The China Round — July 10, 2026

Lab-grown leather for luxury brands, an AI drug designed for $23 million, and a new rule that lets technology in but not out

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

Happy Friday. China’s first unified outbound investment regulation took effect on July 1, restricting how technology can leave the country. The same week, 141 deals closed across seven sectors. More on those rules below.

Where the Money Went

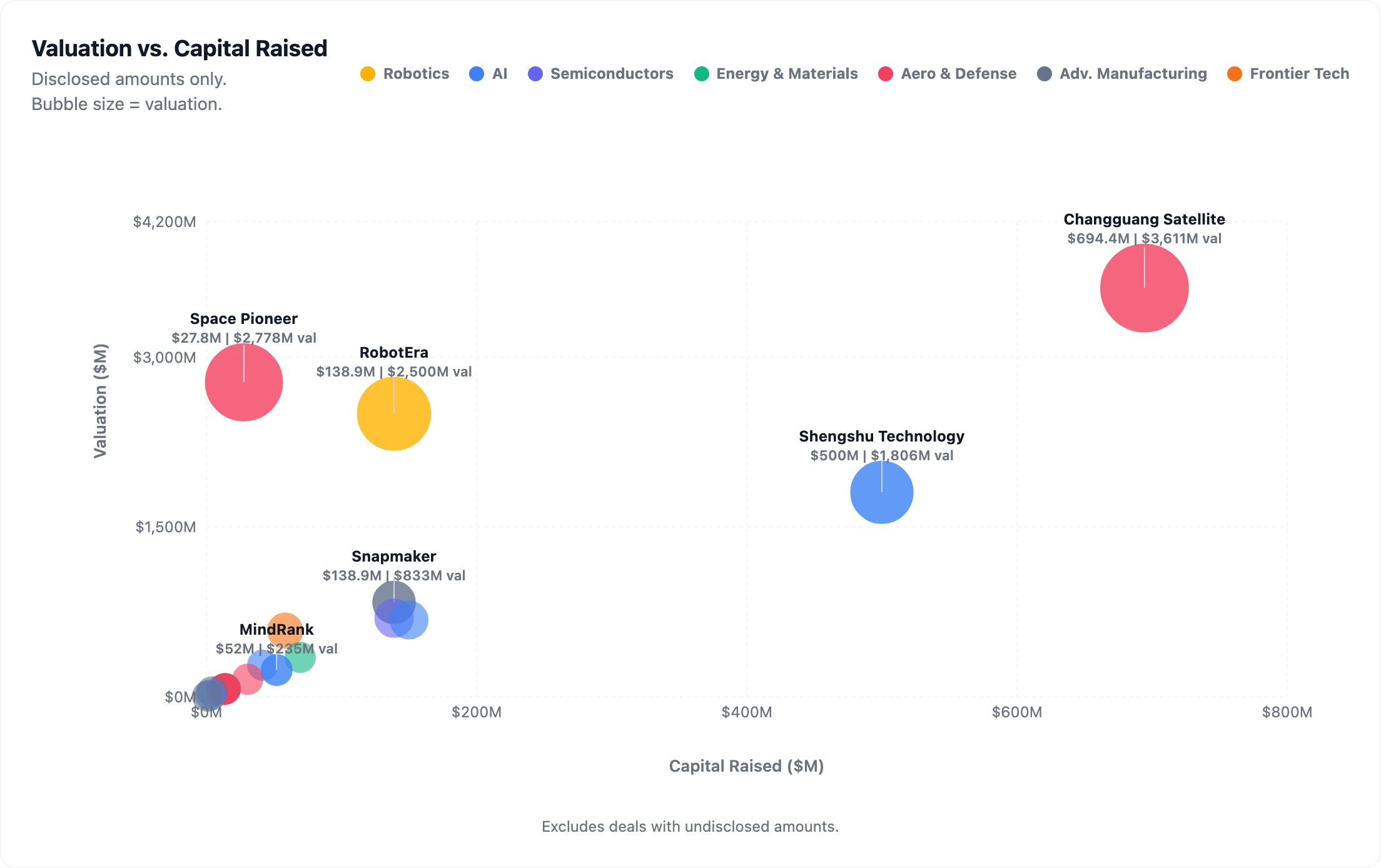

141 deals across seven sectors. 24 disclosed exact amounts, totaling $2.2 billion (~¥15.6B), with most of the capital concentrated in a satellite mega-round and several hundred-million-dollar AI raises.

