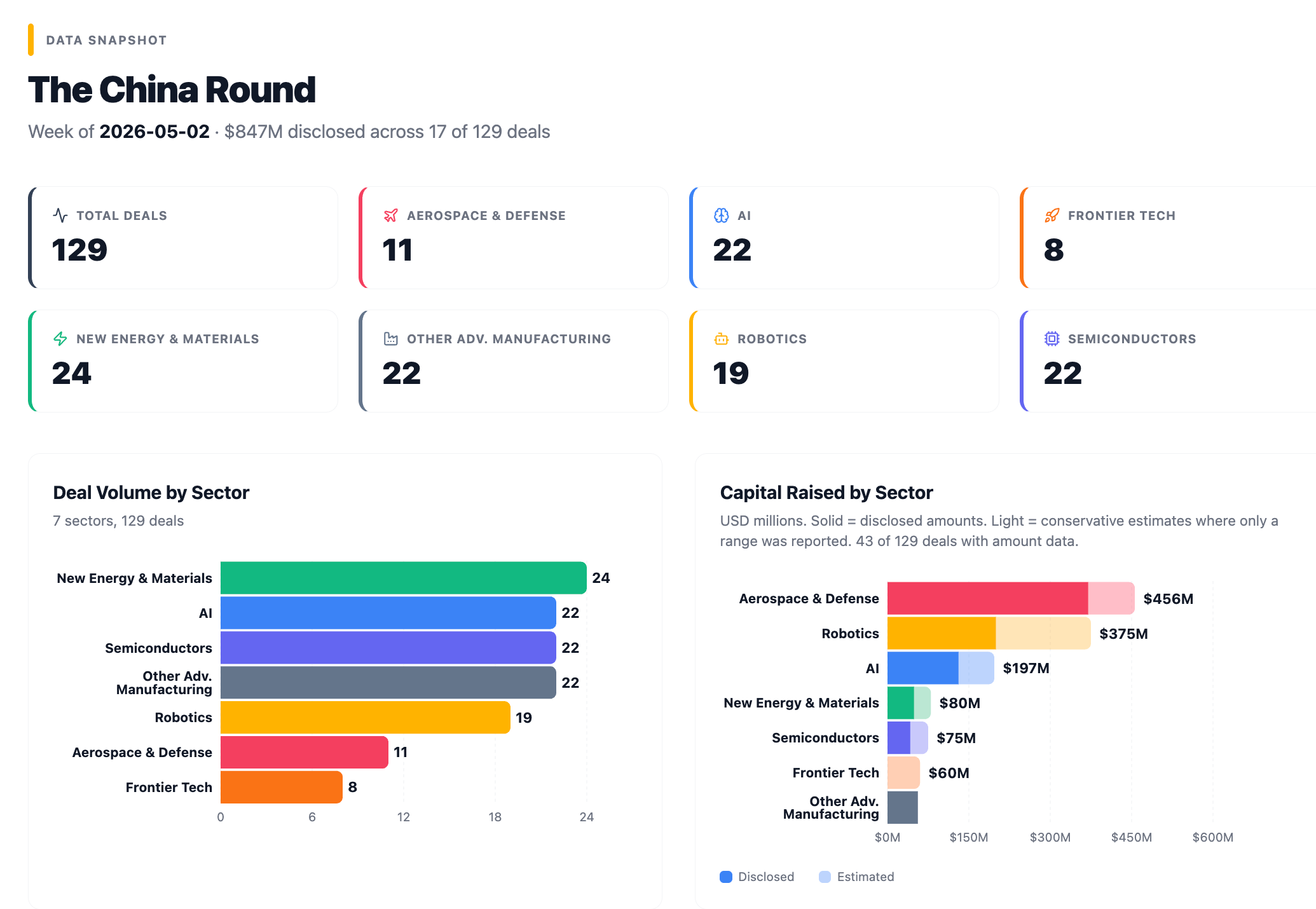

The China Round — May 1, 2026

Record eVTOL Capital, SF Express Bets on Its Own Robot Workforce, and Quantum Goes Commercial

