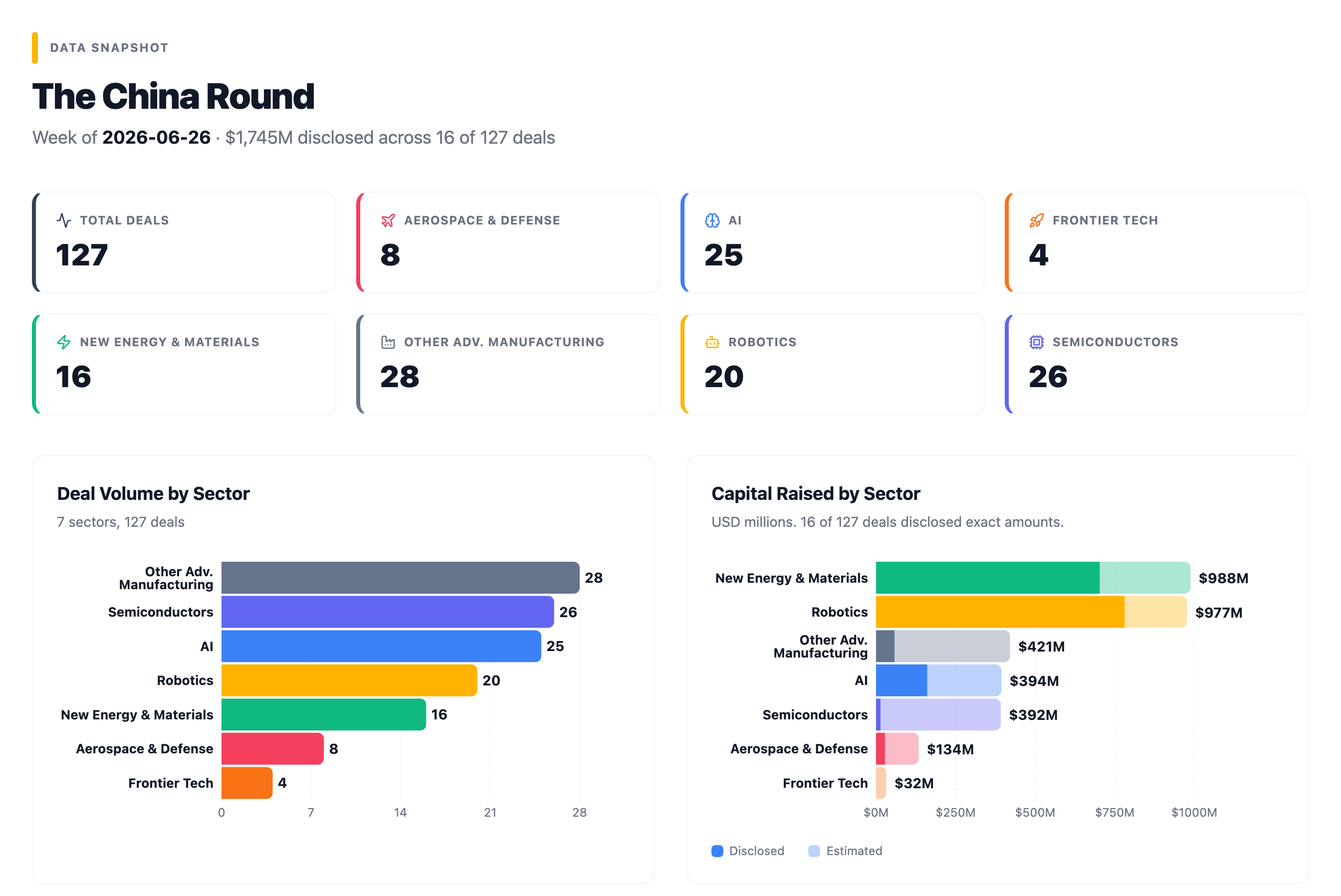

The China Round — June 26, 2026

A chip from a Kuaishou spinout beats NVIDIA at video compression, gaming companies fund robot simulation, and Saudi oil money backs Chinese green hydrogen

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows is where talent concentrates, where production capacity gets built, and where the next commercial technologies will come from.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

This week, a robotics company founded in 2015 with over ¥1 billion (~$139M) in annual revenue filed for its Hong Kong IPO at a ¥19.5 billion (~$2.7B) valuation. The same week, a robotics company founded 90 days ago with zero product raised at a ¥9 billion (~$1.25B) valuation. Both are rational bets. 127 deals spanned every sector, early-stage rounds continued to swell to growth-stage sizes, and the most interesting capital flows crossed sector boundaries.

