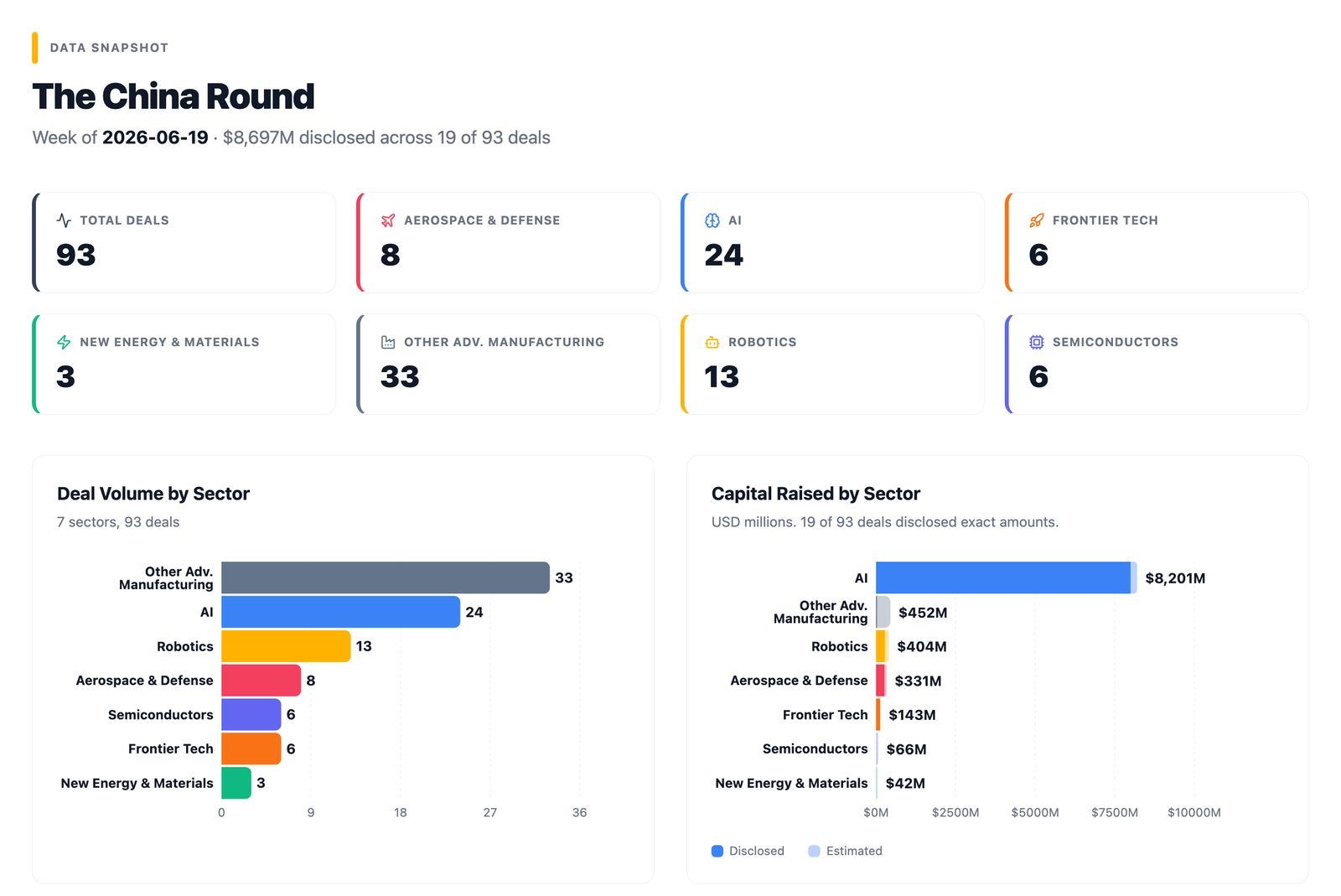

The China Round — June 19, 2026

DeepSeek's first outside money, a $2 billion company with no product, and six companies chasing the world model layer

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows is where talent concentrates, where production capacity gets built, and where the next commercial technologies will come from.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

This past week, DeepSeek raised over $7 billion (~¥51B) in its first-ever external funding round, the largest single financing event in Chinese AI history. The rest of the data is just as revealing: 93 deals in total, a wave of new company formations in physical AI, and at least six companies raising in the same week to build “world models,” AI systems that predict physical cause and effect so robots can plan actions before executing them.

Where the Money Went

Ninety-three deals landed between June 12 and 18. Nineteen disclosed amounts, combining for $8.7 billion (~¥62.6B) in total disclosed capital. DeepSeek alone accounts for 82% of that figure. Strip it out and 18 deals still disclosed a combined $1.6 billion (~¥11.5B), a strong week by any measure.

Roughly 43% of deals were angel or seed rounds, well above the typical weekly mix. This skew reflects a physical AI company-formation wave, with new teams spinning out of established labs and raising within weeks of incorporation.

🧠 AI (24 deals)

AI dominated both deal count and capital. DeepSeek’s ¥51 billion (~$7B+) A round accounted for the vast majority of that capital, but the sector had depth beyond it: LiblibAI raised $300 million (~¥2.2B) for its AI creative platform, SiliconFlow closed a ¥2 billion (~$278M) B round for inference infrastructure, and 卜拉格科技 raised ~$220 million (~¥1.6B) in its first institutional round with no shipped product. A cluster of companies raised to build “world models” for robotics. Physis, Manifold AI, and Synapx all closed world model rounds in the same window. More on this pattern in The Bigger Picture.

