The China Round — June 5, 2026

Two billion-dollar robot startups, an AI that builds 3D worlds, and the race for a homegrown chip stack

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows is where talent concentrates, where production capacity gets built, and where the next commercial technologies will come from.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

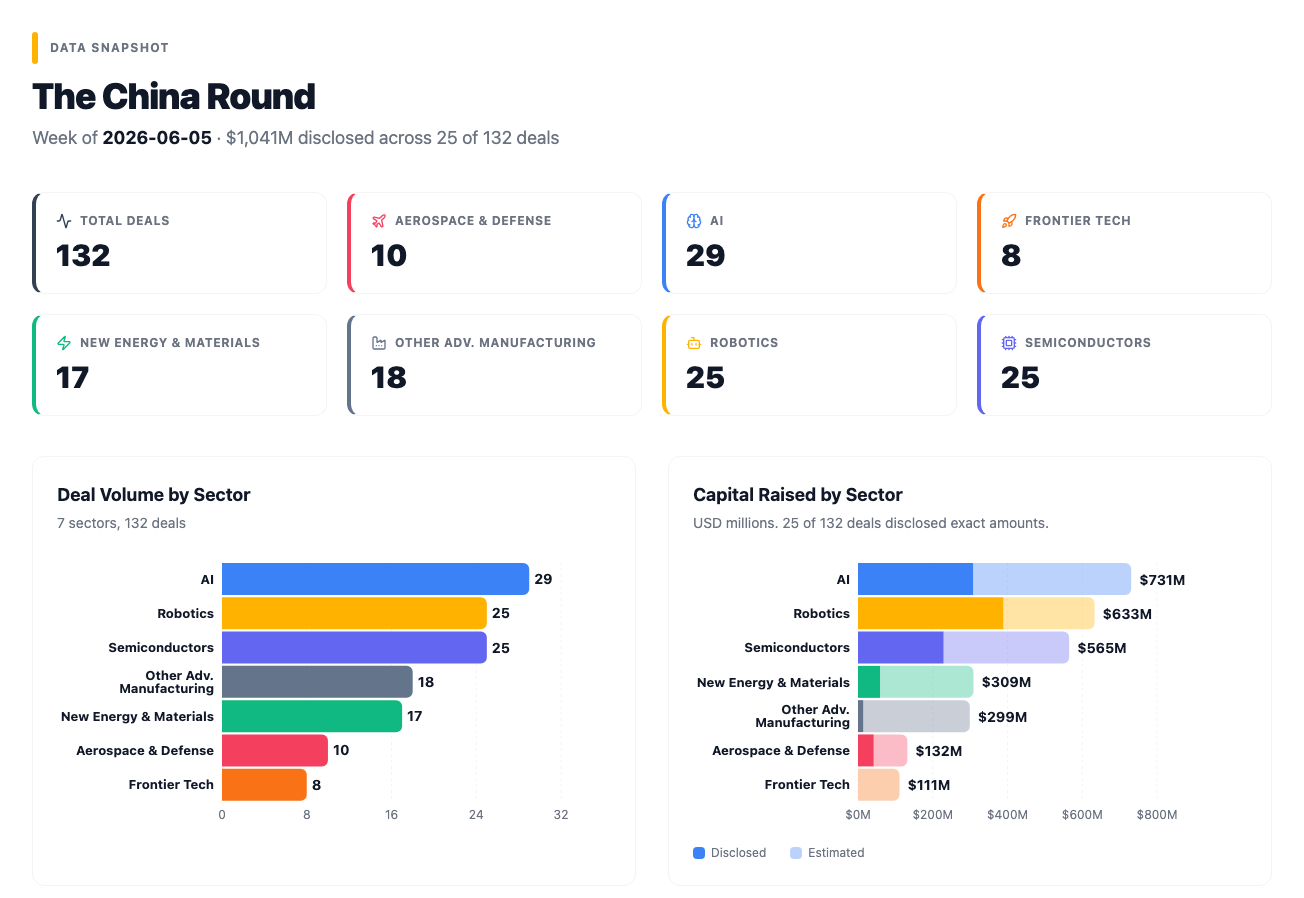

This was one of the busiest weeks of the year, with 132 deals in seven days. Two humanoid robot unicorns, a $200 million 3D AI round, and a wave of quantum deals backed by something closer to industrial policy than venture capital.