Where the Money Went

127 deals this week, 49 of which disclosed amounts totaling approximately $1.75 billion (~¥12.6B). Strip out COOWA’s $600 million (~¥4.3B) IPO round and Tongwei Solar’s ¥5.06 billion (~$703M) restructuring, and 47 deals disclosed a combined ~$442 million. Most Chinese deals don’t disclose amounts, so the actual total is higher.

Stage distribution: 42 angel, seed, and pre-A rounds, 49 at Series A/A+, 15 at Series B or later, and 21 strategic investments. The early-stage dominance reflects a market where the embodied AI and physical AI boom is still generating new companies faster than it is graduating existing ones.

🧠 AI (25 deals)

The largest AI cluster spans physical AI infrastructure, video generation, and 3D content. Lightwheel AI (光轮智能) raised ¥1 billion (~$139M) for robot simulation data from a syndicate that includes three listed gaming companies. Sand AI raised over $100 million for video generation that competes with OpenAI’s Sora. Deemos (影眸科技) raised hundreds of millions of RMB for 3D generative AI with clients including Unity, Figma, and Canva. Jiangxing AI (江行智能) closed its third fundraise of 2026, backed by CATL-affiliated capital, Jinkosolar, and Yanzhou Energy as customer-investors.

⚡ New Energy & Materials (16 deals)

The headline is Tongwei Solar’s ¥5.06 billion (~$703M) restructuring, which dwarfs everything else. Beyond that, the energy transition stories are more interesting than the numbers suggest. HYDOtech (海德氢能) attracted a repeat investment from Saudi Aramco’s venture arm alongside Conch Group’s private equity arm, one of China’s largest cement producers. HYLICreate (合源锂创) landed a Xiaomi fund-led round for solid-state batteries with a live factory. Solide (索理德) raised for silicon-carbon anode materials at volume production scale.

🔬 Semiconductors (26 deals)

The second-largest sector by deal count spans optical interconnect chips, AI inference silicon, and specialized sensors. Aluksen Technology (傲科光电子) closed a B++ for high-speed optical chips that connect GPUs inside AI data centers. AIPhotonix (慧芯激光) raised to build its own manufacturing line for gallium arsenide and indium phosphide optical chips, targeting the same AI data center interconnect market. Transtreams (凌川科技) closed an A+ for a video compression chip that outperforms NVIDIA on compression efficiency benchmarks. Juxin Semiconductor (聚芯半导体) filed for a Hong Kong IPO as the world’s fourth-largest optical sensor company by revenue.

🤖 Robotics (20 deals)