🤖 Robotics (13 deals)

Thirteen robotics deals disclosed $278 million (~¥2B). SEAHI Robotics pulled in ¥1 billion (~$139M) for its marine robots, while GigaAI closed a ¥1 billion (~$139M) B2 round for its humanoid platform. ACE Robotics, which builds AI software brains for robots, raised nearly $100 million (~¥720M) at angel stage with a ¥2.6 billion (~$361M) valuation. NOITOM Robotics, a leading player in the global professional motion capture market, raised several hundred million RMB (~$30-130M) for its pivot into robot training data. At the smaller end, a half-dozen angel-stage robotics companies each raised single-digit millions.

🚀 Aerospace & Defense (8 deals)

Eight deals, $264 million (~¥1.9B) disclosed. Emposat (航天驭星) led with a ¥1.4 billion (~$195M) D+ round for satellite ground operations ahead of an IPO filing. ZEROG (零重力飞机工业), which makes both conventional electric fixed-wing aircraft (already shipping, over 1,000 letters of intent) and electric aircraft designed for vertical takeoff and landing (in development), closed a ¥500 million (~$70M) B round led by three Hefei government funds. Juneng Tianqing (聚能天擎) raised several hundred million RMB (~$30-130M) for methane rocket engines at angel stage.

💡 Frontier Tech (6 deals)

Six deals, $125 million (~¥900M) disclosed. Taiyi Quantum (太一量生) raised ¥300 million (~$42M) at Pre-A for its neutral-atom quantum computer, which uses ytterbium atoms suspended in a laser trap rather than the superconducting qubits favored by IBM and Google. The approach runs at room temperature and makes fewer calculation errors, the main bottleneck in current quantum systems. Xeonova (星能玄光) closed a ¥500 million (~$70M) A round for commercial nuclear fusion. Nuclear fusion, the reaction that powers stars, would produce nearly unlimited clean energy if it can be sustained cheaply. Most approaches require enormous reactor chambers costing billions; Xeonova uses a compact alternative reactor design that reaches initial plasma ignition at far lower cost.

🔬 Semiconductors (6 deals)

Six semiconductor deals, mostly with undisclosed amounts. The most notable chip deal of the week was NanoCore Chip (微纳核芯), which raised ¥1 billion (~$139M) in a B+ round for its RISC-V processor platform. RISC-V is an open-source chip architecture, the open alternative to ARM’s proprietary designs, important because it avoids licensing dependencies on Western IP and gives Chinese manufacturers a path around US export controls on chip technology. The sector was quieter than in recent weeks.

⚡ New Energy & Materials (3 deals)

Three deals, all with undisclosed amounts. TCL’s venture arm backed an early-stage new materials company, and two strategic rounds landed in specialty chemicals and clean energy.

⚙️ Other Adv. Manufacturing (33 deals)

Thirty-three deals across optoelectronics, industrial equipment, quantum instruments, display materials, and precision manufacturing. Most were early stage with undisclosed amounts. The Hefei government continued its aggressive cluster-building, leading or co-leading rounds in advanced materials and quantum instrument companies alongside its aerospace investments.