Where the Money Went

132 deals crossed the wire this week. About half published some indication of the amount raised, with 25 deals disclosing exact figures for a combined total of ~$1 billion (~¥7.5 billion). The real figure is substantially higher: most early-stage Chinese rounds never publish an amount, so treat that as a floor. The biggest individual checks went to humanoid robotics, but the broader story is breadth: every sector had at least eight active deals, and several had more than twenty.

🧠 AI (29 deals)

AI led the week by deal count, anchored by two outsized rounds. VAST (also known as Tripo AI) raised $200 million (~¥1.44B) for its 3D AI foundation model, while LightLink Tech (光联芯科) raised ¥500 million (~$69M) for optical chip-to-chip interconnect, a technology that replaces the copper wires between processors with laser light to keep up with AI compute demands. The rest of the sector split between AI agents, life science automation, and data infrastructure. Several deals went to companies building the training data that physical AI systems need: embodied intelligence is generating its own supply chain.

⚡ New Energy & Materials (17 deals)

Battery materials and energy storage continued their quiet grind. No single blockbuster, but steady capital into cathode and anode materials, lithium-ion cell makers, and advanced-materials plays. The largest disclosed amounts were modest: ¥140 million (~$19M) for a flexible photovoltaic company and ¥88.2 million (~$12M) for a lithium iron phosphate subsidiary. The sector’s capital arrives incrementally, round after round, without the headline figures that robotics and AI command.

🔬 Semiconductors (25 deals)

The second-busiest sector and the most strategically dense. A subsidiary of chip-design house Montage Technology (澜起科技) raised ¥500 million (~$69M) for switch chips that control how processors and memory share data inside an AI data center, the routing layer that determines whether thousands of chips work together efficiently or spend most of their time waiting on each other. Supercore (超摩科技) raised ¥305 million (~$42M) for processors built from smaller, stackable tiles rather than one large chip, a design that lets manufacturers match high-end performance using fabrication processes they have access to domestically. LEDA Tech (立芯软件) took ¥300 million (~$42M) for EDA tools, the software engineers use to design chips before fabrication. And at the other end of the spectrum, Sibai Chuang (偲百创) was acquired at a distressed valuation by listed RF chipmaker Wisecore for vertical integration. The stage distribution skewed early, with several angel and Pre-A rounds targeting advanced chip packaging, processors that compute directly inside memory chips, and display semiconductors.

🤖 Robotics (25 deals)