🧠 AI (26 deals)

Shengshu Technology (生数科技) closed a $500 million (~¥3.6B) B+ round for Vidu, its AI video platform. Tripo AI raised $150 million (~¥1.08B) in an A+ round for AI-generated 3D assets, its third raise in four months. DeepCtrls (深度智控) pulled in hundreds of millions of RMB with Jinko Solar as a strategic investor (covered below). MindRank (德睿智药) raised $52 million (~¥374M) for AI drug discovery, with its lead candidate now in Phase III (covered below). Below the growth rounds, a cluster of Pudong-backed seed and angel deals continued Shanghai’s pattern of systematic early-stage deployment.

⚡ New Energy & Materials (23 deals)

Starchens (星辰新能) led the sector with a ¥500 million (~$69M) B round backed by CITIC Securities Capital, ICBC Capital, and East Money, a lineup of securities and bank-affiliated investors more typical of pre-IPO rounds. The rest split between battery materials, hydrogen, energy storage, and specialty chemicals, with state-linked capital from Hefei, Nanjing, and Jiangsu backing early- and growth-stage rounds.

🔬 Semiconductors (22 deals)

Twenty-two deals, nearly all with undisclosed amounts. Sicreat (新美光) closed a ¥1 billion (~$139M) C+ round for CMP (chemical-mechanical planarization) polishing pads, a key semiconductor consumable (more below). EDA (chip design software), chiplet packaging, and optoelectronic chips each drew a handful of deals. Several semiconductor materials companies are raising in Suzhou, continuing that city’s emergence as a vertically integrated chip-materials cluster.

🤖 Robotics (18 deals)

RobotEra (星动纪元) closed a ¥1 billion (~$139M) B round led by Chengtong, a fund under SASAC (China’s state-asset regulator), part of ¥2.5 billion (~$347M) raised across three rounds in roughly 60 days. Morphi (墨奇智能) pulled in hundreds of millions of RMB in what is reportedly one of the largest disclosed angel rounds in China’s embodied-AI sector (AI designed to operate physical hardware like robots), with Alibaba and Tencent co-anchoring for a six-month-old company. Motorevo (泉智博) completed its seventh round in 18 months for humanoid robot joint modules.

💡 Frontier Tech (8 deals)

Two brain-computer interface companies raised in the same week: Gestala (格式塔科技), a non-invasive ultrasound BCI startup, closed a ¥442 million (~$61M) angel+ round (covered below), while NeuroXess (脑虎科技) raised an A+ round as it began Class III clinical trials at Huashan Hospital. QBoson (玻色量子) closed a Pre-IPO round and filed for IPO coaching (the formal process of engaging an underwriter to prepare a company for listing) three days later. SynMetabio (贻如生物), a synthetic biology company making cultivated leather for luxury brands, closed its A round with Ordos Group co-leading (covered below).

🚀 Aerospace & Defense (16 deals)

Changguang Satellite (长光卫星) dominated with a ¥5 billion (~$694M) strategic round, the largest single raise in the sector this week. The company operates 161 satellites, the world’s largest sub-meter-resolution commercial remote-sensing constellation. Space Pioneer (天兵科技) added ¥200 million (~$28M) in strategic capital. Kaipu Dynamics (开普动能), an eVTOL (electric vertical takeoff and landing) electric propulsion startup founded by a former Rolls-Royce division director, raised an angel round (covered below). Most of the remaining deals were seed and angel rounds for early-stage space-tech and low-altitude economy startups, including Ruiqi Deep Space (瑞启深空), a four-month-old constellation startup that raised ¥220 million (~$31M) at a ¥1.1 billion (~$153M) valuation from Suzhou state funds.

⚙️ Other Adv. Manufacturing (28 deals)

Snapmaker (快造科技) raised ¥1 billion (~$139M) in a C round for consumer 3D printing (covered below). CLAWLAB (浪爪智能) raised hundreds of millions of RMB with miHoYo leading (covered below). Thinkhead (上海星合), a 17-year-old bootstrapped machine-tool manufacturer, took its first outside capital. Coffee robot maker InSpace/XBOT (影智科技) closed a B round. The rest spanned optics, precision measurement, industrial equipment, and microfluidics (tiny channels etched into chips to manipulate fluids for medical diagnostics and lab work).

Spotlight

Gestala (格式塔科技)

Angel+, ¥442M (~$61M), Valued at ¥4.2B (~$583M)

Non-invasive ultrasound brain-computer interface.

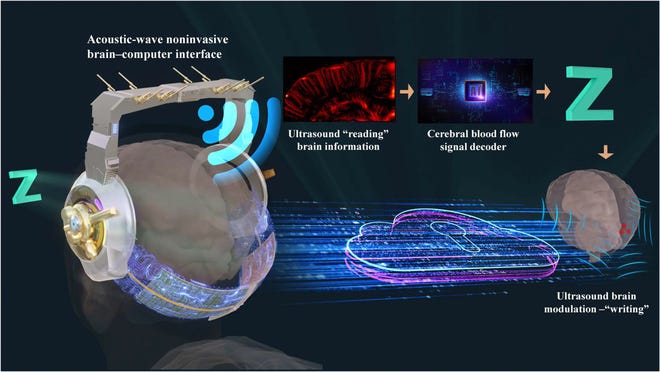

Gestala was founded on January 1, 2026 by Peng Lei, who left NeuroXess (脑虎科技), the invasive BCI company he co-founded and ran as CEO, in late 2025. Six months later, he has raised a cumulative ¥570 million (~$79M) across two rounds for an entirely different approach: instead of implanting electrodes in the brain, Gestala uses focused ultrasound to read and modulate neural signals through the skull. The company has completed over 30 clinical cases targeting chronic pain, reporting 50% pain reduction. It aims to file for NMPA (China’s National Medical Products Administration, the equivalent of the US FDA) medical device registration by year-end, with certification likely around 2028.

Acoustic-wave noninvasive brain-computer interface. Source: Zheng et al., Research (2023), DOI: 10.34133/research.0200. CC BY 4.0.

Chen Tianqiao (陈天桥), the Shanda Interactive founder who has spent the past decade funding neuroscience research through his Tianqiao and Chrissy Chen Institute, holds 25% equity through Shengda Cognition. In the US, Sam Altman-backed Merge Labs raised $250 million at an $850 million valuation four months ago, pursuing the same ultrasound-BCI thesis. The same week as Gestala’s round, Peng Lei’s former company began invasive human clinical trials at Huashan Hospital in Shanghai.

Huaying Capital (华映资本, lead), C Capital, and 11 others participated.

Snapmaker (快造科技)

C Round, ¥1B (~$139M), Valued at ¥6B (~$833M)

Consumer 3D printers and desktop fabrication tools.

Snapmaker makes multi-function desktop machines that combine 3D printing, laser engraving, and CNC carving. The company has shipped over 100,000 units across 80+ countries, with the majority of revenue from overseas. Its U1 model set a Kickstarter crowdfunding record for the 3D printer category, raising ¥47 million (~$6.5M) in 12 hours and ¥150 million (~$20.6M) over the full 43-day campaign, with more than 20,000 backers. Revenue grew 10x year-on-year on the back of the U1.

The Snapmaker U1 mid-print. Source: Snapmaker.

The round was led by Cathay Capital (凯辉基金), a new investor, with existing backers Hillhouse, Meituan, and Shunwei over-subscribing at scale. TAL Education’s (好未来) venture arm also joined as a new entrant. This is the largest single financing in consumer-grade 3D printing in at least the past two years, putting Snapmaker’s valuation at ¥6 billion (~$833M).

Its direct competitor Bambu Lab (拓竹) was valued at over ¥10 billion (~$1.4B) after its 2024 C round, putting two consumer 3D-printing companies above $800 million in the same cycle. Snapmaker’s edge is hardware pedigree: founder Chen Xuedong (陈学栋) is a mechanical engineering graduate who worked at AECC’s Xi’an Aero-engine Research Institute before starting the company in 2016.

MindRank (德睿智药)

B Round, $52M (~¥374M), Valued at ¥1.69B (~$235M)

AI-powered drug discovery, with China’s first AI-designed drug to reach Phase III.

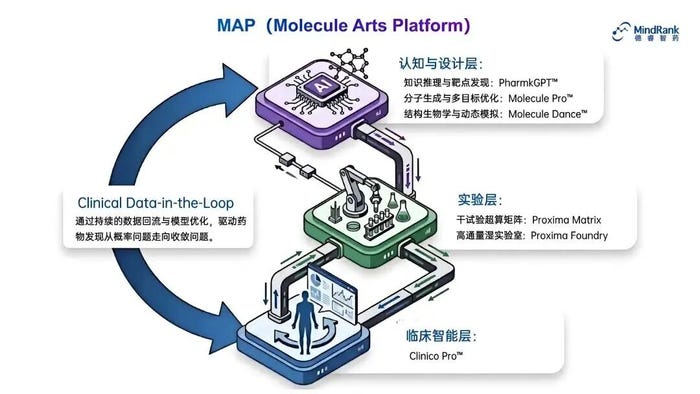

MindRank uses AI to design drug molecules from scratch, then develops them through clinical trials. Its lead candidate, MDR-001, is an oral GLP-1 receptor agonist for weight loss, directly comparable to Eli Lilly’s orforglipron, one of the most closely watched drugs in global pharma. GLP-1 drugs (the class that includes Ozempic and Mounjaro) work by mimicking a hormone that tells the brain you’re full; most are injections, and the race to make an effective pill form is worth hundreds of billions in potential revenue. In January 2026, MDR-001 became the first AI-designed Category 1 new drug (China’s highest regulatory classification for an original compound) in China to enter Phase III clinical trials, with roughly 750 subjects.

MindRank’s Molecule Arts Platform (MAP): three-layer architecture spanning AI molecular design, automated wet-lab validation, and clinical intelligence. Source: MindRank / Sina

MindRank took MDR-001 from initiation to Phase III in about 4.5 years for approximately $23 million (~¥165M). Traditional drug development for a comparable molecule typically costs $300 to $400 million over 7 to 9 years. The company says AI cut its R&D costs by more than 60%, with the rest of the advantage coming from running a 40-person startup rather than a large pharmaceutical operation. The Hangzhou-based team holds 15 drug pipelines, 5 preclinical candidates, and 3 IND (Investigational New Drug, the approval required before human trials can begin) approvals, including a US FDA IND from December 2022.

Xeno Investment (谢诺投资) and SWS Capital (申银万国投资) participated.

CLAWLAB (浪爪智能)

Pre-A (cumulative hundreds of millions RMB across multiple tranches)

AI-powered textile machines that turn a photo into a finished tufted textile.

CLAWLAB builds machines that use AI to convert a photograph or sketch into a pattern, then physically tuft it into fabric. Tufting is the process of pushing yarn through a backing material to create carpets, rugs, and textured textiles. The consumer textile-machine category has seen little new product development in decades. Founder Hu Wenxin (胡文鑫) previously built products at DJI and Meituan before starting CLAWLAB in Shenzhen in December 2022. The company’s first product, a consumer tufting gun, generated roughly ¥100 million (~$14M) in revenue over its first two years.

CLAWLAB’s AI-powered tufting gun with a finished textile piece. Source: CLAWLAB

miHoYo (米哈游), the Shanghai gaming studio behind Genshin Impact and Honkai: Star Rail, led the Pre-A3 tranche. miHoYo has been systematically investing in physical-world AI and robotics, and CLAWLAB’s AI-to-physical pipeline, converting digital designs into manufactured textiles, fits that thesis directly. Earlier tranches were led by Yuanjing Capital (元璟资本) and Sequoia China’s seed fund. Shunwei Capital also participated. The cumulative funding across tranches is in the hundreds of millions of RMB.

SynMetabio (贻如生物)

A Round, over ¥100M (~$14M), Valued at ¥1.5B (~$208M)

Cultivated leather made with synthetic biology, already selling to European luxury brands.

SynMetabio engineers microorganisms at the gene level to produce bio-based leather materials with an 80% lower carbon footprint than traditional leather. A ShanghaiTech University spinout based in Shanghai’s Zhangjiang tech district, the company already has a French subsidiary (SYNMETABIO, based in Lyon) and reports that international orders, predominantly from luxury brands, account for roughly two-thirds of its business, with total orders approaching ¥100 million (~$14M). SynMetabio has also partnered with Anta, the Chinese sportswear brand, for three co-branded shoe drops (April 2025, November 2025, March 2026). The team has grown from 20 to 70 people, and its manufacturing capacity through joint-venture partners reaches 16 million square meters per year.

ANTA x Kris Van Assche sneaker made with SynMetabio’s Mulkol mycelium leather, launched at Dover Street Market Paris. Source: SynMetabio

Ordos Group (鄂尔多斯集团), the Inner Mongolian conglomerate known primarily for cashmere and coal, co-led the round with Heda Jinfu (和达金服). Ordos is actively diversifying into what China calls “new-quality productive forces” (新质生产力, a government term for advanced manufacturing and frontier technology sectors). Backing a synthetic biology company that could eventually supply bio-based alternatives to its own textile operations is a strategic hedge. SynMetabio’s CEO has publicly stated that 2026 is “year one of IPO preparation.”

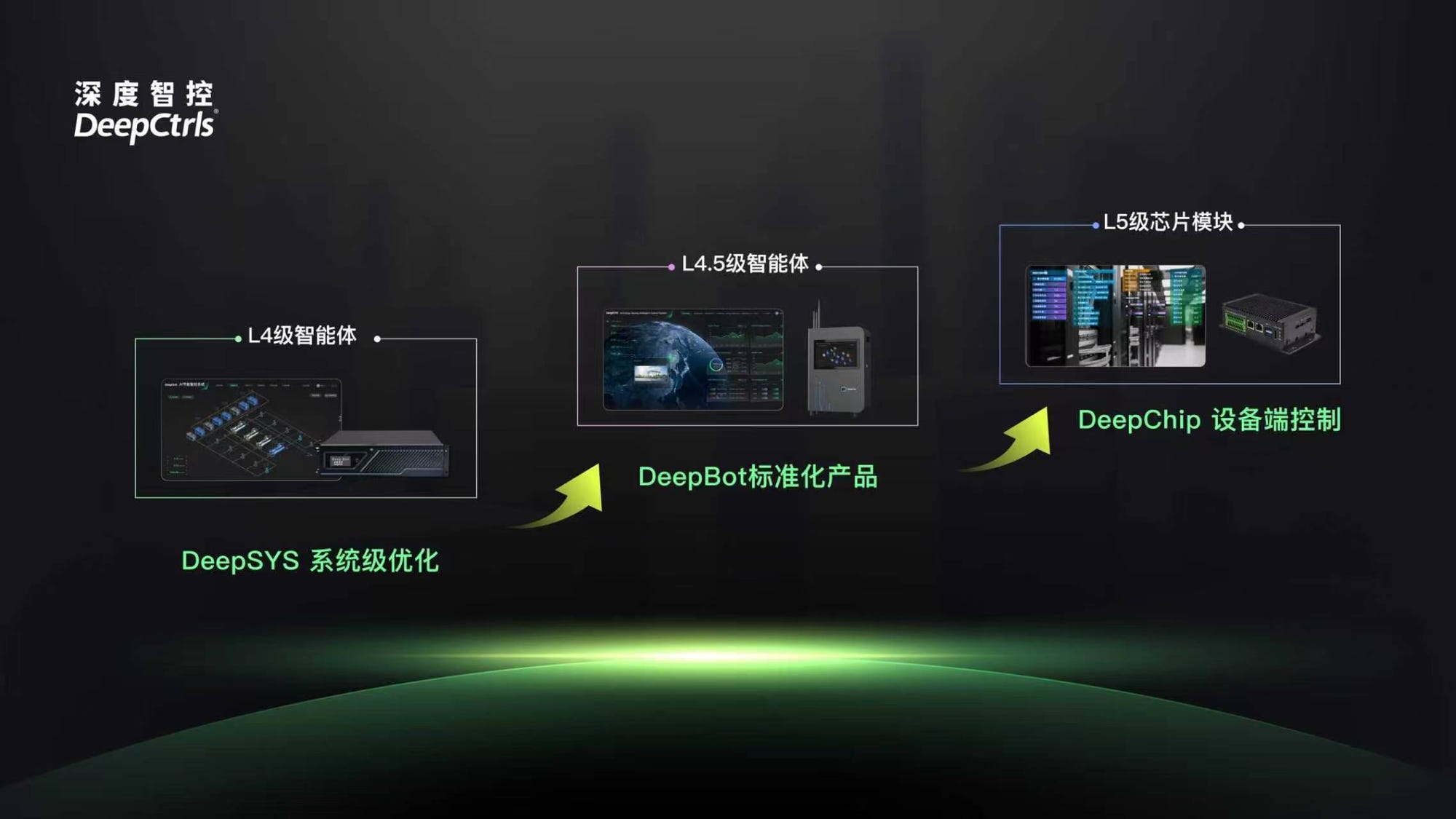

DeepCtrls (深度智控)

B Round, hundreds of millions RMB, Valued at ¥3B (~$417M)

Physical AI that optimizes energy infrastructure, already profitable.

DeepCtrls builds what it calls a “PhyAI” engine: physics-coupled AI models that learn the behavior of electromechanical systems (motors, compressors, cooling units, solar inverters) and optimize them in real time. Where most AI companies sell software to software companies, DeepCtrls sells software to factories, data centers, and power plants. The Nanjing-based company, founded by a team from Tsinghua University and Lawrence Berkeley National Laboratory, reports over 300,000 devices deployed, customers including TSMC, CXMT, Innolight, Foxconn Industrial Internet (FII/工业富联), Tencent, ByteDance, and CATL, and operations in more than 10 countries. Revenue is doubling year-on-year, and the company says it has been profitable since last year.

DeepCtrls product architecture: DeepSYS (system-level optimization), DeepBot (standardized edge products), and DeepChip (device-level control modules). Source: DeepCtrls

Jinko Solar (晶科能源), one of the world’s largest solar panel manufacturers, came in as a strategic investor. SDIC Innovation (国投创新) and CMB International (招银国际) co-led. Sequoia China, Source Code Capital, and GLP Capital continued from earlier rounds. This is the company’s sixth round.

Kaipu Dynamics (开普动能)

Angel (seed + angel combined), tens of millions RMB

Electric propulsion systems for eVTOL aircraft, built by a team that used to make them at Rolls-Royce.

Kaipu Dynamics was founded in 2026 by Zhang Qinyin (张嶔崟), who previously directed Rolls-Royce’s electric fixed-wing division, leading the Tecnam P-Volt and MDA1 EViator nine-seat electric aircraft programs. His two co-founders were chief engineers in Rolls-Royce’s UAM (Urban Air Mobility) and RAM (Regional Air Mobility) divisions. The company’s motor is rated at 130kW continuous (204kW peak), roughly the output of a mid-size car engine, with motor weight 20 to 30 percent lighter than comparable products. The team also includes senior low-altitude technology and airworthiness specialists from COMAC, China’s state aircraft manufacturer.

The Tecnam P-Volt, a nine-seat all-electric passenger aircraft whose propulsion system was developed under Kaipu Dynamics founder Zhang Qinyin’s Rolls-Royce division. Source: Tecnam

Rolls-Royce announced its exit from civil electric propulsion in November 2023 and shut down its electric propulsion unit in 2024 after failing to find a buyer, terminating contracts with Vertical Aerospace and Tecnam. The team that built those systems now sits in Quanzhou, Fujian, developing the same technology for China’s eVTOL market, which got a regulatory boost when a revised Civil Aviation Law took effect on July 1, 2026, writing “low-altitude economy” (低空经济) into national law for the first time. In June, AECC rolled out China’s first domestically built eVTOL engine. A Western company exits, its technical team migrates, and the receiving country builds the regulatory and manufacturing infrastructure to absorb the capability.

Led by Zero Capital (零以创投), with Xinding Capital (新鼎资本) following. Wealthfast Capital (唯快资本) served as financial advisor.

Also on the Radar

Motorevo (泉智博). A+++ round, tens of millions RMB, valued at ¥2B (~$278M). Builds joint modules for humanoid robots. This is the company’s seventh round in 18 months, led by Hillhouse’s GL Ventures (高瓴创投). Zhiyuan (智元机器人) and LinkerBot (灵心巧手), two humanoid-robot manufacturers, invested as strategic shareholders. Robot makers buying equity in their own component suppliers. H1 2026 shipments hit 120,000+ units, with 60,000+ in June alone.

RobotEra (星动纪元). B round, ¥1B (~$139M), valued at ¥18B (~$2.5B). Humanoid robot maker that has raised ¥2.5 billion (~$347M) across three rounds in roughly 60 days, with SASAC’s Chengtong Fund leading the latest. Shipping dexterous hands at thousand-unit scale to logistics customers processing 1,200+ packages per hour across five provinces. About 50% of revenue comes from overseas.

Shengshu Technology (生数科技). B+ round, $500M (~¥3.6B), valued at ¥13B (~$1.8B). Founded by Tsinghua AI professor Zhu Jun (朱军), chief scientist at the Beijing Academy of Artificial Intelligence. Builds “world models,” AI systems that don’t just generate video but attempt to simulate physics. Two rounds totaling ¥5.4 billion (~$750M) in three months. Vidu platform serves 195+ countries and 4.2 million+ creators.

Morphi (墨奇智能). Angel series, hundreds of millions RMB, valued at ¥7B (~$972M). One of the largest angel-round financings in China’s embodied-AI sector, with Alibaba and Tencent co-anchoring for a company that is roughly six months old. Founded by an ex-Huawei “Genius Boy” (天才少年, a title Huawei gives to its top young recruits) and a Huawei veteran who co-founded iMile, a Middle Eastern logistics company. A pure conviction bet on team pedigree, with zero disclosed product traction.

Thinkhead (上海星合). A round, hundreds of millions RMB, valued at ¥1.5B (~$208M). A 17-year-old, profitable, bootstrapped machine-tool manufacturer taking its first-ever outside capital. Led by Wuliangye Fund (五粮液, the baijiu distiller), with Magmeet (麦格米特) following. The company says it is the domestic leader in form gear grinding machines, a precision manufacturing process used in automotive drivetrains, with over 1,000 customers it says include BYD, SAIC, and Geely. Its machines meet GB Class 1 precision, the highest accuracy grade in China’s national standards for grinding equipment.

InSpace/XBOT (影智科技). B round, hundreds of millions RMB, valued at ¥1.5B (~$208M). Makes autonomous coffee robots deployed in 22+ countries across 100+ cities, with over 1,000 units producing 4 million+ cups. Founded by a former Xiaomi VP, with reported angel backing from Zhang Xiaolong (张小龙), the creator of WeChat. Head-to-head with Kaye Technology (咖爷科技), which raised a comparable amount from Hillhouse and Meituan last month.

Changguang Satellite (长光卫星). Strategic round, ¥5B (~$694M), valued at ¥26B (~$3.6B). Operates 161 satellites, the world’s largest sub-meter-resolution commercial remote-sensing constellation. Investors include Changchun Development Group (长发集团), China Orient Asset Management (东方资产), and Lushi Investment (陆石投资). State-backed capital anchoring a strategic satellite asset ahead of a likely IPO.

QBoson (玻色量子). Pre-IPO, hundreds of millions RMB, valued at ¥10B (~$1.39B). Builds quantum computers that use photons (particles of light) instead of supercooled circuits to perform calculations. Closed its Pre-IPO round on July 3, then filed for IPO coaching with Guotai Junan Securities on July 6, three days later. The second pure-play quantum computing startup to begin IPO coaching, after Origin Quantum (本源量子) in September 2025. More in the IPO Factory theme below.

Sicreat (新美光). C+ round, ¥1B (~$139M), valued at ¥5B (~$694M). Makes CMP polishing pads, the consumable discs that flatten silicon wafers between fabrication steps. Led by Yuanhe Holdings (元禾控股), with Zhongping Capital (中平资本) and China Post Capital (中邮资本). Suzhou-based, part of the city’s growing semiconductor-materials cluster.

Starchens (星辰新能). B round, ¥500M (~$69M), valued at ¥2.5B (~$347M). New energy materials company whose investor syndicate (CITIC Securities Capital, ICBC Capital, East Money) looks less like a growth round and more like a pre-IPO pipeline. More in the IPO Factory section.

Guangyin Tech (光引科技). Pre-A round, ¥100M (~$14M), valued at ¥500M (~$69M). Builds spectroscopy instruments (devices that analyze materials by measuring how they interact with light). Led by Henan Gaochuang (河南高创), with CAS Star (中科创星), Xi’an Caijin (西安财金), and others. Notable for attracting state capital from multiple provinces into an early-stage round for hard-science instrumentation.

The Bigger Picture

The IPO Factory

On June 17, the Shanghai Stock Exchange issued Guidance No. 10, expanding the STAR Market’s (Shanghai’s Nasdaq-equivalent board for science and technology companies) “fifth listing standard.” This standard allows companies with no profits and no revenue to list, provided they meet a market cap threshold (¥4 billion / ~$556 million) and hold government-recognized core technology. The new guidance adds detailed review criteria for AI large-model companies, and a parallel update to the strategic-emerging industry catalogue named quantum computing, brain-computer interfaces, robotics, hydrogen energy, embodied intelligence, and 6G as priority sub-industries for listing.

The STAR Market (科创板) at the Shanghai Stock Exchange. Source: Caixin

QBoson (玻色量子) closed its Pre-IPO round on July 3 and filed for IPO coaching three days later, the second Chinese quantum company to do so after Origin Quantum in September 2025. Starchens’ ¥500 million B round drew CITIC Securities Capital and ICBC Capital, both of which have PE subsidiaries that routinely take pre-IPO stakes in companies their parent institutions later underwrite. Changguang Satellite’s ¥5 billion round came from overlapping state investors. SynMetabio’s CEO publicly framed 2026 as “year one of IPO preparation.”

CXMT (长鑫科技), China’s largest DRAM (dynamic random-access memory, the main working memory in phones and computers) chipmaker, opens subscriptions for its STAR Market IPO on July 16, targeting a raise of ¥29.5 billion (~$4.3 billion). Its Q1 results: revenue of ¥50.8 billion (~$7.1B), up 719% year-on-year, net profit of ¥33 billion (~$4.6B). All five major bank asset-investment companies (ICBC, Agricultural Bank of China, Bank of China, CCB, and Bank of Communications) hold stakes.

In H1 2026, bank-affiliated investment firms collectively backed 58+ hard-tech projects. STAR Market listings in the first half of 2026 rose 57% year-on-year to 11, with total IPO fundraising up 148%.

China is building a structured pipeline from venture capital to public markets for specific technology categories. The listing standards define which technologies qualify. The bank and securities PE arms invest early, building positions in companies their parent institutions will later underwrite. QBoson went from round close to IPO coaching filing in three days, following a conveyor belt that runs from angel round to public listing.

The One-Way Membrane

On July 1, State Council Decree 837 took effect, China’s first unified regulation on outbound investment. Article 13 bans transferring state-restricted or prohibited technology abroad by any means, including cross-border dispatch of technical personnel, organizing staff to work overseas, cross-border technical guidance, or cross-border training. The penalties under Article 27 include confiscation of illegal gains and fines of up to 1% of the offending outbound investment. Article 28 adds a ban on new outbound investment activity for one to three years.