Spotlight

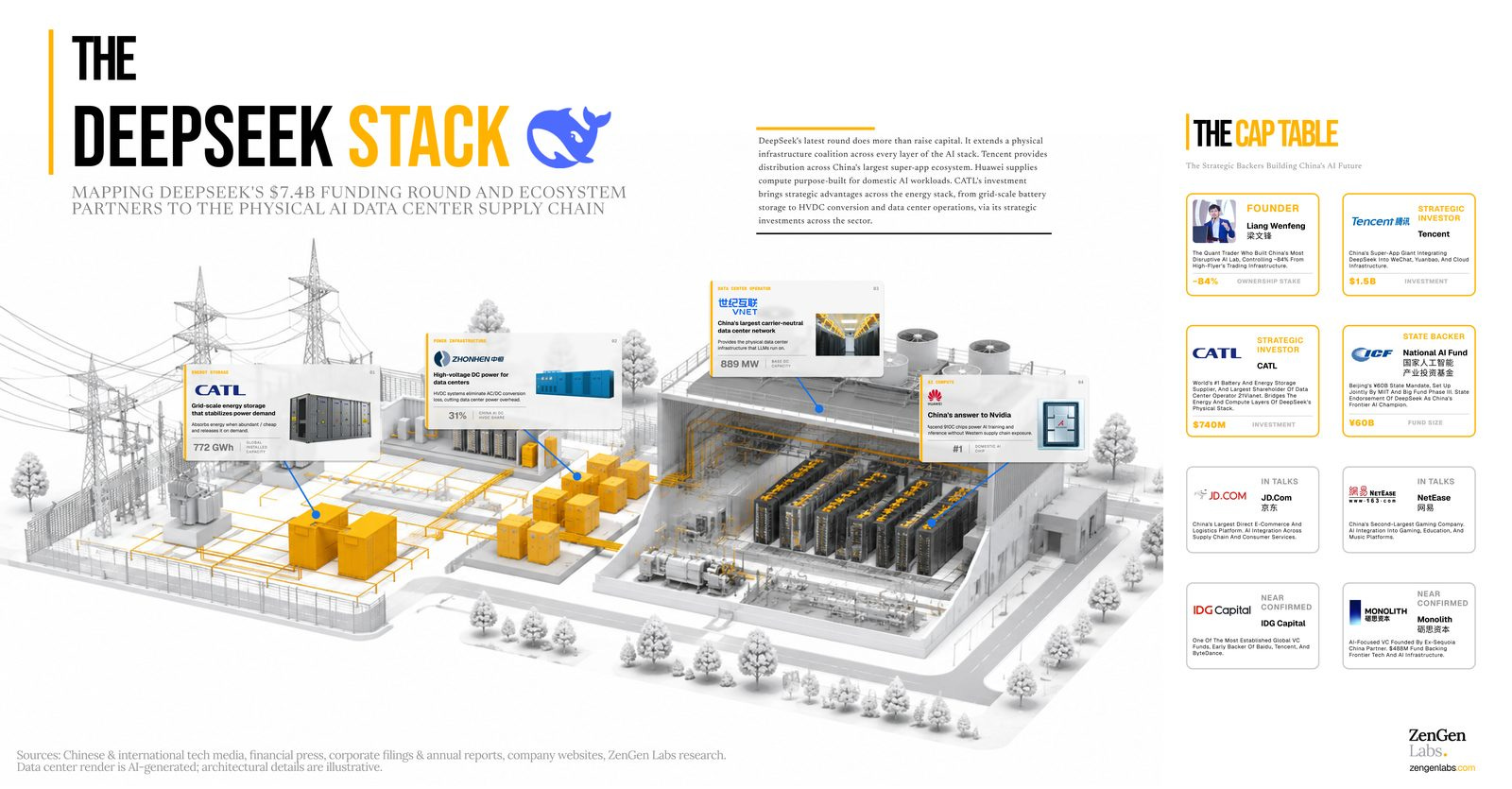

DeepSeek (深度求索)

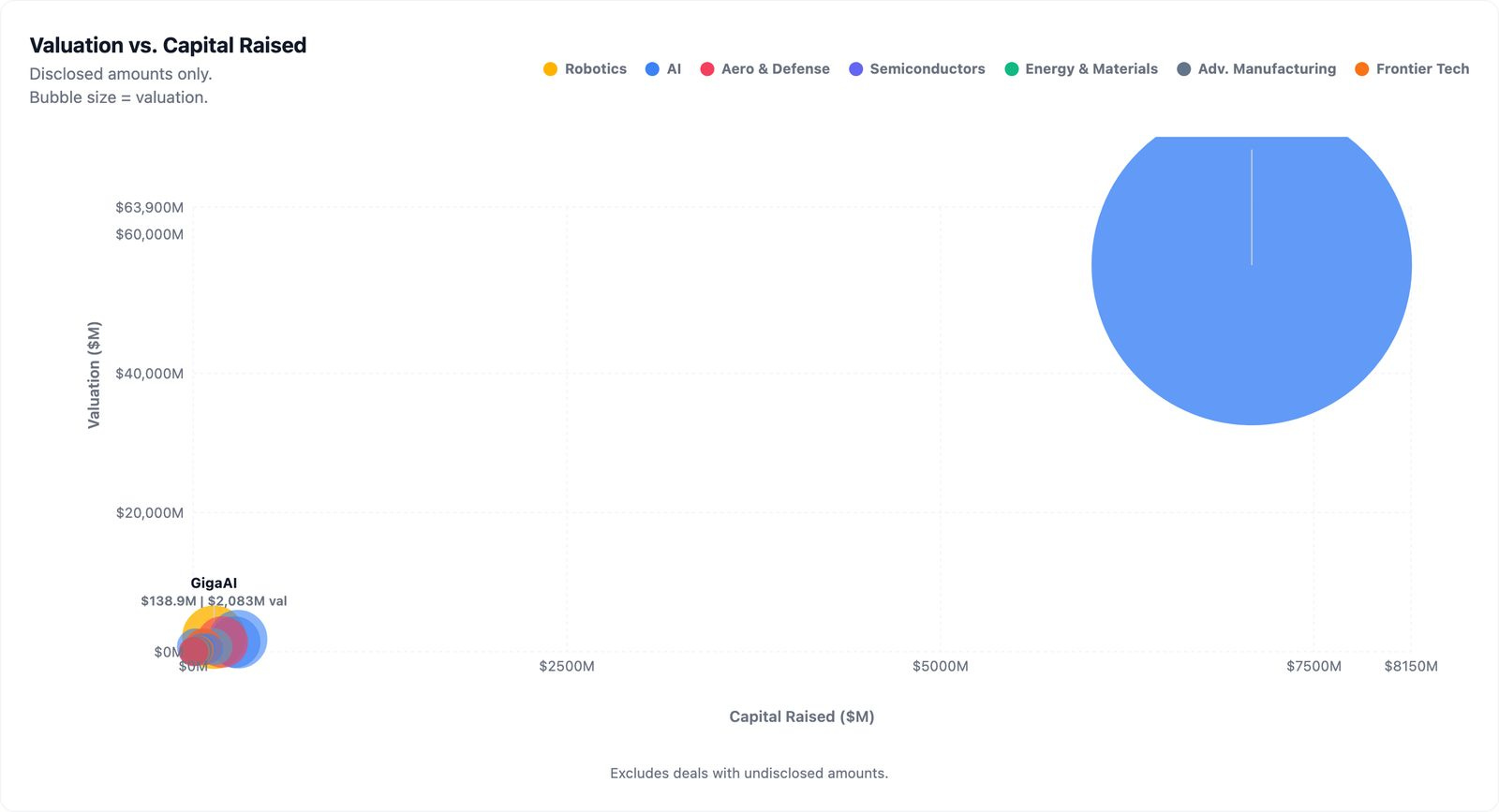

A round, ¥51B (~$7B+), valuation ~¥400B (~$55.6B)

China’s top AI lab takes its first outside money, on its own terms.