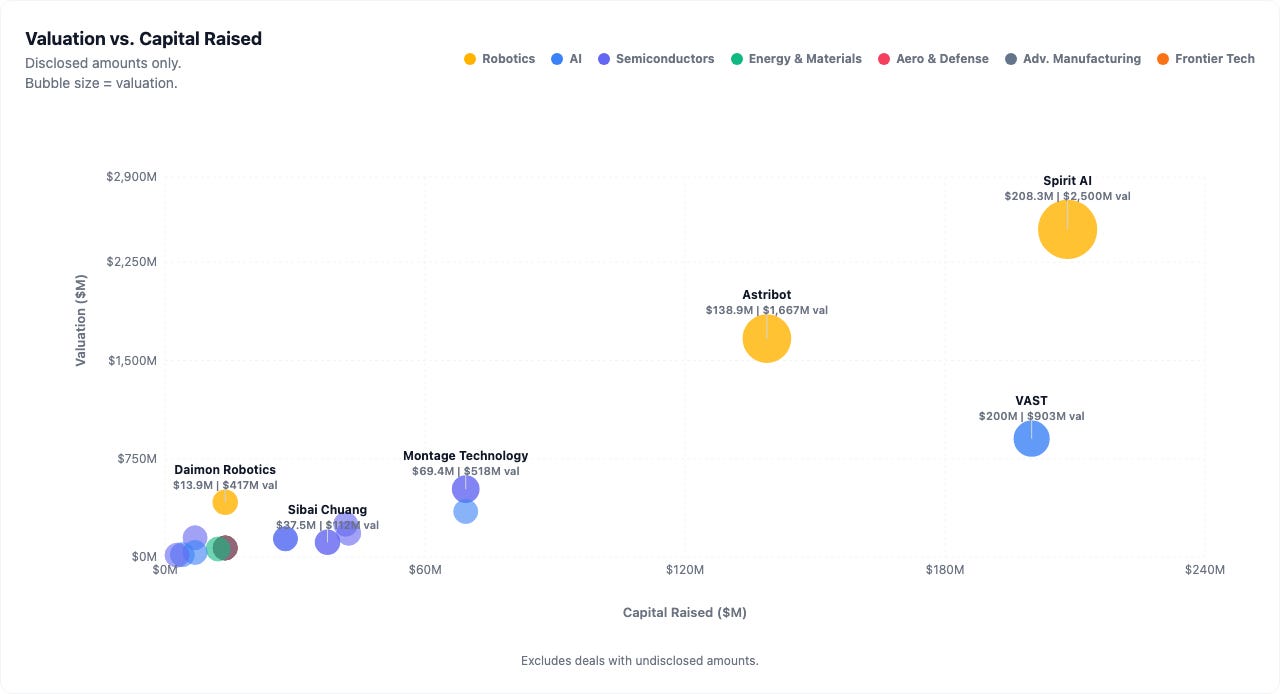

The biggest individual checks of the week. Spirit AI (千寻智能) raised ¥1.5 billion (~$208M) at a ¥18 billion (~$2.5B) valuation, its sixth round in twelve months. Astribot (星尘智能) closed a ¥1 billion (~$139M) Series B at ¥12 billion (~$1.67B). Below those flagships, capital concentrated in components and data rather than finished machines: dexterous hands, tactile sensors, force-torque sensors, tendon-drive mechanisms, and the training data that teaches robots to manipulate real objects all drew more rounds than complete humanoid systems.

💡 Frontier Tech (8 deals)

Eight deals, three of them quantum. HyQubit (华翊量子) raised its A+ from a 10-investor national syndicate for quantum computers that trap individual atoms with lasers to perform calculations. FieldQuantum (量坤科技), a five-month-old quantum-AI middleware company with no product, raised hundreds of millions at a ¥1.8 billion (~$250M) valuation. GGQuanta (国光量子) completed its third round in three months from industrial and strategic listed companies. The non-quantum deals included two brain-computer interface startups and a simulator for modeling nuclear fusion reactions.

🚀 Aerospace & Defense (10 deals)

Satellite communications, eVTOL (electric vertical-takeoff aircraft, essentially flying taxis), and space. Interstellor (穿越者) raised ¥100 million (~$14M) for crewed spacecraft that fly to the edge of space and return without entering orbit, a market aimed at space tourism and high-altitude research. SparkSpace (星火空间) took a Pre-A for liquid rockets that use electric motors to feed propellant rather than traditional turbopumps, a simpler design suited to small satellite launches. The rest was early-stage: satellite-based Earth observation, rocket propellant tanks, and UAVs. Disclosed aerospace capital was modest, about $28 million (~¥200M), but the deals are concentrated in hardware categories that take years and billions to reach scale.

⚙️ Other Adv. Manufacturing (18 deals)

The catch-all sector, and this week mostly components. Kunwei Technology (坤维科技) raised ¥100 million (~$14M) for six-axis force-torque sensors, the kind of touch-sensitive joint that lets a robot arm know exactly how hard it is pressing and adjust in real time. Servo systems, fiber-optic temperature sensors, and industrial automation filled out the list. Stage distribution was scattered: from angel rounds for polishing robots to a Series D for an optical sensing company.

Spotlight

Spirit AI (千寻智能)

A+, ¥1.5 billion (~$208M), ¥18 billion (~$2.5B) valuation

The humanoid robot company that beat global benchmarks and raised nearly ¥5 billion in three months.