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

Where the Money Went

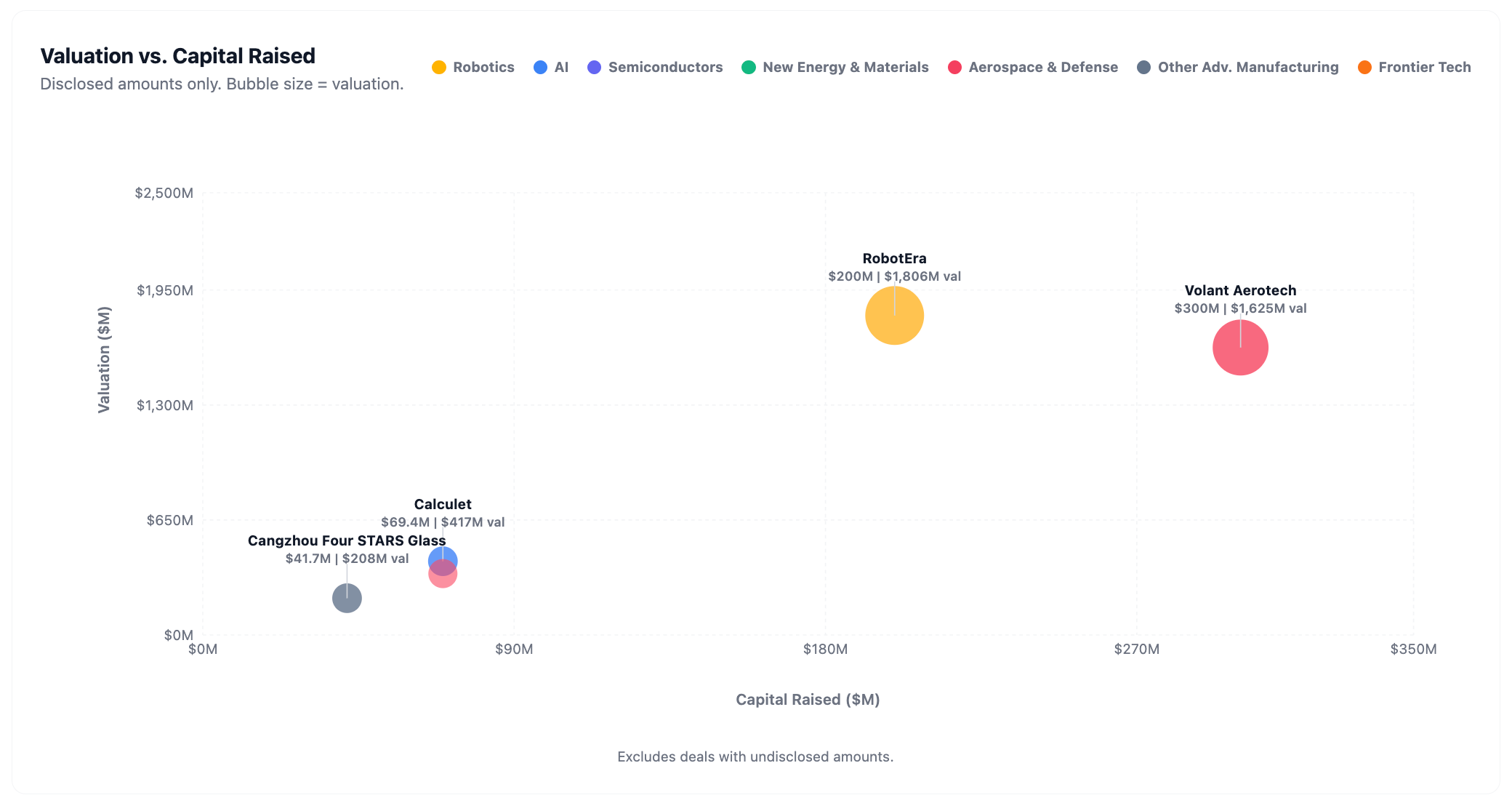

129 deals in seven days, $847M (~¥6.1B) in disclosed capital. Aerospace and defense led on dollar volume at $370M across 11 deals, the lowest deal count of any sector, driven by Volant Aerotech’s $300M Series C and Cosmoleap’s ¥500M (~$69M) Series A; no other sector crossed $200M. Robotics followed at $200M across 19 deals, concentrated in RobotEra’s single large round. The remaining five sectors generated 97 deals and under $280M combined.