DeepSeek is the Hangzhou-based AI research lab behind the open-source models that have reshaped global AI competition. Its R1 reasoning model hit #1 on the US App Store in January 2025, and its latest V4 model is one of the most capable AI systems publicly available: it can process roughly a million words of text in a single session, handle text, images, and audio together, and it does this at a scale (1.6 trillion parameters) that matches or exceeds the largest Western frontier models. For three years since its founding in 2023, DeepSeek was entirely self-funded by its parent High-Flyer Capital Management, a quantitative hedge fund. This A round is its first external capital.

The structure is as notable as the size. Founder Liang Wenfeng holds roughly 84% equity through a limited partnership vehicle that strips commercial investors of voting rights and board seats, with a five-year lockup preventing share sales. In most venture deals, large investors receive some governance rights in exchange for their capital; here they receive none. CATL, the world’s largest battery maker, invested approximately ¥5 billion (~$696M), pursuing a vertical integration thesis where its energy storage systems power AI data centers. The deal effectively prices DeepSeek as China’s most valuable private AI company while keeping founder control absolute. The only exception is the National AI Fund, which received direct equity with voting rights rather than the governance-free structure given to commercial investors. That distinction suggests the Chinese government negotiated for actual influence over the company’s direction, not just financial exposure, signaling that DeepSeek is now explicitly part of national AI strategy.

Investors include Liang Wenfeng, Tencent, CATL, and others.

卜拉格科技 (Bulage, Shanghai)

First institutional round, ~$220M (~¥1.6B), valuation ~$2B (~¥13.5B)

The Qwen team leader leaves Alibaba and raises ~$220 million before building anything.

卜拉格科技 was incorporated in Shanghai in May 2026. The name sounds like a transliteration of “pragmatics” (语用学), a branch of linguistics that studies how context shapes meaning, how the same words mean different things depending on who says them, where, and why. The parent entity is registered as 语用科技 (”pragmatics technology”), a nod to the founder’s roots in language models. It was founded by Lin Junyang (林俊旸), born 1993, who at the time was Alibaba’s youngest engineer to reach its highest internal technical grade (P10, a tier typically held by only a handful of people across a 200,000-person organization) and headed the Qwen large language model team. He left Alibaba in March 2026 and announced his departure on X. Within weeks of incorporation, he raised approximately $220 million from Banyan Capital (高榕创投, $100M, co-lead), HongShan (红杉中国, $100M, co-lead), and Tencent ($20M), at a valuation of roughly $2 billion.

The company has no product, no website, and no employees beyond the founding team. The entire round was priced on founder pedigree. Lin’s focus is on what the field calls “world models”: AI systems that give robots the ability to predict what will happen before they act. Today’s robots largely respond to instructions step by step; a robot with a genuine world model can simulate a sequence of actions in its head and choose the one most likely to work, the way a chess player thinks several moves ahead. The team he built at Alibaba subsequently released Qwen-RobotWorld, a model trained on 8.6 million video-text pairs that ranked first on EWMBench, an independent benchmark measuring how well AI systems understand and predict physical environments, and Qwen-VLA (Vision-Language-Action), a model that takes what a robot sees and what a human tells it to do, and converts both into physical movements. Lin didn’t build those products (they shipped after his departure), but he assembled the team and set the research direction. When three investors commit $220 million to a company that exists only on paper, they’re betting the person who built the team can do it again.

Investors: Banyan Capital (高榕创投, co-lead), HongShan (红杉中国, co-lead), Tencent ($20M).

LiblibAI (哩布哩布AI)

B+, $300M (~¥2.2B), valuation >$2B (~¥14.4B+)

One of China’s highest-revenue AI application companies keeps compounding.

LiblibAI is a Beijing-based AI creative content platform with three products: LiblibAI for image generation, LibTV for AI video (launched March 2026), and 星流 (”Star Flow”) for AI-powered design workflows. The company reports annual recurring revenue exceeding $300 million as of May 2026, with a projection of $600 million by year-end. LibTV generated over $1 million per day in its first month. The platform has over 30 million cumulative users.

Founder Chen Mian (陈冕), born 1992, previously led global commercialization for CapCut/Jianying at ByteDance, reaching management level 4-1 (the youngest to do so at ByteDance at the time). He left to build LiblibAI, and the revenue trajectory since has been the company’s primary pitch. The parent entity is Evoken (演语科技). This B+ round values the company at over $2 billion, making it one of China’s most valuable AI application companies. The valuation is grounded in real revenue rather than research potential, which makes it an outlier among this week’s mega-deals. For context, most of the other $1B+ raises this week are for pre-revenue companies. LiblibAI is not.

