’s quantum moment

Three quantum computing deals totalling over ¥1.6 billion in disclosed funding, each using a different technological approach: photonic (QBoson), superconducting/NMR (SpinQ), and ion trap (Unitary Quantum). That spread suggests a coordinated infrastructure build across all three major technological approaches.

China’s public quantum funding stands at an estimated $15 billion, nearly four times the U.S. government’s $4 billion. Late last year the State Council launched the National Venture Capital Guidance Fund, seeding ¥121.8 billion across three regional funds covering frontier tech from AI to quantum to 6G, with a target scale of ¥1 trillion. The new signal is who’s writing the checks. ICBC’s investment arm leading QBoson’s round. Geely and Ant Group co-leading Unitary Quantum. ICBC is China’s largest state bank. Geely makes cars. Ant Group runs payments. None of them are specialist deep tech investors. Their presence in the same technology category in the same week points to broad institutional conviction (or FOMO), the kind that precedes large procurement and deployment decisions.

SpinQ’s numbers add context: ¥50 million in revenue in 2024, a chip already shipped to the Middle East. Parts of this are already commercial.

The billion-dollar angel

Multiple companies in this dataset hit billion-RMB valuations at angel or seed stage with minimal or no shipped products. Breaking Shell Robotics at ¥2.6 billion. MOSI Intelligence at ¥1.5 billion. Differential Robotics at ¥2.6 billion (see Also on the Radar).

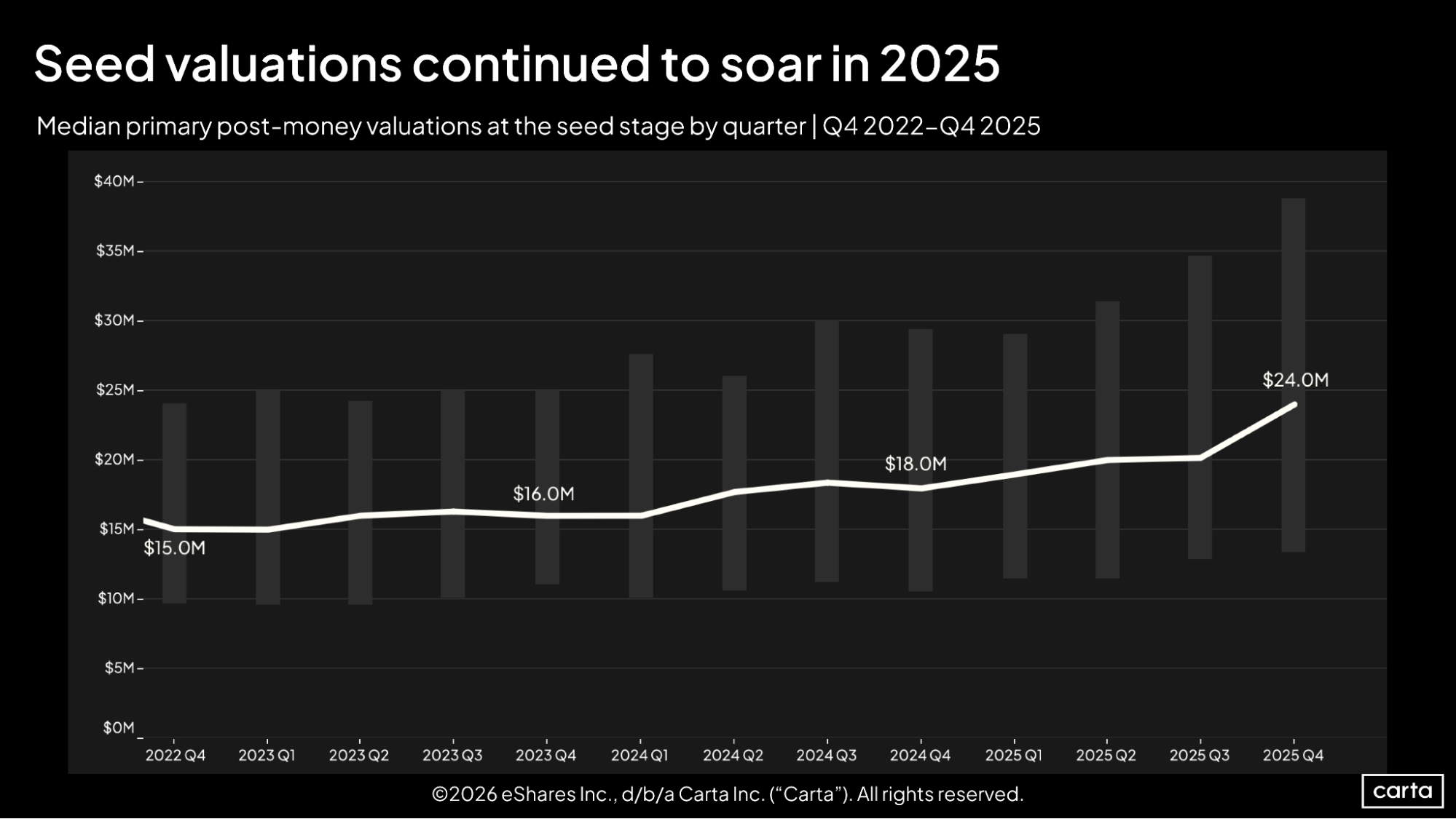

The pattern extends beyond China. Globally, AI seed-stage companies now command a 42% valuation premium over non-AI startups. Even across all sectors, Carta data shows US median seed valuations up 60% in three years to $24 million.

Breaking Shell hit ¥2.6 billion (~$360 million) at angel stage. That’s 15x the US median seed, for a company with no public product. Breaking Shell’s valuation is entirely a bet on Xu Huazhe’s Tsinghua/Galaxea track record. MOSI’s is a bet on Qiu Xipeng’s MOSS lineage. Differential’s is a bet on the team behind it, nine months in.

The question is whether these valuations reflect genuine conviction in specific teams (the Kunlun Xing model: two resumes, no product, $1 billion in 10 days) or whether capital is chasing sector allocation targets, and the honest answer is probably both operating simultaneously.

Robotics: the 2021 autonomous driving moment

27 robotics deals in seven days. By industry estimates, the sector has grown from roughly 120 companies to over 320 in three years. Per the China Academy of Information and Communications Technology, embodied intelligence recorded ¥73.5 billion in financing across 740+ deals in 2025. At least six startups secured $100 million or more in early 2026 alone.

Chinese media has started drawing the comparison to autonomous driving’s 2021 peak, when hundreds of AD companies raised billions before the market consolidated violently. The NDRC has warned about a bubble, flagging “low-level duplication” across 150+ companies chasing immature technology routes and unclear commercialization models. The NEV precedent is instructive: roughly 400 Chinese EV companies ceased operations between 2018 and 2025, leaving around 100 active, with McKinsey projecting fewer than 50 by 2030. A similar shakeout looks likely here.

The data this week supports the saturation thesis. Eight of the 27 robotics deals are embodied AI or humanoid plays. Most are at angel or Pre-A stage. Most have undisclosed amounts. The long tail is getting very long.

The counter-signal is the industrial layer. Companies like JAKA Robotics (cobots, E round, 100+ countries) and Bowintec (Bosch’s sole bet) suggest that the industrial robotics layer, the unglamorous part, is maturing separately from the humanoid hype cycle. The companies building components, sensors, and motion control systems may benefit regardless of which humanoid companies survive.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete.