The China Round — July 3, 2026

A $3 billion debut from Kuaishou's video AI, a record coffee-machine round, and new rules for the government money powering Chinese tech

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

Happy Friday everyone. Let’s get straight into it.

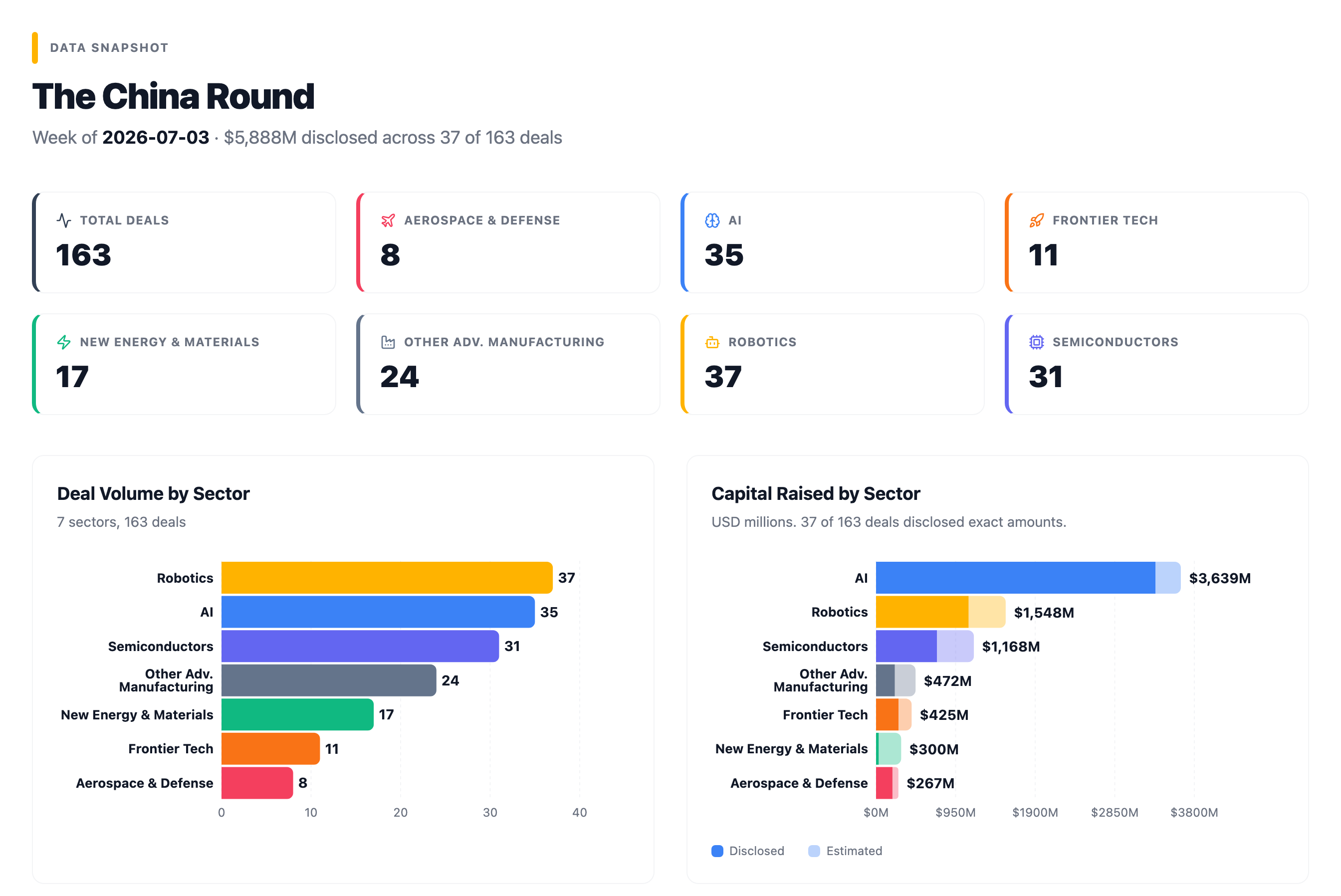

Where the Money Went

163 deals across seven sectors. 37 disclosed exact amounts, totaling $5.9 billion (~¥42.4B). Strip out Kling AI’s $3 billion debut raise and the remaining 36 deals still disclosed $2.9 billion (~¥20.8B). Robotics led on volume (37 deals).

🧠 AI (35 deals)

Kling AI’s $3 billion first external raise dominated the sector and the week (covered below). Several ¥1 billion+ growth rounds closed, including DexForce Technology and Tripo AI (both in Radar below), and Xellar Biosystems (耀速科技), whose organ-on-chip platform screens drug candidates on chip-based organ models (covered below). At the other end, a cluster of seed and angel rounds backed brand-new entrants. Klaren Intelligence (厘清智能), a startup building world models, raised several hundred million RMB with HongShan (红杉), Hillhouse, and Shunwei all on the cap table for a seed round. Founded in April 2026. Eighteen AI companies raised at valuations of ¥100 million (~$14M) or less.

⚡ New Energy & Materials (17 deals)

Mostly sub-¥100 million (~$14M) rounds across battery materials, energy storage, and specialty chemicals. Yingong Technology (隐功科技) raised ¥100 million (~$14M) in a Pre-A for nanocomposite materials, and Anputai (安普态) closed a near-¥100 million A round in advanced insulation, both backed by state-linked funds.

🔬 Semiconductors (31 deals)

31 deals, led by Gowin Semiconductor’s Pre-IPO (covered below). EDA, chiplet packaging, and MEMS sensors each drew 1 to 3 deals, alongside camera sensor chips and power management ICs. Qili Semiconductor (齐力半导体) raised ¥100 million (~$14M) for chiplet packaging at Zhangjiang, and Jiyi Semiconductor (集溢半导体) raised ¥130 million (~$18M) for analog chip design. State capital appeared in investor lists across the sector, with Guangdong, Jiangsu, and Zhejiang government funds all active.

🤖 Robotics (37 deals)

The most active sector by deal count, with three mega-deals (AI2 Robotics, X Square Robot, and Boundless Motion, all covered in Radar below). Below those, the deals split between platform-backed humanoid companies and smaller startups building components, sensors, or manipulation software. Fifteen deals closed at valuations of ¥100 million (~$14M) or less.

💡 Frontier Tech (11 deals)

Eleven deals. SpinQ (量旋科技) raised ¥1 billion (~$139M) in a D-round for quantum computing (more in Radar below). Xinghe Fusion’s (星核聚变) ¥833 million (~$116M) debut was the largest first-round raise in Chinese private fusion, backed by 25 investors including SAIC Motor. Two other fusion companies also raised this week, Andong Jubian (安东聚变) and Chaoci Xinneng (超磁新能), making it a three-fusion-deal week. SynSense (时识科技) closed several hundred million RMB for neuromorphic chips, event-driven processors that react only to changes in a scene rather than analyzing every frame, cutting power consumption for always-on cameras and sensors.

🚀 Aerospace & Defense (8 deals)

Eight deals, dominated by Hongqing Technology’s ¥1.3 billion (~$181M) Pre-B for its satellite constellation (covered below). Puxing Aerospace (谱星航天) raised several hundred million RMB across combined rounds for optical remote-sensing payloads, with plans for a 1,024-satellite constellation.

⚙️ Other Adv. Manufacturing (24 deals)

24 deals spanning optoelectronics, industrial equipment, and consumer hardware. Sinoscience Fullcryo’s ¥1 billion (~$139M) Pre-IPO for cryogenic equipment (covered below) was the sector’s largest. CAYE raised ~¥400 million (~$56M) in a B-round for coffee machines (covered below). At the other end, AIVELA raised several million dollars for its smart ring.

Spotlight

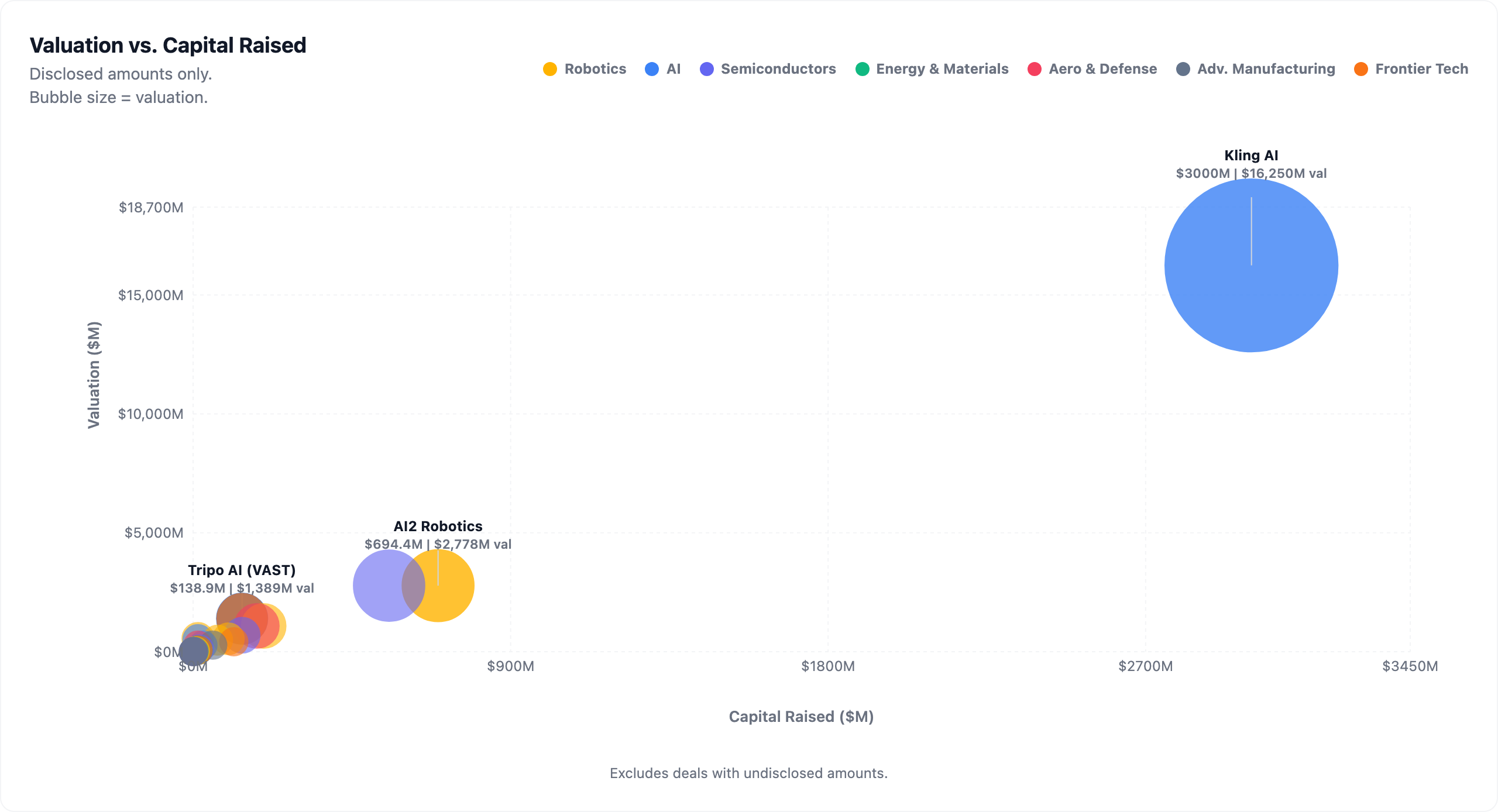

Kling AI (可灵AI)

First External Round, $3B (~¥21.6B), Valued at ~$18B (~¥129.6B)

Kuaishou’s video generation platform raised its first outside capital, with $500M in annualized revenue and a Hong Kong IPO planned within 12 months.

Kling AI is a video and image generation platform spun out of Kuaishou (快手), China’s second-largest short-video app. Users type a text description or upload a photo, and the system generates video clips, still images, or edited versions of existing footage. Kling 3.0, launched globally in February 2026, handles text-to-video, image-to-video, and post-production editing across web, mobile app, mini-programs, and international markets. The platform is known for strong human-motion realism, a persistent weakness in competing systems.

Until this round, Kling was wholly internal to Kuaishou, developed and funded as a product line within the parent company since 2023. Kuaishou registered two wholly-owned subsidiaries in April 2026 to house the spin-off and filed a disclosure with the Hong Kong Stock Exchange in May. Tencent was among the investors. General Atlantic is reportedly in talks, per Bloomberg.

Q1 2026 revenue exceeded ¥650 million (~$90M), up over 300% year-on-year. The company discloses annualized revenue of approximately $500M. The platform reports over 60 million global users, 30,000+ enterprise API clients (businesses that plug Kling’s video generation into their own products), and over 600 million videos generated to date. Approximately 70% of revenue comes from overseas subscriptions and enterprise API services. Goldman Sachs has projected 2026 annual revenue exceeding $1 billion.

Kling competes directly with OpenAI’s Sora, Google’s Veo, Runway, and domestically with ByteDance’s Jimeng (即梦), MiniMax’s Hailuo (海螺), and Alibaba’s Tongyi Wanxiang (通义万相).

This is the second Kuaishou spinout to raise in consecutive weeks. Transtreams, whose SL200 video compression chip placed first in independent benchmarks and has shipped 100,000 units, raised last week. Two separate entities, but together they represent Kuaishou externalizing its video AI stack, from the model that generates the content to the chip that compresses and serves it.

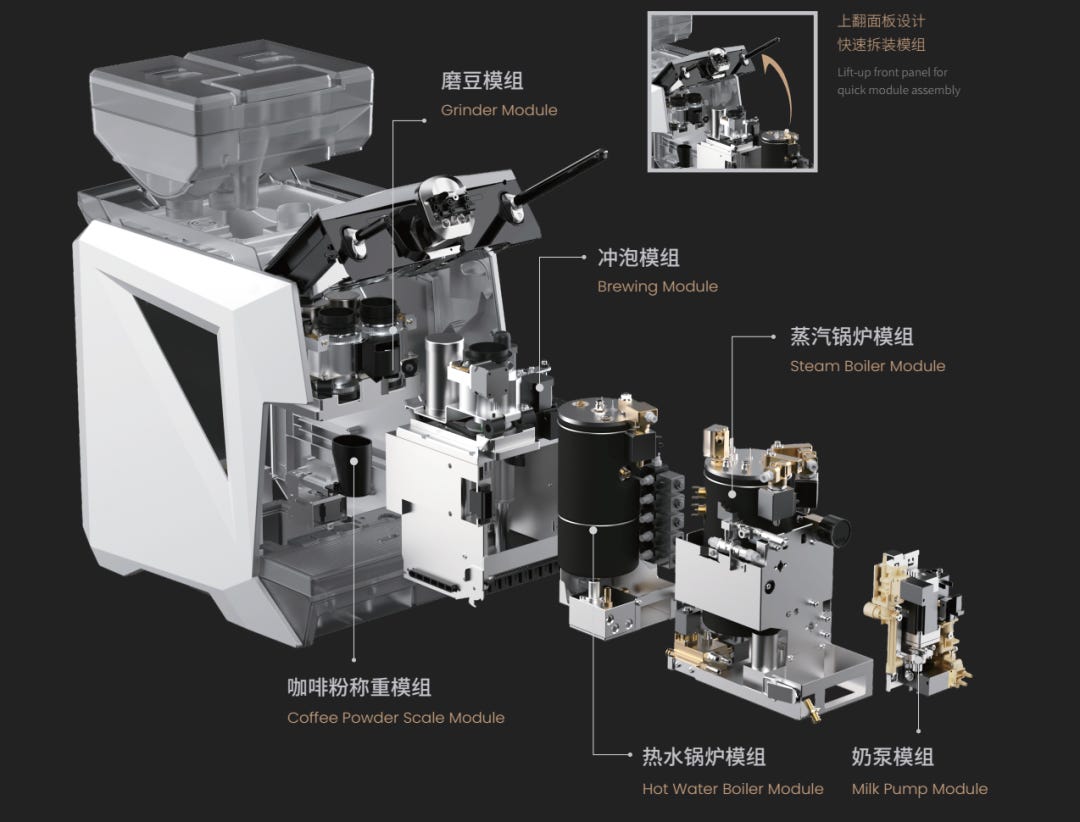

CAYE (咖爷科技)

B Round, ~¥400M (~$56M), Valued at ¥2B (~$278M)

Commercial coffee-machine maker with the sector’s largest-ever single financing round.

CAYE makes fully automatic commercial coffee machines, the kind that produce hundreds of cups an hour in chain cafes, airports, and hotel lobbies. Founded in late 2022 in Suzhou by Wu Peng, a former co-founding team member at Dreame Technology (the robot vacuum company at the center of a government-fund controversy in June), the company has built its own ceramic grinding disc and an automated dosing system that it says improved dosing accuracy by 83%, to within ±0.2 grams per shot. Its top-end Smart X Master model produces up to 429 cups per hour.

This is the largest single financing round in the commercial fully-automatic coffee-machine sector, per both PEdaily and 36Kr. For context, De’Longhi acquired Swiss competitor Eversys in 2021 for approximately $160 million (~¥1.15B), and Eversys was a mature business at the time. CAYE is three years old, claims to operate in 80+ countries and count Peet’s Coffee and Tim Hortons among its clients (though those names come from company press materials, not the chains themselves), and holds over 300 patent applications, competing in a market dominated by European incumbents: WMF, Franke, and Thermoplan.

Meituan Longzhu (美团龙珠, lead), Bairui Capital (柏睿资本), GL Ventures, and others. Meituan Longzhu has now led three consecutive CAYE rounds, a sustained strategic bet from China’s largest food delivery platform.

Gowin Semiconductor (高云半导体)

Pre-IPO, Hundreds of Millions of RMB, Valued at ¥1.5B (~$208M)

China’s first automotive-grade FPGA maker, now on the path to a STAR Market listing.

Gowin Semiconductor designs FPGAs, programmable chips that can be reconfigured after manufacturing to perform different functions. The global market is dominated by three Western firms: AMD/Xilinx (~51%), Intel/Altera (~29%), and Lattice (~7%).

Founded in Guangzhou in 2014, Gowin was the first Chinese company to pass AEC-Q100, the industry test that proves a chip can survive the heat, cold, and vibration of a moving car. At least two domestic competitors (Anlogic and Pango Micro) have since followed, but Gowin’s head start and product breadth (100+ chip models across the Arora, LittleBee, and GoBridge families) give it the deepest lineup. The company has offices in Hong Kong, Taipei, Seoul, Exeter, San Jose, Austin, Tokyo, and Ho Chi Minh City. China’s securities regulator accepted Gowin into the mandatory pre-listing review process for the STAR Market, Shanghai’s stock exchange board built specifically for high-growth tech companies, in May 2026.

13 investors, 7 of them Guangzhou district and city-level state funds. More on what the State Council’s new rules mean for syndicates like this in The Bigger Picture below.

AIVELA

A Round, Several Million Dollars, Valued at ~¥97.5M (~$14M)

A smart ring that proved global demand through crowdfunding before raising from VCs.

AIVELA makes a smart ring with 8 touch sensors and 6 gesture controls. A tiny optical sensor tracks fingertip movement like a mouse’s laser, so a thumb-flick on the ring can scroll a screen. Alongside that, a light-based sensor measures blood flow to calculate heart rate, a motion chip detects tilts and gestures, and a temperature sensor rounds out the package. The product lets users control phone functions, answer calls, navigate presentations, and track health data, all from a ring. The team began work in 2024; the company was formally incorporated in Shenzhen in April 2025 by Li Donghao, a Peking University and Cornell graduate who previously co-founded e-bike company URTOPIA.

Before approaching VCs, AIVELA ran a Kickstarter campaign that raised $865,198 from 5,349 backers (1,730% of its $50,000 goal), then launched on Makuake, Japan’s largest crowdfunding platform, where it pulled in over ¥30 million (~$210,000) within 24 hours. Japan was a deliberate second market. Makuake functions more like a pre-order site than a pitch platform, and Japanese consumers are early adopters of compact wearable hardware. Over 10,000 units were sold through crowdfunding. The company reportedly reached profitability before this round. That sequence, proving consumer demand internationally and reaching profitability before raising institutional capital, inverts the usual sequence of raising VC first, then finding out whether anyone wants the product.

Linear Capital (线性资本, lead), Fengling Capital (锋领资本), URTOPIA (the founder’s prior company), and others.

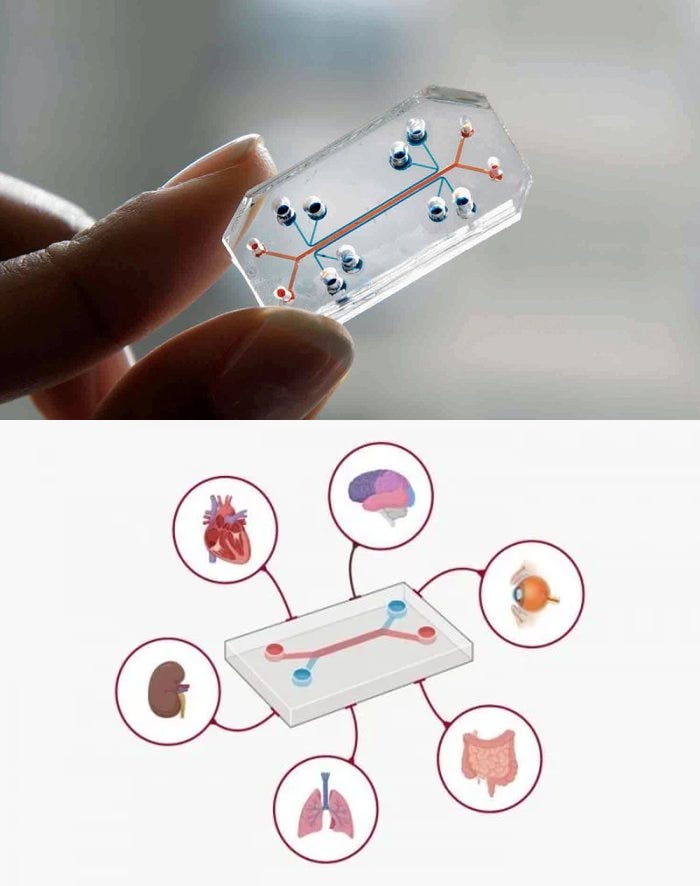

Xellar Biosystems (耀速科技)

A+ Round, ~¥200M (~$28M), Valued at ¥2B (~$278M)

Organ-on-chip platform with FDA participation and pharma clients on 3 continents.

Xellar Biosystems builds organ-on-chip systems, small devices that simulate human organs on microchips using living cells. Instead of testing a new drug on an animal or waiting for human clinical trials, pharmaceutical companies can run early tests on these chip-based models of hearts, livers, lungs, or tumors. The technology does not replace clinical trials, but it can filter out failing drug candidates earlier, potentially saving years and hundreds of millions of dollars per program.

Founded in late 2021 in Boston by Xin Xie (PhD Northeastern University, research fellowship at Harvard/Brigham and Women’s Hospital), Xellar operates from dual headquarters in Boston and Beijing with additional offices in Shenzhen. The company is the sole Chinese participant in a nine-platform study run by a consortium focused on replacing animal testing with lab-grown alternatives, accepted into the FDA’s ISTAND program (Innovative Science and Technology Approaches for New Drugs) in January 2026, a regulatory pathway that could help organ-on-chip data gain broader acceptance in drug applications. Xellar lists Sanofi, Pfizer, and L’Oréal among its clients, though these names come from company materials, not the pharma companies themselves. Cumulative A-series financing has reached approximately ¥400 million (~$56M).

Oriental Fortune Capital (东方富海), GF Xinde (广发信德), Yunbai Capital (沄柏资本), Guofang Ventures (国方创投), Qingsong Capital (清松), and others.

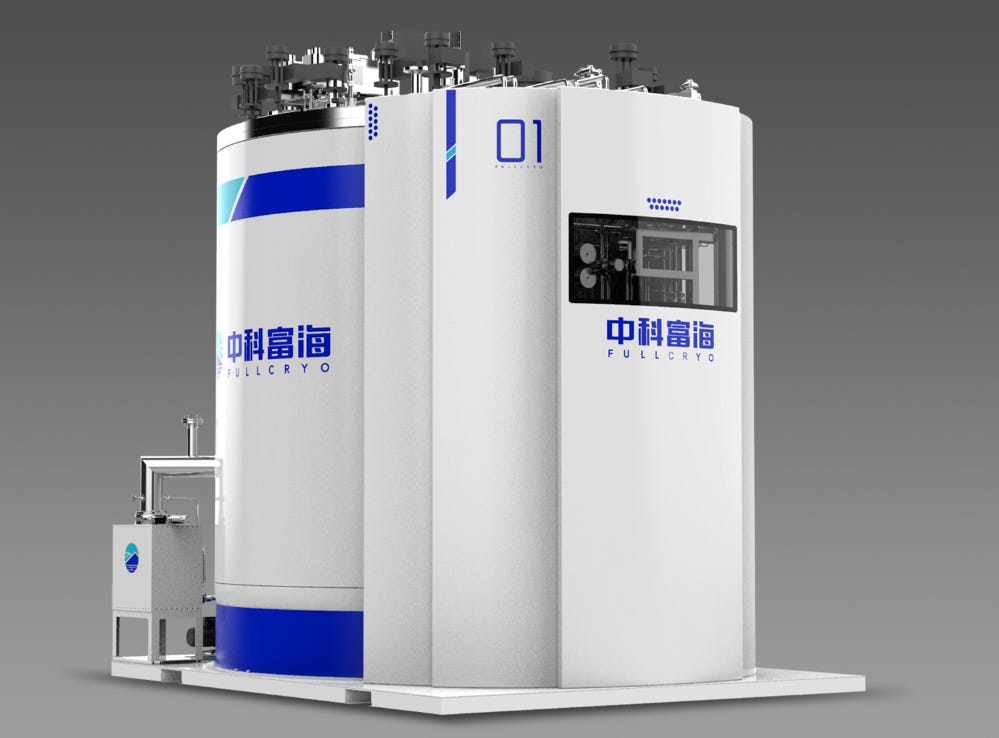

Sinoscience Fullcryo (中科富海)

Pre-IPO, ¥1B (~$139M), Valued at ~¥10B (~$1.39B) per ITJuzi

The only Chinese company with full independent IP in large-scale cryogenic refrigeration, now IPO-bound.

Sinoscience Fullcryo builds large-scale cryogenic refrigeration systems, equipment that cools gases to temperatures between 2 and 20 kelvin (roughly -271°C to -253°C). At those temperatures, hydrogen liquefies for storage and transport, helium becomes a superfluid, and superconducting magnets function for fusion reactors and quantum computers. The company is described by state media as the third entity globally, and the only Chinese one, with full independent intellectual property across the cryogenic chain, after Linde and Air Liquide.

Founded in August 2016 as a spinout from the Chinese Academy of Sciences (CAS) Institute of Physics and Chemistry. Revenue reached ¥740 million (~$103M) in 2024. The company exported China’s first large-scale hydrogen-liquefaction unit (1.5 tons per day) to Canada in January 2022. STAR Market (科创板) IPO coaching began in October 2025 with Zhongtai Securities as underwriter, after the company abandoned an earlier plan to list in Hong Kong.

CAS Capital (国科资本), the investment arm of CAS Holdings, led the round. The academy’s own investment vehicle backing its own spinout at the pre-IPO stage. Prior rounds include a ¥300 million (~$42M) B-round from Sinopec Capital (2022) and an ¥800 million (~$111M) C-round at a post-money valuation of ¥7.8 billion (~$1.08B) in 2023.

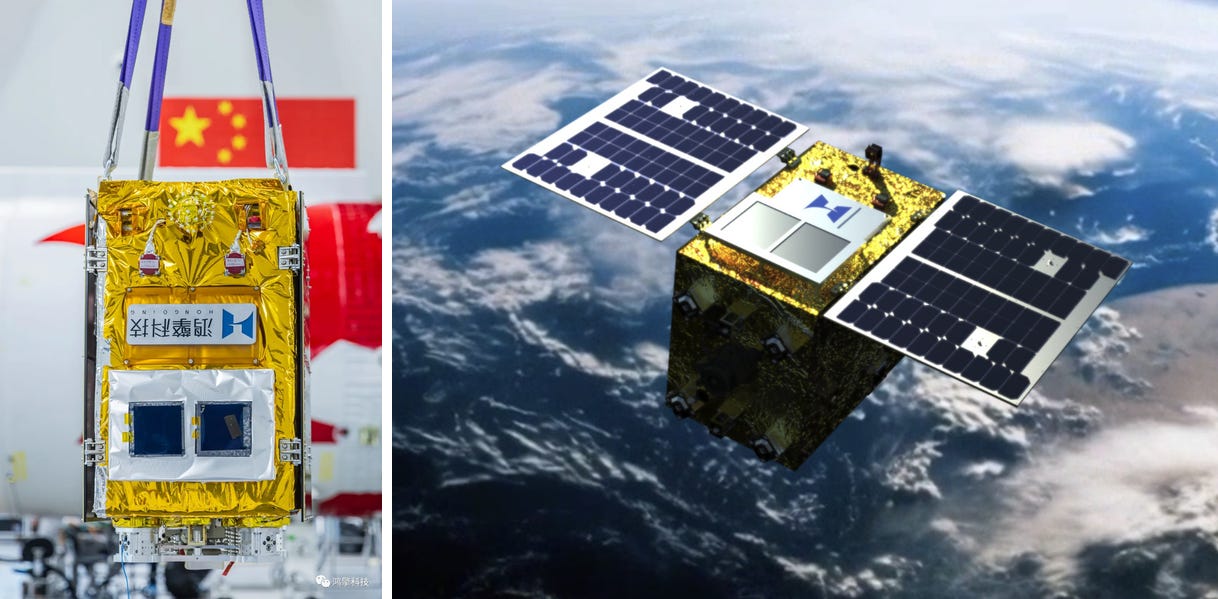

Hongqing Technology (鸿擎科技)

Pre-B, >¥1.3B (~$181M), Cumulative >¥2.5B (~$347M), Valued at ¥7.8B (~$1.08B)

Backed by a rocket company, this satellite subsidiary builds its own propulsion, power systems, and electronics, filing for a 10,000-satellite constellation.

Hongqing Technology is building a satellite constellation of 10,000 satellites spread across 160 separate orbital paths around Earth (so the constellation can deliver continuous coverage instead of clustering all satellites along a single track), filed in May 2024 with the International Telecommunication Union, the UN body that allocates orbital slots and radio frequencies, a mandatory step before any company can legally operate a satellite network at that scale.

Hongqing is a subsidiary of LandSpace (蓝箭航天), the Chinese private rocket company that operates the Zhuque-2, the world’s first methane-fueled rocket to reach orbit. LandSpace holds a majority stake (reported combined holdings above 50%), with CEO Zhang Changwu serving as Hongqing’s chairman. The company was founded in November 2017, longer ago than most satellite startups, and manufactures its own propulsion (Jinwu, with 4,089 ignitions at 100% success rate per company site), power systems (Chiyu solar arrays), and satellite electronics (Baize). A Xiong’an manufacturing base can produce over 100 flat-panel satellites per year. A test satellite launched from Xichang on May 31, 2026 via a Long March 2D.

One entity builds the rockets, a subsidiary builds and operates the satellite network. The filing makes Hongqing China’s third megaconstellation after the state-backed Guowang (国网) and Shanghai’s Qianfan/G60 (千帆). The difference is that Hongqing can price its own launches through its parent company, a cost advantage that state-operated constellations using commercial launch providers do not have.

CCB Investment (lead), ICBC Capital, Jinpu Capital (金浦资本), and others. 18 investors in total.

Also on the Radar

AI2 Robotics (智平方). C round, ~¥5B (~$694M), valued at >¥20B (~$2.78B). The Greater Bay Area’s highest-valued privately-held embodied-AI company raised from 26 institutional investors. Its AlphaBot humanoid robots are in early mass production at over 100 units per month, with a verified ¥500 million three-year order from HKC (惠科) for semiconductor display production lines.

X Square Robot (自变量机器人). C round, valued at >¥20B (~$2.78B). The only Chinese embodied-AI company to have received investment from all 4 major platforms across successive rounds: Meituan, Alibaba, ByteDance, and Xiaomi (corroborated by 每经网, 新华网, 财联社). China Mobile joined in the C round. The company has deployed robotic arms on a German auto-parts production line and in a domestic home-services pilot with 58.com.

Tripo AI (生数科技/VAST). A3 round (per PEdaily; ITJuzi categorizes as A+), >¥1B (~$139M), valued at ¥10B (~$1.39B). A platform that generates 3D digital models from text or photos, used by game studios, e-commerce sellers, and product designers, with over 2 million creators and 700+ enterprise customers, per company materials. Founder Song Yachen previously co-founded MiniMax. This was VAST’s second round in 30 days.

SpinQ (量旋科技). D round, ¥1B (~$139M), valued at ¥10B (~$1.39B). Builds superconducting quantum computers and has shipped systems to over 200 customers in 40+ countries. Third round in 2026, bringing total funding raised this year to approximately ¥2 billion (~$278M).

Boundless Motion (无界动力). Angel (cumulative), >$200M (~¥1.44B). Mass-producing the K15 dual-arm wheeled robot. Verified global orders include ZF LIFETEC (Germany) and Ormowell Group. Founded by Zhang Yufeng, former VP of Horizon Robotics. JD, C Capital, and Hony Capital among the investors in this latest tranche.

DexForce Technology (跨维智能). B round, ¥1B (~$139M), valued at >¥10B (~$1.39B). Over 1,500 robotic units deployed on factory floors and H1 2026 revenue of ¥100 million (~$14M). Confirmed clients include Midea, GAC Aion, Zoomlion, and Lens Technology.

Lexiang Technology (乐享科技). Pre-A, ~¥500M (~$69M), valued at ¥3.5B (~$486M). Home robotics brand (元点 Zeroth) with a 30,000+ unit backlog and H1 2026 revenue up 600% year-on-year, per PEdaily. Ant Group (lead) and Geely Capital among the investors.

Xinghe Fusion (星核聚变). First round, ¥833M (~$116M), valued at ¥3B (~$417M). The largest debut raise in Chinese private fusion. Most fusion companies use a tokamak; Xinghe is building a quasi-isodynamic stellarator instead, a more geometrically complex magnetic design that trades harder engineering for potentially steadier plasma control. Founded November 2025 in Hefei. 25 institutional investors including SAIC Motor and Shenzhen Capital Group.

Discover Robotics (求之科技). Angel, >$100M (~¥720M), valued at ¥3.9B (~$542M). A Tsinghua spinout building the AIRBOT series, wheeled robots with two arms that can grasp and move objects. Founded by Zhou Guyue, who led the DJI Mavic drone product line before joining Tsinghua as a professor. PEdaily called this the record angel round in the consumer embodied-robot sector.

SynSense (时识科技). B+ round, several hundred million RMB, valued at ¥5B (~$694M). Neuromorphic chip maker with dual headquarters in Shanghai and Zurich. Its Speck chip is in mass production for edge sensing. Acquired Swiss sensor company iniVation in 2024 and counts Samsung as a strategic investor.

Primelife Science (璞睿生命科技). A round, ~¥100M (~$14M), valued at ¥500M (~$69M). AI-powered clinical trial platform that counts 7 of the global top 10 pharmaceutical companies as clients, per company materials. Co-founded with IQVIA. CICC Capital (中金资本) and Sumitomo Corporation Asia Capital (住友商事亚洲资本) participated.

The Bigger Picture

The State Capital Squeeze

In early June, the State Council issued Document No. 54 (reposted by the securities regulator), a set of rules that for the first time explicitly bars counties and districts from establishing new government investment funds without approval from higher levels of government. Government investment funds are public money that local governments invest into private startups, often requiring the startup to build a factory or office locally in return, to seed the tech industries they want in their region. The operative text: “严控新设政府投资基金,县区原则上不得新设” (strictly control the establishment of new government investment funds; counties and districts shall in principle not establish new ones).

By 2025, China had set up over 2,100 government guidance funds with target capital of approximately ¥11 trillion (~$1.53 trillion). In one central province, for example, over 60% of counties had established their own funds competing for the same deals.