Investors: Granite Asia (lead), Tencent (lead), Shunwei Capital (顺为资本, lead), and others including HT Investment, Era Capital, Banyan Capital, Ant Group, Greenpan Capital, Mingjing Ventures, Sourceware Capital, and HongShan (follow-on).

GigaAI (极佳视界)

B2, ~¥1B (~$139M), valuation >¥10B (~$1.39B+)

Rare among Chinese companies in that it has both shipping humanoid robots and a top-ranked world model.

GigaAI builds what it calls “Physical AGI” from its Beijing headquarters: a full stack spanning world models (GigaWorld), which handle physical prediction; perception-and-action models (GigaBrain), which translate visual input and verbal instructions into physical movements; and two hardware products (Maker H01, a wheeled humanoid robot for industrial use, and SeeLight S1, a household humanoid). Maker H01 began its first batch deliveries on January 31, 2026, and the company has partnerships with over 30 automakers and autonomous driving companies. A planned deployment of 1,000 robots with Longsheng Technology in Wuxi is underway over the next three years.

GigaAI raised ¥3.5 billion (~$487M) across three rounds (Pre-B, B1, B2) in just three months. GigaAI was founded by Huang Guan, a Tsinghua PhD in automation who previously worked at Horizon Robotics and Microsoft. Its GigaWorld-1 topped the WorldArena benchmark in April 2026. WorldArena is an independent evaluation framework run by Tsinghua’s FIB Lab that measures how well AI systems predict physical world changes, the closest the field has to an independent performance test rather than a company’s own promotional benchmark. GigaAI is rare in that it has both benchmark performance and shipping hardware, a combination that most competitors lack. The B2 investor base includes a Singapore-based fund (Lion City Capital, 狮城资本, a multi-round follow-on investor) and the China-Belgium Direct Equity Investment Fund (中比基金), a bilateral fund established by the Chinese and Belgian governments in 2004.

Investors: Lion City Capital (狮城资本), China-Belgium Fund (中比基金), China Construction Investment (建投投资), Wanxiang Qianchao (万向钱潮), Fosun Ruizheng (复星锐正), Huagai Chuangying (华盖创赢), Deyi Capital (德屹资本), Huacang Capital (华仓资本), Yuanshi Fund (元石基金), and others. Returning shareholders: Guozhong Capital (国中资本), Dachen Caizhi (达晨财智), Turing Asset Management (图灵资管). FA: Gengxin Capital (庚辛资本).

SiliconFlow (硅基流动)

B round, ¥2B+ (~$278M+), valuation ~¥10B (~$1.39B)

The neutral inference rail where every investor is also a customer.

SiliconFlow is a Beijing-based AI inference infrastructure platform that serves as a neutral middleman between AI models and enterprise users. It hosts over 160 models from providers including DeepSeek, Qwen, OpenAI, and Google, without favoring any single model family. The platform has over 10 million users and 10,000 enterprise clients. Its daily usage, measured in tokens (the units of text that AI models process), ranked first among more than 70 providers on OpenRouter, an internationally-run marketplace that aggregates AI models from dozens of providers and tracks real usage volume. First place on a neutral leaderboard is a stronger signal of scale than a company-reported traffic claim, because the aggregator has no stake in inflating the numbers. Monthly overseas revenue has reached several million dollars.

CEO Yuan Jinhui holds a PhD from Tsinghua and was a researcher at Microsoft Research Asia, where he later created the OneFlow deep learning framework, an open-source tool for training large AI models, before founding SiliconFlow in August 2023. The B round’s investor composition is the most interesting structural signal of the week: several of the investors, including Ctrip (the travel platform), JinkoSolar (solar panel manufacturer), Kingdee (enterprise software), NIO Capital (electric vehicles), Biren (GPU maker), and SenseTime (AI), are simultaneously enterprise customers of SiliconFlow’s inference services. When your investors are also your customers, the capital comes with built-in demand. It also means the investors have direct visibility into the company’s product performance, which makes the pricing more informed than a typical venture round.

Investors: Huakong Fund (华控基金), GGV Capital (纪源资本), Ctrip Strategic Investment, JinkoSolar, Kingdee, China Unicom Xinwo, Shengyi Capital (盛奕资本), Biren Strategic Investment, NIO Capital, SenseTime Strategic Investment, Giant Interactive, Guotai Junan Innovation, WaldenVentures, China Development Finance, Zhongguancun Science City, and others. FA: China Renaissance (华兴资本).