🚀 Aerospace & Defense (11 deals)

Two rounds accounted for nearly all disclosed capital. Volant Aerotech closed what multiple Chinese financial outlets confirmed as the largest single round in Chinese passenger eVTOL history: over $300M, with a UAE fund (Stone) leading and Shanghai’s first city-level state capital entering. Cosmoleap closed a ¥500M (~$69M) Series A for its chopstick-catch reusable rocket (the same tower-arm booster recovery system SpaceX uses), covered by SpaceNews. The remaining nine deals are earlier stage, concentrated in urban air mobility, SAR satellite infrastructure, and UAV systems.

🤖 Robotics (19 deals)

SF Express both led RobotEra’s $200M+ strategic round and operates the company’s humanoid robots across 10+ logistics centers. The operator-as-investor structure, where the round lead is also the largest deployment partner, is defining which companies demonstrate commercial traction rather than commercial intent. LinkerBot extended its fundraising to seven rounds in 18 months after shipping 10,000+ dexterous hands. Wujie Power attracted a ¥500M (~$69M) overseas deployment contract from Envision alongside its raise, the largest overseas commercial contract signed by a Chinese embodied AI company to date. Botshare, a robot rental platform launched December 2025, completed its fourth round in 105 days.

🧠 AI (22 deals)

Creati.ai closed a $20M Series B for its Buzzy video editing product, which the company frames as “the world’s first AI Video Photoshop,” reporting $15M in ARR and 20 million+ global users. Spirit AI’s Series A+, a straggler from the April 24 batch with Alibaba as sole lead and a reported ¥5.5B (~$760M) valuation, rounds out the AI highlights. The remaining 20 AI deals are early-stage and mostly undisclosed.

🔬 Semiconductors (22 deals)

IDG Capital led a ¥500M (~$69M) Pre-Series A for Calculet at a reported ¥3B valuation, building AI processors on a chiplet architecture. With access to advanced monolithic nodes constrained by export controls, chiplet designs assembled from available process nodes are emerging as a structural workaround. The remaining 21 deals are early-stage and undisclosed.

⚡ New Energy & Materials (24 deals)

The highest deal count at 24, but only $49M disclosed. QingNa Technology raised ¥200M (~$28M) in a Series A for sodium-ion batteries, with one million large cylindrical cells shipped to European customers in January 2026 and five million contracted for the year. The remaining 23 deals are early-stage and mostly undisclosed.

⚙️ Other Advanced Manufacturing (22 deals)

22 deals, almost entirely undisclosed. Cangzhou Four STARS Glass, a 33-year-old pharmaceutical glass maker, closed the only disclosed round at ¥300M (~$42M) Pre-IPO. The remaining deals are concentrated in industrial automation, precision testing, and manufacturing equipment suppliers, the enabling layer beneath the robotics and semiconductor sectors above it.

💡 Frontier Tech (8 deals)

TuringQ completed a Series B+ for photonic quantum computing, reaching an estimated ¥7B (~$970M) valuation on the strength of ¥100M+ (~$14M) in signed orders in H1 2025 and approaching ¥1B (~$138M) raised in 2026 alone. BCDTEK closed a Series A for silicon-based OLED microdisplays (the display technology inside the Apple Vision Pro) while building China’s first 12-inch silicon OLED fab.

Spotlight

Volant Aerotech (沃兰特航空)

Series C, over $300M (~¥2.16B)

The largest single round in Chinese passenger eVTOL history: UAE capital leads, Shanghai’s first city-level state investor enters, and the order book stands at over 1,900 aircraft.

Volant Aerotech is developing the VE25-100 (Tianxing), a six-seat eVTOL with a 2,500kg maximum takeoff weight and a 200-400km range. The pre-production prototype completed its rollout at the Zigong Aviation Industrial Park in Sichuan in May 2025. China Southern General Aviation signed the first confirmed commercial passenger eVTOL order in China in January 2025, for multiple aircraft at approximately ¥25M (~$3.5M) per unit, deposit paid.