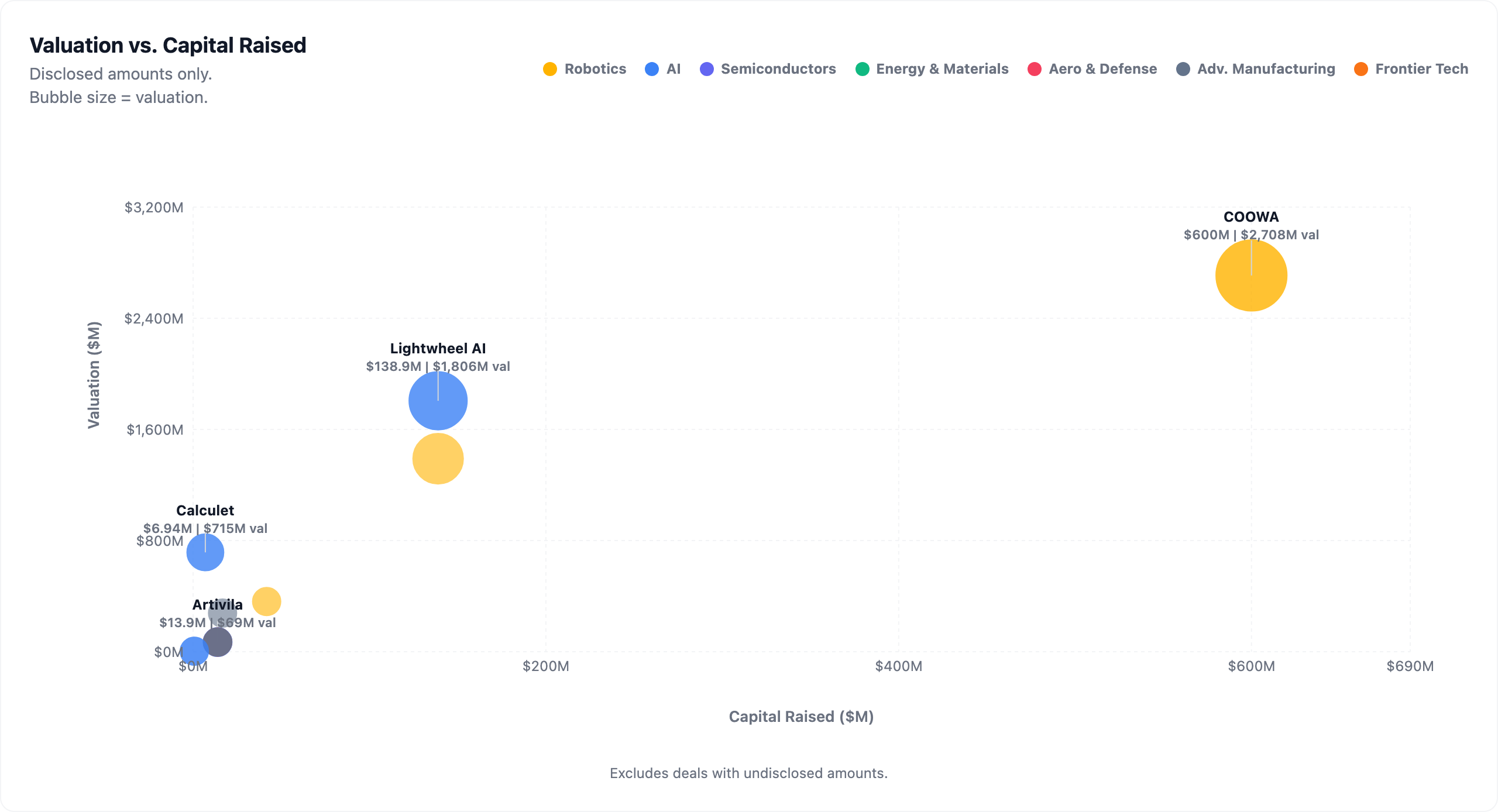

COOWA (酷哇科技) is raising $600 million (~¥4.3B) ahead of a Hong Kong IPO at a ¥19.5 billion (~$2.7B) valuation, with SoftBank China Venture Capital backing. At the other extreme, Kunlun Xing (昆仑行机器人) raised an undisclosed amount at a ¥9 billion (~$1.25B) valuation 90 days after founding, with zero product. AGILINK (临界点) hit unicorn status at ¥10 billion in its B round, five months after founding, though unlike most instant unicorns it actually has revenue and 8,000+ dexterous robot hands shipped.

💡 Frontier Tech (4 deals)

The smallest sector by count but one deal carries outsized signal: Juhe Jubian (聚合聚变), a fusion energy startup in Hefei, raised an angel round co-led by Hillhouse Ventures and Sequoia China, the third fusion deal in three consecutive weeks across three distinct fusion approaches.

🚀 Aerospace & Defense (8 deals)

Argo Space Technology (吉天星舟) raised a B round as a profitable space-tech component supplier with 55 payloads delivered and 30 in orbit at a 100% success rate. Jitai Aviation (吉太航空) raised for a modular electric vertical takeoff and landing aircraft, an air taxi that takes off like a helicopter but runs on electric motors, targeting China’s government-designated “low-altitude economy” covering commercial airspace below 1,000 meters.