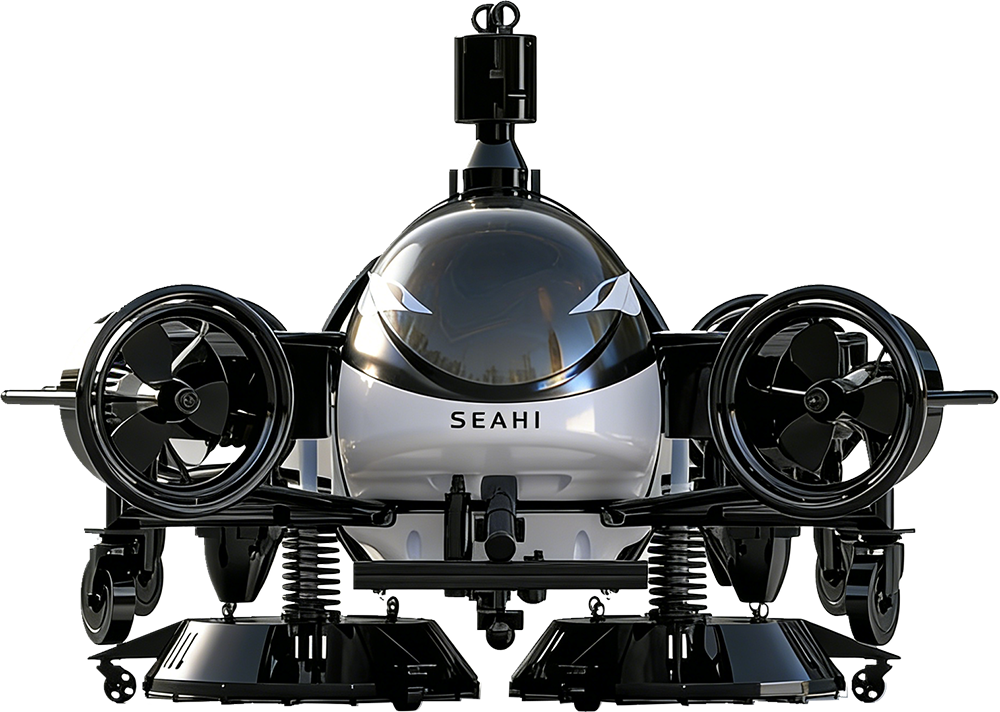

SEAHI Robotics (世航智能)

A round, ¥1B+ (~$139M+), valuation ~¥5B (~$696M)

Marine robots for hull cleaning and underwater inspection, with orders exceeding ¥1 billion in six months.

SEAHI Robotics builds autonomous underwater and surface robots for ship hull cleaning, underwater security, and offshore wind farm inspection from its base in Suzhou. The company’s flagship product is the Orca (虎鲸) marine robot. Its AI system for marine operations, trained on data gathered from millions of hours of real commercial deployments (not simulations), handles the decision-making for the robots: identifying hull fouling, navigating around obstacles, and determining when a section is clean enough to stop scrubbing. In the first half of 2026 alone, SEAHI’s order backlog exceeded ¥1 billion (~$139M).

CEO Chen Xiaobo, born 1989, won China’s top national award for defense science and technology at 28, a credential that matters in a sector where contracts often require security clearances and government trust. SEAHI was selected by Singapore’s Maritime and Port Authority (MPA) as one of six partners for its In-Water Hull Inspection and Cleaning Innovation program, with trials beginning in H2 2026. Saudi Arabia’s HAKA Group has also visited the company to explore cooperation. Moore Threads (摩尔线程) and Kunlun Chip (昆仑芯), both domestic GPU makers, co-invested alongside Vertex Growth (a Temasek subsidiary). The companies building China’s AI compute chips are now investing in the robots that will run on them.

Investors: Moore Threads (摩尔线程), Kunlun Chip (昆仑芯), Shanghe Momentum Fund (上河动量), Vertex Growth (Temasek), CITIC Agriculture Fund (中信农业基金), Yuzun Capital (裕尊资本), Dayang Electric (大洋电机), and others. Returning shareholders: GSR Ventures (金沙江创投, 5th round), Vertex Ventures China (祥峰中国), Meridian Capital (华映资本), Changshi Capital (长石资本).

Physis (逆矩阵科技)

Seed++, >$100M (~¥720M+), valuation ~¥3.25B (~$452M)

Two founders, ages 27 and 21, raise over $100 million in four months to build a universal model of the physical world.

Physis was founded on February 14, 2026, in Beijing by Ji Jiaming (纪嘉铭), 27, a PhD student at Peking University’s AI Research Institute who was selected as an Apple Scholar in AI/ML, an annual award Apple gives to roughly 20 PhD students globally whose research it considers among the most promising in machine learning. His co-founder is Chen Boyuan (陈博远), 21, an undergraduate at Peking University’s Yuanpei College who had already published a Spotlight paper at NeurIPS 2025, the field’s most competitive academic conference, where roughly 3% of submitted papers receive that recognition. In four months, they raised over $100 million across an angel round (from Hillhouse Capital and PKU-affiliated Yanyu Ventures/燕缘创投) and this seed++ round.

Their thesis: the “window for winning the world model race is compressing from three years to 18 months,” a quote from a 36kr profile. Physis debuted its first model, Physis-v0.1, at the Zhiyuan AI Conference on June 12, 2026, organized by the Beijing Academy of Artificial Intelligence (BAAI). The company has no commercial product and no revenue. The investors are betting on the founders and the timing: if the world model layer proves to be the critical missing piece for making robots useful, being early matters more than being profitable.

Investors: Matrix Partners China (经纬创投), 5Y Capital (五源资本), Guanghe Capital (光合创投), Ant Group (strategic), BAI Capital, Zhongding Capital (钟鼎资本). Returning from angel: Hillhouse Capital, Yanyu Ventures (燕缘创投). FA (angel round): Gaohu Capital (高鹄资本).

Also on the Radar

Taiyi Quantum (太一量生). Pre-A, ¥300M (~$42M), valuation ¥1.8B (~$250M). Neutral-atom quantum computing (see Frontier Tech above). Team includes members from Microsoft, MIT, JILA, and NIST. Led by IDG Capital and Banyan Capital (高榕创投).

Xeonova (星能玄光). A round, ¥500M (~$70M), valuation ¥5B (~$696M). Compact nuclear fusion (see Frontier Tech above). Two working devices built in 26 months. Founded by Prof. Sun Xuan, a USTC professor with experience at Princeton Plasma Physics Lab. Led by Jinpu Investment (金浦投资), Dachen Caizhi (达晨财智), and Cornerstone Capital (基石资本).

Emposat (航天驭星). D+, ¥1.4B (~$195M), valuation ¥10B (~$1.39B). Emposat runs the ground infrastructure that keeps satellites functional: the network of antenna stations that communicate with satellites, confirm their position, and send operational commands. Without this layer, a satellite launched into orbit cannot be steered, monitored, or tasked. Emposat operates over 60 such stations, serving more than 500 satellites. IPO guidance filed in June 2026. Investors include SAIC Group (上汽集团) and China Insurance Investment (中保投资).

ACE Robotics (大晓机器人). Angel, ~$100M (~¥720M), valuation ¥2.6B (~$362M). ACE builds the AI software layer that gives robots physical understanding, the ability to interpret their surroundings and plan movements without step-by-step human instruction. Rather than selling robots directly, ACE sells the “brain” that other hardware companies can integrate into their products. Co-founded by Wang Xiaogang, a SenseTime co-founder, and Tao Dacheng, an AI academician. Investors include Geely Capital (吉利资本) and Dachen Caizhi (达晨财智).

Manifold AI (流形空间). Pre-A extension, several hundred million RMB (~$30-130M). Builds interactive world models for physical AI, the same prediction-and-planning layer that the Bigger Picture section below explores. WorldScape-0.2 leads the WorldScore benchmark. Six rounds totaling close to ¥1 billion (~$139M) raised since the company was founded in May 2025. Backed by Temasek, China Guoxin (中国国新), and BAIC Industry Investment (北汽产投).

Synapx (章鱼动力). Pre-A, $50M (~¥360M), valuation ¥3.25B (~$452M). Synapx builds the data infrastructure and decision-making software that robot companies use to train and improve their machines, collecting movement data, labeling it, and turning it into training sets that make robots more capable over time. Founder Du Dalong was the sixth employee at Horizon Robotics, one of China’s leading autonomous driving chip companies. Three rounds totaling roughly $140 million in four months. Led by Jinqiu Fund (锦秋基金), Xinlian Capital (芯联资本), and HPR Capital (黄浦江资本).

MoleculeMind (分子之心). A round extension, past $100M cumulative, valuation ¥3.6B (~$501M). MoleculeMind uses AI to design proteins, the molecular structures that most drugs target. For decades, figuring out how a protein folds into its three-dimensional shape (which determines what it does and how drugs bind to it) required years of lab work. Deep learning cracked this problem, and Prof. Xu Jinbo, MoleculeMind’s founder, built one of the early methods for doing so in 2016. The company is a resident at Eli Lilly’s Lilly Gateway Labs Shanghai innovation hub. Per company materials, it claims over 90% target hit rate on protein design tasks. Investors include Lanqiao Capital (蓝桥资本), Pudong Venture Capital (浦东创投), and Fosun Chuangfu (复星创富).

Noematrix (穹彻智能). A+, several hundred million RMB (~$30-130M), valuation ¥4B (~$557M). Most robots today navigate visually, using cameras to see where things are, but they have no sense of how hard they are pressing or whether they are about to break something. Noematrix teaches robots to feel force and resistance during physical contact, the way a human hand knows the difference between picking up a glass and crushing it. Without this, robots cannot safely handle fragile objects or work alongside people. Co-founded by Prof. Lu Cewu, who conducted postdoctoral research in Fei-Fei Li’s group at Stanford, and Wang Shiquan, founder of Flexiv (a robotics company). Investors include Wuxi Data Group (无锡数据集团, lead), Yicun Capital (一村资本), and Shanghai Jiao Tong University AI Future Fund.

Simple AI (深朴智能). Pre-A, several hundred million RMB (~$30-130M), valuation ¥3B (~$417M). General-purpose service robots initially targeting hotel housekeeping, powered by a lightweight world model (Simple-World) that lets the robot predict what will happen when it interacts with objects in a room. CEO Li Xiaofei holds a Tsinghua PhD and co-founded autonomous driving company Idriverplus (智行者). Led by Didi (滴滴出行), the ride-hailing platform, which sees hotel robots as a step toward future autonomous fleet management. Investors: Didi (lead) and CCV (创世伙伴创投).

NOITOM Robotics (诺亦腾机器人). Pre-A++, several hundred million RMB (~$30-130M), valuation ¥3B (~$417M). NOITOM’s parent company supplies motion capture systems, the technology used to record human movement for film and video games, to a significant share of the professional market. That library of human movement data, accumulated over 13 years, is now being converted into robot training sets: teaching robots how humans walk, reach, grasp, and manipulate objects by showing them recordings of people doing the same things. Chief Scientist Han Lei, per company materials, previously led Tencent’s Robotics X Lab. The robotics division is now selling motion data and training pipelines to 30+ robot companies.

NanoCore Chip (微纳核芯). B+, ¥1B (~$139M), valuation ¥5B (~$696M). RISC-V AI chips for on-device processing in robots, vehicles, and factory machines (see Semiconductors above). Led by BlueRun Ventures (蓝驰创投), SMIC Juyuan (中芯聚源), and Cybernaut (赛伯乐投资).