")

The Series C, closed April 27 and led by Stone (UAE), sets a size record for Chinese passenger eVTOL confirmed by multiple Chinese financial outlets and the company’s English press release. Futen Capital (孚腾资本), backed by Shanghai State-owned Capital Investment Co. as its primary shareholder, entered the round in what reporting describes as the first direct investment by Shanghai city-level state capital in a crewed eVTOL OEM, a designation that carries implications for certification support, infrastructure investment, and public procurement. The accumulated order book now stands at over 1,900 aircraft worth more than ¥47.5B (~$6.6B), with confirmed deposits from China Southern General Aviation, Asian Express, and ABC Financial Leasing.

Founder Dong Ming spent over 20 years in civil aviation across AVIC, GE, Rockwell Collins, and Aviage Systems, with direct involvement in the ARJ21, C919, and CR929 programs.

Sequoia China, Futen Capital, Future Capital, and Legend Capital co-invest alongside Stone.

Announcement (Chinese) · Announcement (English)

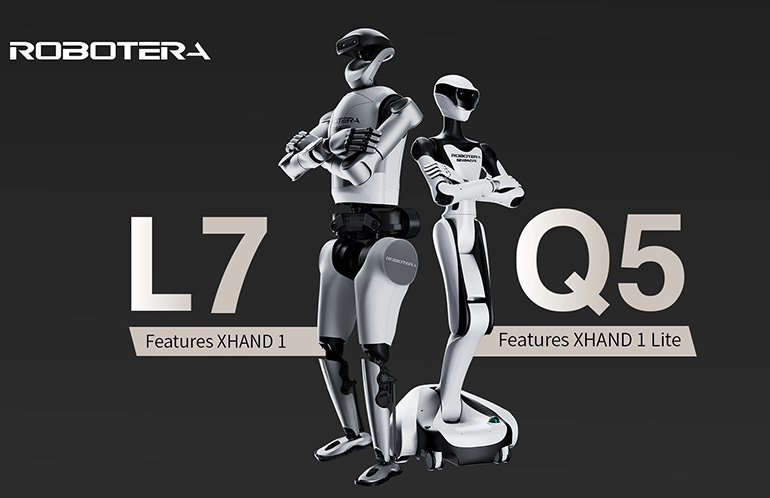

RobotEra (星动纪元)

Strategic Investment, over $200M (~¥1.44B)

SF Express led the round and operates the robots across its own logistics network, the only deal this week where the lead investor is also the operator at production scale.

RobotEra builds full-stack humanoid robots with a stated goal of industrial deployment at scale. Its L7 stands 171cm, weighs 65-70kg depending on configuration, runs 55 degrees of freedom (the count of independent joint movements, a proxy for human-like dexterity), and reaches 4 m/s, among the fastest bipedal humanoids in production. Bimanual carry capacity is 20kg. The XHAND1 dexterous hand adds 12 degrees of freedom as a modular unit. RobotEra develops approximately 95% of its hardware in-house, including motors, sensors, and control systems, a prerequisite it argues for the cost reduction required at deployment scale.

SF Group, China’s largest integrated logistics company, led this round and simultaneously operates RobotEra robots across 10+ logistics centers spanning North, East, and South China. Deployed robots run at 85% of human worker efficiency in logistics environments. RobotEra shipped 600+ cumulative units as of CES 2026 in January and announced thousand-unit scale batch deliveries beginning Q2 2026. SF Express is running robots on its own production lines and backing the supplier with over $200M simultaneously.

Founder Chen Jianyu is an assistant professor and doctoral supervisor at Tsinghua University’s Institute for Interdisciplinary Information Sciences, PhD from UC Berkeley under Masayoshi Tomizuka. Tsinghua University holds equity, described on the company website as unique among humanoid robotics companies.

Sequoia China, IDG Capital, and CICC co-invest alongside SF Group.

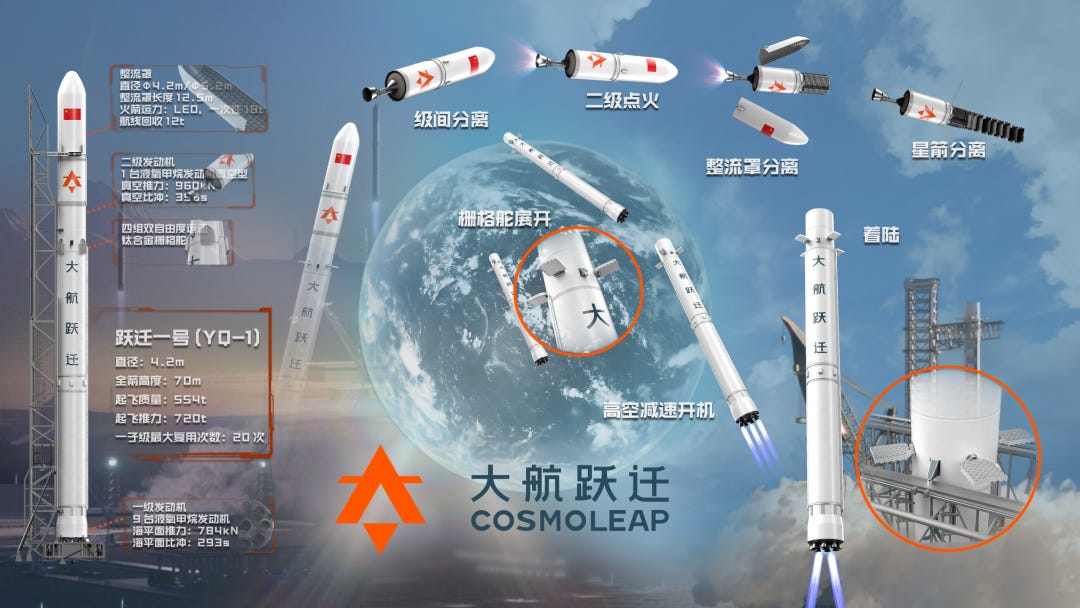

Cosmoleap (大航跃迁)

Series A, ¥500M (~$69M)

Founded February 2024, Cosmoleap has raised approximately $83M in 18 months for a chopstick-catch reusable rocket, with SpaceNews coverage marking rare Western trade press attention for a Chinese launch startup at this stage.

Cosmoleap is developing the Leap-1A (跃迁一号甲), a 70-meter methane/liquid oxygen rocket targeting an 18-ton LEO payload capacity and first flight in 2027. The Qingyu-11 engines are rated for 50 reuses.

The company is testing a tower-catch booster recovery system (the same chopstick-arm architecture SpaceX uses with Mechazilla), with catch tower testing underway since November 2024. A nine-engine first stage burns liquid oxygen and methane.

This Series A, co-led by Houji Capital (厚纪资本) and Puhua Capital (普华资本) with Huaxing Capital as financial advisor, brings total capital raised to approximately $83M (¥100M (~$14M) seed in November 2024 plus ¥500M (~$69M) here) after 18 months of operation. SpaceNews covered the round directly, a level of Western trade press attention rare for a Chinese launch startup at Series A stage. Zhongguancun Development Group entered as a strategic investor.

TuringQ (图灵量子)

Series B+, amount undisclosed

Photonic quantum computing with ¥100M+ in commercial orders, a national guidance fund entering directly, and an estimated valuation of ¥7B (~$970M).

TuringQ builds photonic quantum computers using a full integrated device manufacturer model, designing, fabricating, and commercializing its own chips while operating China’s first photonic chip pilot production line at the Wuxi Photonic Chip Research Institute. Two in-house photonic chip fabrication approaches enable a 2-3 week iteration cycle, fast for a hardware company running its own production line. Products are sold into financial services, quantum cryptography, and scientific computing customers including state-owned enterprises in energy and telecommunications.

The commercial trajectory matters: ¥500,000 (~$69K) in revenue in 2022, over ¥10M (~$1.4M) in 2023, and over ¥100M (~$14M) in signed orders in H1 2025. The 2025 World Internet Conference awarded TuringQ and SJTU’s Wuxi institute its Leading Technology Award, the first time the prize went to a quantum computing project. China’s quantum sector saw investment in Q1 2026 approach full-year 2025 levels, with TuringQ among the largest deals. This B+ is led by Zhangjiang Group (张江集团), Haiwan Capital (海望资本), and Guotou Chuanghe (国投创合, managing the Yangtze River Delta Fund under the National Venture Capital Guidance Fund). Total raised in 2026 alone is approaching ¥1B (~$138M). Estimated valuation: approximately ¥7B (~$970M) per deal trackers.