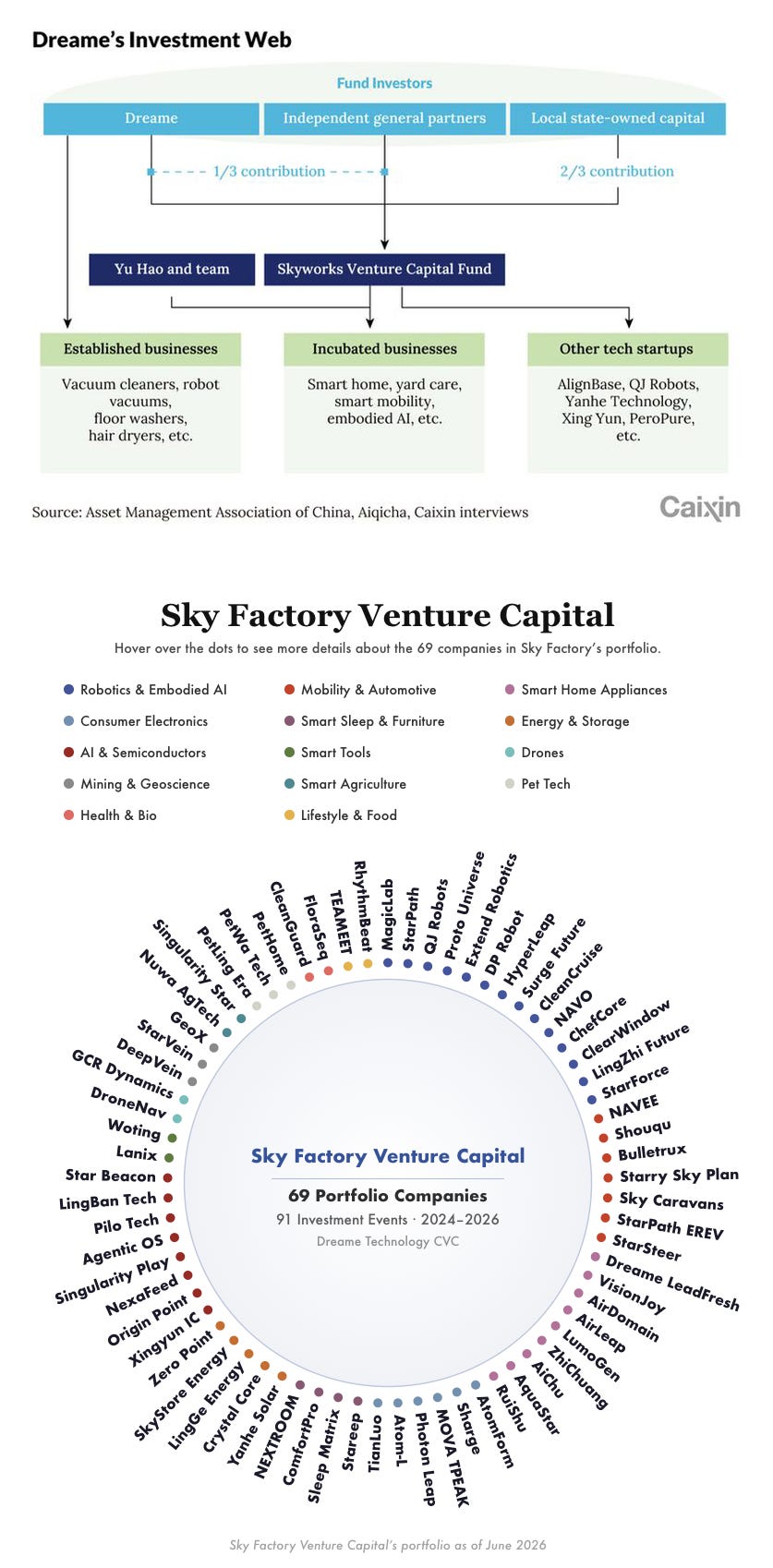

The most visible case was Dreame Technology (追觅科技), the robot vacuum maker whose ambitions outran its core business.

Dreame’s Sky Factory Venture Capital Fund manages ¥41.6 billion (~$5.8B), with approximately 80% drawn from local government industry funds across cities including Suzhou, Xiamen, Shaoxing, Hangzhou, and Chengdu. Through a four-layer corporate structure, the company has spawned 955 affiliated entities. Of the 101 entities Dreame directly controls, roughly 72% were registered in the past two and a half years. Founder Yu Hao’s Weibo account was suspended in early June. The pattern echoes the over ¥15 billion (~$2.1B) Wuhan Hongxin semiconductor failure from 2020, where local government capital funded an ambitious chip project that collapsed.

Gowin Semiconductor’s Pre-IPO syndicate included 7 Guangzhou district and city-level state funds, local government vehicles backing a company in their jurisdiction, often competing with neighboring cities for the same technologies. Compare that to Sinoscience Fullcryo’s Pre-IPO, led by CAS Capital, the investment arm of the Chinese Academy of Sciences, a national institution with deep technical expertise in the exact cryogenics technology it is backing. The State Council’s rules do not retroactively block existing investments, and they do not ban government capital from startups. They pull oversight upward, from counties to provinces, from local officials to central institutions. For founders, the money is still there, but the path to it now runs through fewer, larger, more selective gatekeepers.

Spinning Out the Stack

This week’s largest deal was a spinout. Kling AI raised $3 billion after Kuaishou separated it into two wholly-owned subsidiaries in April. A week earlier, Transtreams, another Kuaishou spinout, raised for its video compression chip. Two separate entities capitalizing different layers of the same video AI stack.

Sinoscience Fullcryo is a 2016 spinout from the Chinese Academy of Sciences, now at Pre-IPO with CAS’s own investment arm leading the round. Hongqing Technology is a LandSpace subsidiary that builds the satellites its parent’s rockets carry, raising separately with state-bank affiliates leading. Because LandSpace built the launch vehicle, Hongqing can price its own launches at cost rather than buying rides. Discover Robotics, a Tsinghua spinout, raised a $100 million angel round.

Four established organizations this week, a tech platform, a national research institute, a rocket company, and a university, each externalized internal capabilities and raised capital for them separately.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.