ZEROG (零重力飞机工业). B round, ¥500M (~$70M), valuation ¥5B (~$696M). One of the few Chinese companies that makes both conventional electric fixed-wing aircraft, planes that take off from a runway using electric motors instead of jet fuel, with one model (RX1E-A) already shipping and over 1,000 letters of intent, and electric aircraft that take off and land vertically like a helicopter (eVTOL), aimed at urban air taxi markets and currently in development. Revenue from the conventional electric aircraft business funds eVTOL R&D, a self-financing model that most eVTOL competitors lack. Led by three Hefei government funds: Hefei Industry Investment (合肥产投), Hefei Innovation Investment (合肥创新投资), and Hefei High-Tech Investment (合肥高投).

The Bigger Picture

Angel Rounds at Unicorn Valuations

In 2023, Chinese embodied AI startups at the angel and seed stage typically carried valuations of ¥100 to 200 million (~$14-28M), and even at those levels many struggled to attract capital. By 2026, equivalent early-stage companies are commanding valuations of ¥1.5 billion to ¥13 billion (~$208M-$1.8B). This week’s data puts the shift into relief.

ACE Robotics raised nearly $100 million at angel stage with a ¥2.6 billion (~$362M) valuation. Maniformer, an embodied AI startup incorporated on February 3, raised hundreds of millions within 11 days of founding at a ¥2 billion (~$278M) valuation. Juneng Tianqing raised several hundred million RMB at angel stage with a ¥1.5 billion (~$208M) valuation. Physis raised over $100 million at seed++ with a ¥3.25 billion (~$452M) valuation. And 卜拉格科技 raised $220 million at roughly $2 billion (~¥13.5B) with zero product.

What’s driving it? China’s official financial press uses the phrase “关键窗口期” (critical window period) to describe 2026 for physical AI: the year when mass production verification and real-world deployment will sort winners from the field. The framing functions like a fire alarm for capital: it signals that the companies forming now will be the ones that survive consolidation, and that investors who wait for proof of concept will find the winners already locked up. Private investment rounds typically predict where public stock prices will move 6 to 18 months later. Investors who get into a company before it goes public, or before it becomes too expensive in private markets, capture the largest gains. That lag creates urgency: if you believe the public market will price robotics companies much higher in 18 months, the time to invest is now, not then. One VC told 36kr: “Maybe we are in a relatively crazy stage now.” TMT Post reported that investors now ask about valuation and previous backers before asking about the technology: companies outside the ¥10 billion (~$1.4B) valuation club reportedly “lack even the ticket to sit at the table.”

The first half of 2026 has already seen ¥46 billion (~$6.4B) across 288 financing events in embodied AI, with the top 20 companies capturing 70% of that capital. In 2025, CloudMinds (达闼机器人), which had accumulated over ¥5.4 billion (~$750M) in lifetime funding at a ¥20 billion+ (~$2.8B) valuation, ran out of capital, proving that massive funding at the pre-revenue stage does not guarantee survival. The pricing is not irrational on its own terms: investors are paying growth-stage valuations at the angel stage, betting these companies will be Series B businesses within 18 months. Whether those expectations survive contact with the market is the open question.

The World Model Gold Rush

The valuation surge above and the pattern below are the same bet: that the companies forming now will own the layer that makes robots useful.

This week, at least six Chinese companies raised specifically to build “world models” for physical AI: GigaAI (B2, ~¥1B), Manifold AI (Pre-A extension, several hundred million RMB), Physis (seed++, >$100M), 卜拉格科技 (first round, ~$220M), Synapx (Pre-A, $50M), and Aether AI (angel, $20M). Combined capital: roughly $500 million in a single week for the same narrow niche.

A world model is an AI system that predicts physical states rather than text or images. A video generator like Sora produces visually plausible content but cannot respond to an action in real time. A world model takes an input (a robot arm moves left) and predicts the resulting physical state (the cup slides off the table). The practical goal is to give a robot a mental model of what will happen before it acts, enabling planning and simulation without real-world trial and error.

Q1 2026 physical AI funding alone exceeded $6.4 billion, with China accounting for 43% of global robotics venture investment. WorldArena, run by Tsinghua University’s FIB Lab and hosted as a CVPR 2026 challenge (CVPR is the flagship computer vision research conference), evaluates how well world models predict physical changes. But WorldArena’s own research found that visual quality and functional utility have a correlation of only 0.36, meaning a model can generate realistic-looking physical simulations while being poor at actually guiding a robot.

In 2023, China’s “百模大战” (Hundred Model War) saw hundreds of large language models, the AI systems that power ChatGPT and DeepSeek, announced by Chinese companies, with six major startups each raising hundreds of millions. By 2025, the field had consolidated to a handful of survivors. World models may be entering the same phase: concentrated bets on a narrow layer, with the question of whether six companies (or sixteen) can maintain genuinely differentiated approaches, or whether open-source releases will collapse the field as DeepSeek did to LLMs.

Ninety-three deals, $8.7 billion in disclosed capital, and a generation of companies that didn’t exist six months ago now valued like mid-stage enterprises. The capital has picked its thesis: physical AI is the next platform, and the window to own it is closing. What remains to be seen is whether 2026’s bets age like DeepSeek’s early believers or like CloudMinds’ last backers.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.