Founder Jin Xianmin is an assistant professor and 2021 Changjiang Scholar at Shanghai Jiao Tong University’s School of Physics and Astronomy. He holds 150+ publications across Science, Nature Photonics, and Nature Communications and gave up UK residency after his postdoc at Oxford to return and found the company.

Creati.ai (感知阶跃)

Series B, $20M (~¥144M)

A Chinese-founded AI video company launching Buzzy, which the company frames as “the world’s first AI Video Photoshop,” with $15M in ARR and 20 million global users.

Creati.ai launched as ZMO.AI in 2020 generating AI fashion product imagery for e-commerce. It relaunched as Creati in April 2024 with a broader AI content platform. This Series B is structured around the launch of Buzzy: a conversational video editing tool that makes localized edits to existing footage (removing background people, fixing eye contact, adjusting lighting, swapping products) without regenerating the full clip. The company positions Buzzy as “the world’s first AI Video Photoshop,” a deliberate framing against both Adobe and the generative-AI-replaces-everything narrative. It targets video creators and e-commerce merchants who need precise, reversible edits.

The commercial signals behind a $20M round: the company reports $15M in annual recurring revenue and 20 million+ global users. For a Chinese AI SaaS product with USD pricing and international distribution, those figures at this raise size represent one of the stronger commercial profiles in this week’s batch. Founder Ella Zhang (张诗莹) has run the company through both pivots. The prior Series A was led by Hillhouse with GGV Capital and GSR Ventures participating.

Redpoint leads. CCV (创世伙伴创投) co-invests.

Also on the Radar

LinkerBot (灵心巧手)

Series B+, undisclosed

Seven rounds in 18 months. LinkerBot’s 42-degree-of-freedom dexterous hand has shipped over 10,000 units at a production rate of 4,000+ per month, with a reported valuation now above ¥15B (~$2.1B). Government capital (Zhongguancun Fund, Bank of China Asset Management) leads the B+ alongside commercial VCs, a composition that typically tracks procurement contract visibility rather than purely financial valuation.

Linkhou (灵猴机器人)

Series B+, hundreds of millions RMB

CIIF (中网投基金), China’s national industrial investment fund, led Linkhou’s Series B+ at a reported ¥3B (~$415M) valuation. Linkhou makes components for humanoid robots (perception systems, motors, and controllers) sold into multiple OEMs rather than competing at the system level. Silicon Valley R&D office. Revenue reportedly exceeding ¥200M (~$28M) from embodied AI orders. The picks-and-shovels position is defensible regardless of which humanoid OEM wins at scale.

Wujie Power (无界动力)

Angel, hundreds of millions RMB

Over $200M raised cumulatively at angel stage, ¥5B (~$695M) valuation, and a ¥500M (~$69M) overseas deployment contract signed with Envision for humanoid robots on European and Asian production lines. Envision, a clean energy and battery materials company backed by Chinese and Japanese capital, both led the investment and signed the deployment contract simultaneously, the same operator-as-investor structure as RobotEra and SF Express this week.

Calculet (原粒半导体)

Pre-Series A, ¥500M (~$69M)

IDG Capital led a ¥500M (~$69M) Pre-Series A for Calculet at a reported ¥3B valuation. Calculet builds AI processors on a chiplet architecture, modular standardized compute units assembled into custom configurations rather than monolithic designs that require advanced process nodes. Chiplets assembled from production-capable nodes avoid the export control constraints on equipment and advanced processes. Guoxin Science and Technology Innovation Fund (国新科创基金) co-invests alongside IDG and semiconductor-specialist VCs.