Spirit AI builds humanoid robots and the AI models that control them, and this week it became the most visible symbol of where Chinese robotics capital is going. Founded in Hangzhou in January 2024, the company’s Moz1 humanoid runs on Spirit, a proprietary AI model that takes in what the robot sees and spoken commands, then directly outputs the physical movements needed to execute the task, seeing, understanding, and acting in one loop rather than three separate systems. In June 2026, Spirit v1.6 topped the RoboArena global benchmark, a public leaderboard where researchers submit robot control models for head-to-head comparison. It beat Nvidia-affiliated Cosmos3-Nano-Policy in second place and DreamZero in third. Earlier, in January, Spirit v1.5 beat Physical Intelligence’s Pi0.5 on RoboChallenge, a separate benchmark testing how well robot AI generalizes to unfamiliar tasks. The robot is not just a demo: it is deployed on CATL’s battery pack assembly lines with a reported success rate above 99%, and at JD.com retail operations.

The team behind the pace is unusually deep. CEO Han Fengtao (韩峰涛) co-founded and was CTO of Rokae (珞石机器人), one of China’s established collaborative robot makers. Chief Scientist Gao Yang (高阳) holds a PhD from UC Berkeley, where he trained under Pieter Abbeel, a pioneer in robot reinforcement learning at UC Berkeley who co-founded robot learning company Covariant. Combined, the ¥1.5 billion A+ brings Spirit AI’s total to nearly ¥5 billion (~$694M) raised in three months. That fundraising velocity, plus a rare co-investment from Yunfeng Capital (Jack Ma’s fund) and Shunwei Capital (Lei Jun’s fund), signals that Alibaba and Xiaomi ecosystem capital has converged on the same bet, treating physical AI as the next platform war.

Investors: Yunfeng Capital (云锋基金) and Shunwei Capital (顺为资本) co-invested. Gengxin Capital (庚辛资本) as financial adviser.

VAST / Tripo AI

A+/A++, ~$200 million (~¥1.44B), valuation $1 billion+ (~¥7.2B+)

China’s best-funded 3D AI company, and it’s taking on a $5 billion American rival.

VAST builds AI models that generate three-dimensional objects from text descriptions or images, the 3D equivalent of what DALL-E and Midjourney do for pictures. Its Tripo platform has roughly 20 million users globally, the majority in the United States, with about 150 staff across Beijing and Hangzhou. Enterprise clients include NetEase, Sony, Tencent, ByteDance, and Microsoft. This round, combining A+ and A++ tranches, pushes total fundraising to roughly $250 million (~¥1.8B) and tips the company past the $1 billion valuation mark.

CEO Song Yachen (宋亚宸), born in 1997, studied theology at Johns Hopkins, then became founding employee number one at MiniMax, the Chinese AI lab behind the Hailuo video model. He left to start VAST at 26. The company’s research arm, Project Eden, is building a “world model,” AI that simulates entire 3D environments rather than generating objects one at a time, a direct challenge to World Labs, the $5 billion startup founded by Stanford AI pioneer Fei-Fei Li, which raised $1 billion in February 2026. The market for AI-generated 3D content underpins everything from game development to architecture to virtual retail, and it is large enough, and the race urgent enough, that both the American and Chinese champions are being funded to the hilt at the same time.

Investors: Ince Capital (渶策资本, lead), China Life Private Equity (国寿股权), Alibaba, Baidu Ventures, Primavera Capital, and others. Yuanshi Capital (远识资本) as financial adviser.

Aippy

Series A, tens of millions of USD, ~$250 million valuation

An AI game creation platform built in China for Western players.

Aippy lets users describe a game in natural language and plays it back as a working mini-game within seconds. Think of it as interactive TikTok, where every post is playable. The platform is a pure overseas product, built for the US and European markets, with a 4.8-star rating on the US App Store and a company-reported 3 million-plus downloads. Users have generated over 2 million games on the platform, and the company reports daily engagement of nearly 50% of monthly actives. The app operates under NADA AI, a subsidiary of Hong Kong-listed Newborn Town (赤子城科技), which incubated the product before spinning it off for external funding.

Chinese companies have struggled to export consumer AI products to Western markets; most of the cross-border traffic flows the other direction. Aippy is a rare case of a Chinese-built, Chinese-funded consumer AI product competing natively in the US App Store, not as a China story exported but as a product Western users are adopting on its own merits. Founder Evan Yip (叶椿建), CTO of Newborn Town, has a track record building social apps for overseas audiences. If the retention numbers hold, it will serve as evidence that Chinese teams can build consumer AI products for overseas markets.

Investors: Glowill Capital (歌未资本, lead).

LightLink Tech (光联芯科)

Series A, ~¥500 million (~$69M), ¥2.5 billion (~$347M) valuation

Optical chip-to-chip interconnect for AI clusters, and the most consensus-rich deal on the list.

LightLink Tech, incorporated in Beijing in February 2024, builds optical I/O chips: tiny photonic circuits that replace the electrical copper connections between processors with light. The problem they solve is concrete and growing. AI clusters are scaling to tens of thousands of chips working in concert, and the data flowing between those chips is outrunning what copper traces can carry. Electrical connections lose signal strength over distance and generate heat; photonic interconnects carry data farther, faster, and cooler. That is why the space has exploded globally. In March 2026, Silicon Valley’s Ayar Labs closed a $500 million Series E at a $3.75 billion valuation. In May, Marvell acquired competitor Celestial AI for $3.25 billion, with earnouts up to $5.5 billion. LightLink Tech’s A round represents the largest early-stage financing for optical I/O in China.

Gaorong Capital, Lenovo Ventures, and Cornerstone Ventures came in new; Sequoia China, Hillhouse, and Legend Capital followed on from prior rounds. The round closed within a single month. A round closing that fast, with that combination of top-tier VCs converging on a pre-commercial company, reflects strong consensus that optical I/O is critical infrastructure for the next generation of AI clusters. If China’s AI clusters are going to scale without dependency on Western photonic interconnect, this is one of the places where the domestic alternative is being funded.

Investors: Gaorong Capital (高榕创投, lead), Lenovo Ventures (联想创投), Cornerstone Ventures (基石资本), Sequoia China (红杉中国), Hillhouse (高瓴), Legend Capital (君联资本), and others. Duowei Capital (多维资本) as financial adviser.

HyQubit (华翊量子)

A+, undisclosed amount, valuation reported at ¥3.6 billion (~$500M)

Ten investors, one quantum computer, and a signal that reads more like policy than venture capital.

HyQubit, spun out of Tsinghua University’s Quantum Information Center, builds quantum computers using trapped ions: individual charged atoms suspended in electromagnetic fields and manipulated with laser pulses to perform calculations. It is one of the three main hardware approaches to practical quantum computing, alongside superconducting circuits and photonic chips. HyQubit is among the most-funded ion-trap specialists in China. The company’s HYQ-B100 system, capable of stable operation at over 100 qubits, has been delivered to the China Mobile Research Institute, a confirmed commercial customer.

What makes this round unusual is the investor composition. Ten investors participated, led by Jianyin Investment (建投投资), a private equity arm of Central Huijin Investment, China’s state financial holding company. New investors include CRRC Capital (中车资本, the investment arm of China’s state rail company) and CITIC Construction Investment (中信建投资本). Follow-on investors include Baidu Ventures, Legend Capital, and the Beijing Information Industry Fund. The chief scientist is Duan Luming (段路明), a Chinese Academy of Sciences academician and director of Tsinghua’s Quantum Information Center, one of the leading figures in Chinese quantum research. The breadth of the syndicate, spanning state banks, rail, telecom, and defense-adjacent institutions, suggests that ion-trap quantum has moved from a research curiosity to a nationally coordinated investment priority.

Investors: Jianyin Investment (建投投资, lead), CRRC Capital (中车资本), CITIC Construction Investment (中信建投资本), Dunhong Asset (敦鸿资产), Baidu Ventures (百度风投), Legend Capital (君联资本), and others.

Sibai Chuang (偲百创)

Strategic investment, ¥270 million (~$37M), ¥808 million (~$112M) implied valuation

An RF chip startup with real technology, negative net assets, and a listed buyer getting it at a discount.

Sibai Chuang, based in Suzhou, makes radio-frequency acoustic wave filters, the tiny components inside every phone and base station that separate one wireless signal from another so that calls, data, and GPS do not interfere with each other. The company builds several generations of these filters, from conventional surface-wave designs to newer, higher-frequency variants, and has developed a proprietary version it calls UltraLAW, which handles the millimeter-wave frequencies that 5G and future 6G networks require. The company says it is among the first to reach commercial production of this design. This week, Wisecore (唯捷创芯, 688153.SH), a Shanghai-listed RF front-end chipmaker, paid ¥270 million for a 33.4% stake, implying a valuation of roughly ¥808 million (~$112M). That is a markdown from the 2023 Pre-A.

The price tracks the financials. Per Wisecore’s public filing, Sibai Chuang had revenue of ¥7.44 million (~$1M) in 2025, a net loss of ¥56.77 million (~$7.9M), and negative net assets of ¥137 million (~$19M). Founder Gong Songbin (龚颂斌) is an Associate Professor of Electrical and Computer Engineering at the University of Illinois at Urbana-Champaign and an IEEE Senior Member. The technology is genuine; Lamb wave filters handle higher frequencies than conventional designs and matter for 5G and future 6G bands. But the balance sheet shows a company that has spent through its prior funding without reaching commercial scale. Wisecore’s rationale is vertical integration: combining its power amplifier chips with Sibai Chuang’s filters creates the kind of integrated front-end package that every smartphone needs and that Chinese phone makers currently buy from American suppliers like Qualcomm and Skyworks, one compact component containing amplifier, filter, and signal switch. This is a deal about supply chain autonomy, priced to reflect Sibai Chuang’s balance sheet rather than its technology.

Investors: Wisecore (唯捷创芯, 688153.SH, sole).

Also on the Radar

Astribot (星尘智能). Series B, ¥1 billion (~$139M), ¥12 billion (~$1.67B) valuation. The company claims to be the first globally to mass-produce rope-driven humanoid robots, which replicate the mechanics of human tendons rather than using conventional gears. Thousands of units delivered in 2025, with the T1 model priced at ¥89,900 (~$12,500). State tech fund Guoke Investment (国科投资) and Ant Group on the cap table.

Botshare (擎天租). A+, hundreds of millions of RMB, ¥7 billion (~$972M) valuation. A robot-as-a-service platform co-founded by Agibot (智元机器人), one of China’s better-funded humanoid robot makers, in December 2025. Over 4,000 robots deployed across 100+ Chinese cities, with a leasing network operating in 13 countries. Six rounds in six months. The bet is that the deployment model for humanoid robots is leasing, not selling.

GenRobot.AI (简智机器人). Pre-A, hundreds of millions of RMB, ¥1.5 billion (~$208M) valuation. Not a robot maker but a data supplier: wearable systems that capture how humans move and handle objects, generating the real-world training data that robot AI needs to learn dexterous manipulation. Per company materials, over 10,000 hours of training data collected, with the majority of revenue from overseas customers. Ant Group and Didi co-led, with Shunwei continuing.

XYZ Embodied AI (星源智). A round, hundreds of millions of RMB, ¥3 billion (~$417M) valuation. A software and compute platform that acts as the central intelligence layer for humanoid robots, coordinating perception, planning, and action. Incubated by the Beijing Academy of Artificial Intelligence (BAAI), China’s flagship state AI research institute. Per company materials, it supplies over 70% of China’s top embodied AI companies and operates as Nvidia’s largest distribution partner for Jetson Thor, the specialized AI computing module Nvidia designed for humanoid robots. ¥1 billion (~$139M) raised in ten months. CRRC Capital on the cap table.

LEDA Tech (立芯软件). Series C, ¥300 million+ (~$42M+), ¥1.8 billion (~$250M) valuation. EDA tools, the software used to design chips before they are fabricated. The round was led by the China Internet Investment Fund (CIIF), the investment arm of the Cyberspace Administration of China, with prior backing from Huawei’s Hubble fund, Social Security Fund sub-funds, and Shenzhen Capital Group. That the country’s cybersecurity regulator is the lead investor places chip-design software firmly in the national-security category.