⚙️ Other Advanced Manufacturing (28 deals)

The largest sector by deal count spans industrial automation, optoelectronics, and specialized manufacturing. Highlights include Fubusi (辅布司), an AI textile cutting company, and Botler Robotics (博特勒), building high-temperature superconducting magnets for fusion reactors.

Spotlight

COOWA (酷哇科技)

Latest round, $600M (~¥4.3B), ¥19.5B (~$2.7B) valuation

Autonomous urban robots that actually make money.

COOWA builds autonomous robots for urban sanitation, delivery, and patrol, deployed across more than 50 cities. Founded in 2015 by He Tao, who taught at Shanghai Jiao Tong University from 2012 to 2014, the company has spent 11 years building what might be the most unglamorous corner of robotics: street-sweeping machines, garbage-collecting vehicles, and delivery bots that navigate sidewalks and roads without human operators. The result is annual revenue exceeding ¥1 billion (~$139M) and the company’s first year of positive EBITDA, meaning the core operations generate more cash than they consume before financing costs and accounting write-downs. For a hardware robotics company, where depreciation on factories and fleets can mask operating health, that number is the one that shows whether the actual business works.

COOWA’s autonomous sanitation robots navigating a residential complex and public roads. Source: COOWA

The company plans to file for a Hong Kong IPO within the next two to three months, with Deutsche Bank as co-sponsor and Huatai Securities as lead. The listing would make COOWA one of the first Chinese robotics companies to go public on operational profit rather than a growth story.

Investors: SoftBank China Venture Capital (软银中国资本), Asia Investment Capital (亚投资本).

Lightwheel AI (光轮智能)

Strategic round, ¥1B (~$139M), valuation exceeding ¥15B (~$2.1B)

The data factory underneath every robot company.

Lightwheel AI doesn’t build robots. It builds the synthetic environments where robots learn to move, grasp, and navigate before they encounter the real world. Think of it as the training gym for physical AI: companies like NVIDIA, Google DeepMind, Figure AI, and 1X Technologies use Lightwheel’s simulation data and physics-accurate virtual worlds to train their machines. The company claims that over 80% of the simulation assets used by the world’s leading embodied AI teams come from its platform.

Three listed Chinese gaming companies, Giant Network (巨人网络), BOTON Technology (宝通科技), and 37 Interactive Entertainment (三七互娱), all ended up on the same cap table. The connection is infrastructure: the physics engines that power video games, the same technology that simulates gravity, collisions, and fluid dynamics in realistic game worlds, are the exact tools needed to create synthetic training data for robots. NVIDIA’s PhysX engine, originally built for gaming, now powers Isaac Sim, the company’s robotics simulation platform. Lightwheel sits downstream of that same stack with a proprietary physics solver. BOTON Technology is perhaps the most interesting investor of the three: it’s both a mobile game publisher and a manufacturer of industrial conveyor belts for mines and ports, and its stated investment rationale is that its mine shafts and factory floors provide real-world training environments that complement Lightwheel’s simulations.

The global benchmark is Applied Intuition, the US simulation company valued at $15 billion after a $600 million Series F in June 2025. Lightwheel’s ¥15 billion+ (~$2.1B+) valuation puts it at roughly one-seventh of that, despite operating in an adjacent market. Founded in Beijing in January 2023 by Xie Chen, a former simulation lead at NVIDIA, Cruise, and NIO, the company has raised approximately ¥2 billion (~$278M) across two rounds in the space of about a month.

Investors: Zhongguancun Science City Fund, Sichuan Development S&T Fund, Shandong Development S&T Fund, Giant Network (巨人网络), BOTON Technology (宝通科技), 37 Interactive Entertainment (三七互娱, follow-on), and others.

HYDOtech (海德氢能)

B+, hundreds of millions of RMB, valuation undisclosed

Saudi Aramco invests twice in the same Chinese green hydrogen startup.

HYDOtech manufactures alkaline pressurized electrolyzers, the machines that split water into hydrogen and oxygen using renewable electricity. Founded in Nanjing in late 2021 by a team from Academician Ouyang Mingao’s group at Tsinghua University, the company has delivered over 700 megawatts of electrolyzer capacity and operates projects across China, Europe, the Middle East, and Saudi Arabia. Aramco Ventures, the venture capital arm of the world’s largest oil company, first invested in HYDOtech in December 2024, marking its first hydrogen investment anywhere in the Asia-Pacific region. It came back for a second investment in this B+ round.

Conch Group, one of China’s largest cement producers and one of the country’s biggest industrial carbon emitters, also invested in this round through its private equity arm. Shell and TotalEnergies are project partners collaborating on green hydrogen production. The broader pattern — why oil companies, cement producers, and European energy majors are all converging on Chinese electrolyzer technology — is explored in The Bigger Picture below.

Investors: Aramco Ventures (repeat), Conch Private Equity (海螺私募, strategic), Dongfang Jiafu (东方嘉富, follow-on). Prior investors include Sinopec Capital (中国石化资本), NIO Capital (蔚来资本), Sequoia China, Xianghe Capital (襄禾资本).

Sand AI

Two rounds totaling over $100M, valuation undisclosed

China’s bet against OpenAI’s Sora, with the Kuaishou founder investing in his own competitor.

Sand AI builds video generation models. Where OpenAI’s Sora and Kuaishou’s Kling (Kuaishou is China’s second-largest short-video platform) generate entire videos as a single computation, Sand AI’s approach generates video in 24-frame chunks, processing each chunk as a self-contained scene before threading them together in sequence, the way a filmmaker shoots scenes in order rather than computing the entire film at once. The company argues this produces more physically consistent motion, better cause-and-effect logic, and longer coherent video.

Sand AI’s MAGI-1 model demonstrating autoregressive video extension, generating physically consistent motion beyond the original clip. Source: Sand AI

The product, called VidMuse, launched in early 2026 and hit $10 million in annual recurring revenue within two months, an unusually fast commercial ramp for a Chinese AI company. The interface is English-first, the product competes globally, and the company has released its core model (MAGI-1) as open source on GitHub, where it has accumulated over 3,700 stars. A next-generation model is planned for July 2026, using an architecture that routes different types of content (human motion, lighting, backgrounds) to specialized sub-networks trained for each task rather than running everything through one neural network. The approach costs less to run at scale and tends to produce sharper results.

Su Hua (宿华), the founder of Kuaishou, invested personally alongside Wang Huiwen’s family office. Kuaishou operates Kling, one of Sand AI’s direct competitors. A platform founder investing in a company that competes with his own product suggests he sees a future where the market is large enough for multiple approaches, or that Sand AI’s architecture might eventually complement rather than cannibalize Kuaishou’s own tools.

Investors: Su Hua (宿华, personal), Lollapalooza Capital (王慧文家族办公室), Jiukun Ventures (九坤创投), Matrix Partners China (经纬创投), IDG Capital, Baidu Ventures (百度风投), Sinovation Ventures (创新工场), CAS Star (中科创星), and others.

Deemos (影眸科技)

Strategic round, hundreds of millions of RMB, valuation undisclosed

A Shanghai startup selling 3D content tools to ByteDance, Unity, and Canva.

Deemos builds generative AI that creates three-dimensional objects, the kind of 3D models used in games, product visualization, film, and virtual worlds. Where image and video generation AI have attracted most of the attention, 3D generation has been a harder problem: objects need to look correct from every angle, with proper geometry, texture, and lighting. Deemos’s latest model, Gen-2.5, introduced test-time scaling, where the AI allocates more computing time to harder requests. Generating a simple cube gets a quick pass; generating a detailed human face with correct geometry from every angle gets five times the compute. The result is models with up to 10 million polygons, roughly the detail level of a professional 3D artist’s work.

About 80% of the company’s revenue comes from international customers, with Unity, Figma, and Canva among its global clients alongside domestic giants like ByteDance. That international revenue mix is notable for a Shanghai-based AI company, it suggests the product is competing on quality in global markets rather than relying on domestic demand. Subscribers and annual recurring revenue grew over 400% month-on-month following the Gen-2.5 launch.

Founded in 2020 at ShanghaiTech University’s MARS lab by Wu Di, who was 23 at the time, Deemos competes with VAST/Tripo AI in what is becoming a real-time category race for 3D generative AI. The company maintains offices in Singapore and Los Angeles alongside its Shanghai headquarters.

Investors: Cathay Capital (凯辉基金, co-lead), Shanghai State-Owned Capital Investment Pioneer Fund (上海国投先导, co-lead), ByteDance, Sequoia China, Meituan DragonBall Capital (美团龙珠), Lanchi Ventures (蓝驰创投).

Transtreams (凌川科技)

A+, hundreds of millions of RMB, valuation undisclosed

A Kuaishou spinout chip that beats Intel and NVIDIA at video compression.

Transtreams builds a specialized chip called the SL200 that handles two tasks most data centers currently split across separate hardware: compressing video for streaming and running AI inference calculations. The company reports that the SL200 has placed first in multiple editions of the MSU Video Codecs Comparison, an independent benchmark run by Moscow State University’s Graphics and Media Lab that the streaming industry uses to compare how different chips compress video without degrading quality. The company claims a 30-35% compression efficiency improvement over NVIDIA’s latest encoder using AV1, the current industry-standard video compression format, meaning the same video quality at roughly a third less bandwidth and storage cost.

The company spun out of Kuaishou, one of China’s largest short-video platforms, in March 2024. CEO Liu Lingzhi was Kuaishou’s VP and head of its internal chip program, and was the first employee of Kuaishou’s computing center. The chip started with an immediate customer: Kuaishou’s own data centers, where it now covers 99.7% of live-stream transcoding. Total sales have reached approximately 100,000 chips, and Baidu Cloud is now a customer as well. Baidu Ventures also invested in this round, making it both a customer and a shareholder.

This is a chip story where the product shipped and scaled before the major fundraising rounds. In a semiconductor sector where most companies are pre-revenue and raising on roadmaps, Transtreams has 100,000 units in production, a benchmark record, and two of China’s largest internet companies as paying customers.

Investors: Qifu Capital (啟赋资本, lead), Xinguodu (新国都), Jinpu Investment (金浦投资), Zhaohui Capital (朝晖资本), Baidu Ventures (百度风投), Shuimu Investment Group (水木投资集团), Yizhuang Kechuang Fund (亦庄科创二期基金), and others.

HYLICreate (合源锂创)

A round, hundreds of millions of RMB, valuation undisclosed

Xiaomi bets on a solid-state battery factory that’s already running.

Solid-state batteries, which replace the liquid electrolyte in conventional lithium-ion cells with a solid material, have been “five years away” for roughly a decade. The promise is higher energy density (more range per kilogram), faster charging, and reduced fire risk. The reality has been persistent manufacturing challenges that keep most companies at the pilot-line stage.

HYLICreate is trying to change that timeline. Founded in Suzhou in January 2023 by Dr. Liu Min, a former solid-state battery technology director at Dongfeng Automobile, the company built a factory in Huai’an, Jiangsu, that launched in early 2026. The company uses an oxide-based solid electrolyte, a ceramic material that is more stable and less likely to react with the battery electrodes than the sulfide-based alternatives favored by Toyota and Samsung, though harder to manufacture at scale. That stability-over-scalability tradeoff is why HYLICreate is targeting drones, low-altitude aircraft, robotics, and light electric vehicles rather than passenger cars: smaller batteries are more forgiving, and the energy density advantage matters most in applications where weight is a constraint.

The lead investor is Xiaomi Yangtze River Fund (小米长江基金), Xiaomi Group’s industrial investment arm. Xiaomi entered the EV market in 2024 and is building out a battery supply chain. Investing in solid-state battery manufacturing, even at the non-automotive end of the market, signals that Xiaomi is positioning for a technology transition that most of the auto industry has been pushing to “next decade.” The competitive landscape includes QingTao Energy, which has SAIC as a major backer and leads global solid-state battery commercialization, and WeLion New Energy, which filed for a ChiNext (Shenzhen growth board) IPO at a ¥18.5 billion valuation in late 2025.

Investors: Xiaomi Yangtze River Fund (小米长江基金, lead), Zhongbao Fund (中保基金), Chengdu Scientific Innovation Investment (成都科创投), Yangtze Green Water Fund (长江绿水基金), and one unnamed industry partner.