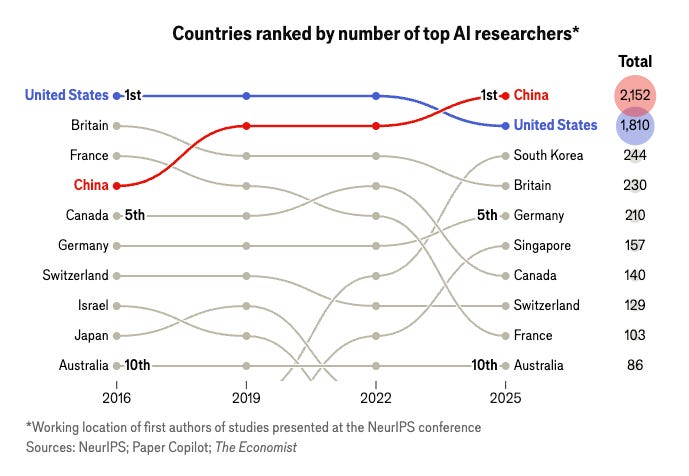

Countries ranked by number of top AI researchers at NeurIPS. China overtook the US for first place by working location of lead authors. Source: NeurIPS, Paper Copilot, The Economist

Less than three weeks before Decree 837 took effect, the Ministry of Commerce, NDRC, and Ministry of Finance jointly issued a Foreign Investment Stabilization Action Plan (June 16, publicly released June 22). Among its 15 measures: improved support for foreign R&D centers in China, streamlined entry for high-level foreign talent, and a provision allowing qualified foreign-invested companies to raise capital through domestic listings. In October 2025, China introduced the K-visa, a five-year, multiple-entry visa for STEM graduates and researchers from recognized institutions, with no domestic employer required.

Technology flows in, but not out. The mechanism is talent. Kaipu Dynamics was founded by a team that built electric aircraft propulsion systems at Rolls-Royce in the UK, which exited the business entirely. DeepCtrls was founded by a team from Tsinghua and Lawrence Berkeley National Laboratory. QBoson’s founder has a Stanford pedigree.

The talent pipeline extends beyond this week’s deals. An Economist analysis of NeurIPS 2025 found that the share of overseas-trained Chinese AI researchers who returned to China rose from 12% in 2019 to 28% in 2025. The Financial Times reported that three AI headhunters operating between China and San Francisco helped relocate more than 30 US-based researchers to China in the past year alone.

Two policies, opposite in direction, working in concert. One locks the door on outbound tech transfer. The other opens it for inbound talent and capital.

Supply-Chain Strategic Investing

Three deals this week share an unusual investor pattern. The lead investor in each is not a financial institution but a non-financial company that is also, or intends to become, a customer or supply-chain partner of the company it’s backing.

Jinko Solar’s production line in Chuzhou, Anhui. The solar manufacturer invested as a strategic backer in DeepCtrls this week. Source: Xinhua / Lu Hua

Ordos Group (鄂尔多斯集团), an Inner Mongolian conglomerate built on cashmere and coal, co-led SynMetabio’s A round.

Ordos has been diversifying into “new-quality” industries, and its 2025 annual report shows the company developing a synthetic biology project at its Qipanjing industrial base intended to integrate with its existing cashmere and chemical businesses. It’s backing a bio-leather company that could eventually supply alternatives to its own textile operations.

Jinko Solar (晶科能源), one of the world’s largest solar manufacturers, invested as a strategic investor in DeepCtrls’ B round. DeepCtrls’ physical AI engine optimizes the exact electromechanical systems that Jinko’s factories run on.

And in robotics, Zhiyuan (智元机器人) and LinkerBot (灵心巧手), two humanoid-robot end-product manufacturers, took equity in Motorevo (泉智博), their own joint-module supplier. As reported by Cailianshe, Zhiyuan is planning to produce tens of thousands of humanoid robots in 2026 and is already integrating Motorevo’s modules into one of its largest product lines. LinkerBot, which reports holding over 80% of the global dexterous-hand market, plans to bundle joint modules with its hands for integrators.

In all three cases, the capital comes with a purchase order. These companies are investing in their own supply chains, locking in access to components and capabilities they need to scale. In a market where H1 2026 embodied-AI funding alone totaled ¥93.5 billion (~$13B, up 5x year-on-year across 322 deals), the companies writing checks are increasingly the ones buying the products.

CXMT’s IPO subscription opens on July 16. A DRAM chipmaker with ¥33 billion in quarterly profit doesn’t need the fifth standard to list, but its sheer scale validates the STAR Market as the destination board for domestic hard tech. The dozens of pre-revenue quantum, BCI, and robotics companies now stacking their cap tables with the same bank-affiliated investors are betting that the fifth standard will do for them what profitability did for CXMT. The capital flowing in this week already has its exit route mapped.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.