Daimon Robotics (戴盟机器人). Series A, ~¥100 million (~$14M), ¥3 billion (~$417M) valuation. Vision-tactile sensing for dexterous robot hands: mm-thin sensors with 40,000 sensing units per square centimeter, roughly 170 times denser than human skin. China Mobile invested in December 2025, China Telecom in June 2026, and Inovance (汇川), the world’s largest industrial servo maker, led this round, an unusual convergence of telcos and the dominant servo company on a single tactile-sensing startup.

Xynova (曦诺未来). Series A, hundreds of millions of RMB, ¥3.6 billion (~$500M) valuation. Dexterous hands for humanoid robots: the Flex 2 hand offers 23 degrees of freedom (independent points of movement, against roughly 27 in a human hand) with fine-grained fingertip force control, and the company manufactures its own 8mm brushless motors and ball screws rather than sourcing them. Li Auto led the round, with Xiaomi and CATL (via Puquan Capital) also on the cap table.

OriginFlow (渊澈太初). Pre-A, over ¥500 million (~$69M) across three rounds in five months, ¥1.5 billion (~$208M) valuation. The founder, Qin Shentao (秦慎涛), was 25 at close: a Tsinghua PhD student who built an embodied AI data company around capturing the electrical signals from human muscles as people perform tasks, a more detailed signal than video or motion capture alone because it records the intent and force behind a movement, not just its shape. A partnership with 58.com gives access to household scenarios no lab can replicate.

FieldQuantum (量坤科技). Angel, hundreds of millions of RMB, ¥1.8 billion (~$250M) valuation. A quantum-AI middleware startup (building the software layer that would let AI systems tap quantum machines) that is five months old, has no shipped product, employs about 40 people, and just raised at a quarter-billion-dollar valuation. The thesis: quantum computers can generate the high-precision simulation data that classical machines cannot, repositioning quantum as AI training infrastructure. The valuation is almost entirely a thesis bet on a future capability.

NCC (微纳核芯). Series B+, undisclosed amount, ¥5 billion (~$694M) valuation. Compute-in-memory AI chips that perform calculations directly where data is stored, avoiding the energy-intensive shuttling between processor and memory that is one of AI’s largest power costs. SMIC’s venture arm (中芯聚源) is an investor, signaling a direct manufacturing relationship.

Xinhan Intelligent (芯寒智能). Pre-A, ~¥100 million (~$14M), ¥1.5 billion (~$208M) valuation. Two-phase liquid cooling for AI data centers: a coolant that boils as it absorbs heat from chips and vents that heat directly, without the large refrigeration units that conventional liquid cooling requires. As AI cluster power density climbs past what air cooling can handle, liquid cooling has gone from niche to mandatory.

Stragglers

Hydwin Robotics (海桓科技). Series C, hundreds of millions of RMB, ¥1.5 billion (~$208M) valuation. Ship hull cleaning robots with a reported 45% domestic market share and international clients reportedly including Maersk and MSC Mediterranean Shipping, deployed across 12 or more countries. International maritime regulations requiring ships to remove marine growth from their hulls, which otherwise slows vessels and spreads invasive species, are creating mandatory demand for automated hull cleaning.

The Bigger Picture

China’s sovereign AI compute stack, assembling one deal at a time

Four deals this week map onto a single thesis. If China’s AI industry is going to scale without dependency on Western technology, it needs to build its own stack from design tools down to cooling systems.

Start with EDA. Electronic design automation software is the first step in making any chip, the tools engineers use to lay out a circuit before it goes to a fabrication plant. Three companies, Synopsys, Cadence, and Siemens EDA (the division Siemens acquired from US-based Mentor Graphics), control over 80% of the global EDA market and over 90% of the Chinese market. China has fewer than 3,000 EDA professionals, a fraction of the headcount at any of the global EDA leaders. In May 2025, the US Bureau of Industry and Security imposed new restrictions on EDA exports to China; those were rescinded in July under a trade truce, but the structural vulnerability was exposed. This week, LEDA Tech raised ¥300 million (~$42M) for its backend EDA tools, led by CIIF, the investment arm of the Cyberspace Administration of China, the country’s cybersecurity regulator. Its money reclassifies chip design software from a commercial product into a national security asset.