Also on the Radar

Kunlun Xing (昆仑行机器人) — Pre-A, undisclosed amount, ¥9B (~$1.25B) valuation. A 90-day-old robotics company valued at ¥9 billion with zero product. Founded by alumni of Alibaba Cloud and Li Auto, all eight investors re-committed across three rounds in 90 days. The market is pricing founder pedigree from tier-one tech companies at unicorn valuations before a prototype exists.

AGILINK (临界点) — Series B, ¥1B (~$139M), ¥10B (~$1.39B) valuation. Five months from founding to unicorn, but unlike most instant unicorns, AGILINK actually has revenue. Spun out of AgiBot, the company has shipped over 8,000 dexterous robot hands and reports profitability in Q1 2026.

Striding AI (正行创新) — Angel, near $100M, ¥1.95B (~$271M) valuation. Lead investors Charoen Pokphand (12,000+ retail stores) and Huaqin Technology, a contract manufacturer that builds smartphones for major brands under their labels, are also the company’s first deployment sites and training data sources. The founder’s third startup, after AI chips and rockets.

SENAD (赛那德) — Series C, ¥300M (~$42M), ¥2.6B (~$361M) valuation. Autonomous loading and unloading robots for logistics warehouses, deployed across tobacco, e-commerce, and industrial sites. Prior investors include Sinotrans and Alibaba. Investors include Yuanhe Houwang (元禾厚望) and Yuanhe Puhua (元禾璞华).

Jiangxing AI (江行智能) — C+D rounds, hundreds of millions of RMB, ¥5B (~$694M) valuation. Eight-year-old physical AI company for energy and industrial applications. The company reports 1,500+ site deployments, a ¥5 billion (~$694M) order book, and profitability in 2025. Three fundraising events in 2026 alone. CATL-affiliated Chendao Capital, Jinkosolar, and Yanzhou Energy all invested as customer-shareholders.

Argo Space Technology (吉天星舟) — Series B, hundreds of millions of RMB, ¥1.5B (~$208M) valuation. Manufacturer of optical imaging and sensing systems installed on satellites, the hardware that actually observes the Earth or communicates through space. The company reports 55 payloads delivered, 30 currently in orbit, a 100% mission success rate, and breakeven in 2025.

Artivila (科辉智药) — Series A, nearly ¥100M (~$14M), ¥500M (~$69M) valuation. AI drug discovery that went silent for four years between fundraising rounds, then returned with actual Phase I clinical data on ARD-885, a drug targeting inflammatory diseases. In a sector where most AI pharma companies have no molecules in human trials, Artivila returned from four years of silence with a drug in Phase I.

Juhe Jubian (聚合聚变, roughly “Convergent Fusion”) — Angel, hundreds of millions of RMB, ¥1.5B (~$208M) valuation. A fusion energy startup in Hefei co-led by Hillhouse Ventures and Sequoia China, an unusual pairing at the angel stage. Chinese fusion startups are splitting into three camps by chamber design: the tokamak (a donut-shaped magnetic chamber, the approach used by ITER, the 35-nation international fusion research project), laser fusion (firing lasers to implode a fuel pellet), and field-reversed configuration, a more compact cylindrical magnetic field. Juhe Jubian uses the third. Based in Hefei, where China’s EAST experimental fusion reactor is also located, the third Chinese fusion deal in three consecutive weeks.

Fuxi Quantum (伏曦量子) — Angel, undisclosed amount. CATL, the world’s largest battery maker, leading a quantum computing angel round. CATL’s investment portfolio now spans AI models (a reported ¥5 billion in DeepSeek), industrial AI (Jiangxing AI), and quantum computing, building positions well beyond its battery core.

Zhiyue Spatial Intelligence (知跃空间智能) — Angel 5+ round, hundreds of millions of RMB, ¥3B (~$417M) valuation. A robot intelligence company betting on neuromorphic AI, computing systems that mimic the structure of biological neurons, processing information in sparse, event-driven bursts, firing calculations only when sensor data changes, rather than the constant matrix calculations that transformer models (the architecture behind ChatGPT and most modern AI) use. Neuromorphic chips consume a fraction of the power and react to sensor inputs in real time, which matters for robots that need to process continuously without draining their battery. A contrarian bet: the transformer has won almost every AI benchmark of the last five years, but its energy cost may be prohibitive for untethered robots.

The Bigger Picture

When Aramco Invests Twice: Green Hydrogen’s Quiet Cross-Bloc Alliance

Advanced semiconductors face export controls, entity lists, and deliberate supply-chain separation between the US, China, and their respective allies. AI models face similar pressures. Energy transition technology is moving in the opposite direction.

When Aramco Ventures invested in HYDOtech in December 2024, it was the Saudi oil giant’s first hydrogen investment anywhere in the Asia-Pacific region. Eighteen months later, it came back for a second round. In the same period, Sinopec Capital, the venture arm of China’s state oil company, deepened its own position. Conch Group, whose cement plants are among China’s largest industrial emitters, bought strategic equity. Shell and TotalEnergies signed project partnerships for green hydrogen production.

The logic is economic, not ideological. China holds approximately 65% of global installed electrolyzer capacity, and Chinese manufacturers produce systems at roughly $600 per kilowatt, a quarter of the cost of non-Chinese alternatives. Saudi Arabia needs the technology for its own economic diversification. Industrial emitters need it for decarbonization. There are no export controls on electrolyzers, no entity lists blocking hydrogen collaboration.

The capital flows extend well beyond one startup. Saudi Arabia’s Public Investment Fund has invested $22 billion (~¥158B) in China, with clean energy as a priority. ACWA Power, the Saudi renewable energy developer, has long-term plans reaching $50 billion (~¥360B) in clean power assets by 2030, with a substantial share in Chinese solar, wind, and hydrogen. CYVN Holdings, an Abu Dhabi government vehicle, invested a combined $3.3 billion (~¥23.8B) in NIO across two tranches.

HYDOtech’s cap table reflects what these broader flows confirm: the countries with the most urgent need for energy transition technology are investing in China regardless of the broader geopolitical environment. Semiconductor supply chains face deliberate separation through export controls and entity lists. Green hydrogen supply chains are moving in the opposite direction.

The Gaming Engine Hedge: Why Three Game Studios Invested in a Robot Simulation Company

Three A-share listed companies whose businesses span mobile gaming, industrial conveyor belts, and military logistics all ended up on the cap table of the same physical AI data startup. Giant Network, BOTON Technology, and 37 Interactive Entertainment all hold positions in Lightwheel AI, the robot simulation company profiled above.

The infrastructure connection between gaming and robotics was covered in the Lightwheel Spotlight above. What the Bigger Picture adds is the investor behavior: none of the three publicly framed their investments as “transferring gaming physics expertise to robotics.” Giant Network described it as expanding its AI infrastructure portfolio. 37 Interactive positioned it as part of a broader AI strategy that includes investments in over 30 hard-tech companies, from Zhipu AI to Moonshot AI (月之暗面).

BOTON Technology’s investment rationale is the most revealing. Listed on Shenzhen’s ChiNext board (China’s growth enterprise market, similar to NASDAQ), the company’s original business is manufacturing rubber conveyor belts for mining, ports, and steel mills. It acquired a mobile gaming business in 2015. Its stated rationale for Lightwheel was that its mine shafts and factory floors provide real-world environments that complement Lightwheel’s virtual simulations, closing the gap between simulated and physical robot training.

37 Interactive first invested in Lightwheel’s A/A+ round in November 2025, months before the company reached unicorn status, and has followed on in every subsequent round. That early conviction, combined with its separate positions in multiple large language model companies, reads as a bet that physical AI infrastructure is the next computing platform.

Physical AI investment is pulling capital from unexpected sectors. Gaming companies, industrial manufacturers, and state-backed science funds are converging on the same infrastructure layer. The robots that will eventually clean factory floors, navigate warehouses, and drive delivery vehicles all need to train somewhere first, and the companies that control that training environment are attracting investors from every corner of the economy.

This week’s data makes one thing clear: the most revealing capital flows are the ones where the investor is also the customer. Aramco backed the electrolyzer company whose technology it needs for Saudi diversification. Baidu invested in the chip that runs its own video pipeline. Xiaomi funded the battery factory its vehicle division will eventually need. Three gaming companies invested in robot simulation because their physics engines share the same technological foundation. Customer-investors are becoming the norm, not the exception.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.