Move up the stack. Supercore (超摩科技) raised capital for chiplet-architecture CPUs, processors assembled from smaller, specialized tiles rather than carved from one slab of silicon, which allows manufacturers to use domestically available fabrication processes while approaching the performance of cutting-edge monolithic designs. LightLink Tech raised its Series A for optical chip-to-chip interconnect, the photonic plumbing that connects those chiplets at the speed AI training demands. Xinhan Intelligent raised its Pre-A for two-phase liquid cooling, solving the thermal problem that arrives once thousands of these chips are packed into a single room.

Together, these four deals cover design tools (LEDA Tech), chip architecture (Supercore), interconnect (LightLink Tech), and thermal management (Xinhan Intelligent). None of them is individually sufficient, and none is at commercial scale for the target applications. But the pattern of capital flowing into adjacent layers of the same stack, often from overlapping pools of state-affiliated and strategic investors, suggests something more deliberate than a collection of independent bets.

Quantum crosses into industrial policy

Four quantum deals in a single week: HyQubit (ion-trap, 10-investor national syndicate, ¥3.6 billion valuation), FieldQuantum (quantum-AI middleware, ¥1.8 billion valuation with no product), GGQuanta (国光量子), which uses light particles rather than trapped atoms to run quantum computations and completed three rounds in three months from industrial and strategic listed companies, and a straggler angel for Suidao Zhiyuan (隧穿智元), which is working on quantum computers capable of correcting their own calculation errors in real time. Across all four deals, the investor profiles matter more than the technical distinctions.

The numbers behind the trend are striking. In the first quarter of 2026 alone, Chinese quantum companies raised roughly ¥2.2 billion (~$305M) across 17 deals, nearly matching the full-year total for 2025. Quantum was named among the priority “future industries” in China’s 15th Five-Year Plan, announced in March 2026. Regional governments have allocated an estimated ¥121.8 billion (~$16.9B) through national venture guidance funds covering key tech corridors including Beijing-Tianjin-Hebei, the Yangtze River Delta, and the Greater Bay Area, with quantum among the target sectors.

On the applications side, quantum hardware is increasingly funded by the industries that intend to use it. This week’s GGQuanta round was led by Weide Information (688171.SH), a listed industrial control security company; its prior round was led by another strategic investor. HyQubit’s delivered system sits at China Mobile’s research institute. The checks are coming from prospective customers and state-adjacent strategics, not generalist VCs.

Corporates are replacing VCs as lead investors

Spirit AI was backed by Jack Ma’s Yunfeng and Lei Jun’s Shunwei, ecosystem funds attached to Alibaba and Xiaomi. Sibai Chuang was bought by a listed chip company for vertical integration. Daimon Robotics was led by Inovance, the servo giant, after consecutive investments from China Mobile and China Telecom. Xynova stacked Li Auto, Xiaomi, and CATL on its cap table. HyQubit’s 10-investor syndicate includes state rail, state telecom, state banks, and social security funds.

Corporate venture capital (CVC) had backed 72.5% of China’s unicorn companies by 2025. In the first quarter of 2026, CVC accounted for 46% of all VC deal frequency, with corporate LP funding amounts up 36% year over year. The state and corporate share of limited-partner capital in RMB-denominated funds reached 41% by 2023, up from 20% in 2014, and the trend has only accelerated since. By 2024, an estimated 8,000 industrial groups were active as direct investors, with CVC comprising 37% of all primary market transactions.

What this means for the companies raising: the investor is increasingly also the customer, the distributor, or the regulator. Inovance invests in Daimon because it needs the sensors for its own humanoid robot production, and the same logic applies to every corporate check on this list. China Mobile and China Telecom are buying a window into the hardware that will populate their 5G-enabled smart factories. When the check-writer is also the buyer, it changes the terms. The startup gets a guaranteed channel, but also a tighter leash. For China’s tech ecosystem, the result resembles the old Japanese keiretsu model, where car makers funded their parts suppliers and electronics giants funded their component makers, binding supplier and customer into one financial web.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.