SEAHI Robotics (世航智能)

Series A+, undisclosed

Underwater robots for 0-10,000 meter depths. SEAHI‘s proprietary thrusters are rated for 10,000 operational hours versus a 300-400 hour industry standard, a 25-30x differential that is the company’s primary technical moat. GSR Ventures’ Zhu Xiaohu has invested across three consecutive rounds. Founded May 2023 by a team from Harbin Engineering University with operational deep-sea deployment experience. Simultaneous Series A+ and A++ rounds announced March 31, 2026.

Botshare (擎天租)

Pre-Series A, hundreds of millions RMB

A robot-as-a-service rental platform founded December 2025 that completed four rounds in 105 days. At ¥300,000 (~$42K) per humanoid robot, the purchase price is out of reach for most SME buyers; daily rental changes the access model. Charoen Pokphand’s robotics arm reportedly invested, bringing the Thai conglomerate’s manufacturing and food processing operations across Asia into both the investor and likely deployment picture. Reported valuation: ¥4.2B (~$580M).

Cangzhou Four STARS Glass (四星玻璃)

Pre-IPO, ¥300M (~$42M)

A 33-year-old borosilicate glass company closing a Pre-IPO round is the most unusual deal by company age in this week’s cohort. Sixing makes pharmaceutical packaging glass (vials, ampoules, syringes) using the cold-top all-electric Vello process, the same manufacturing approach as SCHOTT in Germany. Sixing is reportedly the only Chinese company operating this process at scale, and fourth globally. China’s healthcare supply chain localization push creates sustained demand for domestic alternatives to imported pharmaceutical packaging that can match the quality standard.

BCDTEK (芯视佳)

Series A, hundreds of millions RMB

Silicon-based OLED microdisplays for AR and VR, the display technology inside the Apple Vision Pro, currently dominated globally by Sony’s OLEDoS process. BCDTEK is constructing China’s first 12-inch silicon OLED fab. The combination of display technology (the bottleneck in high-end AR) and domestic fab capacity (the semiconductor sovereignty angle) makes this relevant to both the AR hardware market and China’s display independence agenda.

破壳机器人 (”Hatching Robot”)

Angel, tens of millions USD

Home service robots, founded by a Tsinghua professor, backed by Yunqi Capital (led), Shunwei Capital (Lei Jun’s fund), and Honghui Fund at a reported ¥2.6B (~$360M) valuation with no products shipped publicly. The valuation rests entirely on founder premium: Tsinghua credentials, high-profile investor names, and a large addressable market in home robotics.

Spirit AI (原力灵机)

Series A+, undisclosed

Spirit AI‘s Spirit v1.5 VLA (Vision-Language-Action) model ranked #1 on RoboChallenge, the global real-world robotics benchmark, outperforming Physical Intelligence’s π0.5. Moz1 humanoid robots are deployed on CATL’s Zhongzhou battery production line. Huaqin Technology (华勤技术), Yufu Holdings (渝富控股, Chongqing state capital), and Hengxu Capital (恒旭资本) led the Series A+. Total raised: approximately ¥3.3B (~$460M) across six rounds in 18 months. The “dirty data” training thesis (building robot intelligence from unstructured real-world data rather than curated clean datasets) is the contrarian technical bet underlying the benchmark performance.

QingNa Technology (青钠科技)

Series A, ¥200M (~$28M)

Sodium-ion batteries for industrial and grid applications. One million large cylindrical cells shipped to European customers in January 2026; five million contracted for the year, making QingNa the first Chinese sodium-ion startup to reach commercial-scale export to Europe.

Huaxi Aviation (华喜航空)

Seed, tens of millions RMB

A hydrogen-turbine hybrid eVTOL: hydrogen fuel cell plus turbine rather than battery-electric. Joby, Archer, Wisk, and Volant are all-electric; Huaxi is pursuing a different energy architecture. Hydrogen-turbine hybrids address the range and energy density limitations that battery-electric designs face at larger scale. Seed valuation is reported at ¥150M (~$21M).

The Bigger Picture

The Customer-Investor Loop

The three strongest robotics deals this week share the same structure: the company writing the largest check is also running the robots.

SF Express led the RobotEra round (detailed in the Spotlight above) and operates the company’s humanoid robots across its own logistics network. Envision led Wujie Power’s raise and signed a ¥500M (~$69M) overseas deployment contract in the same transaction. Botshare’s Pre-Series A brings in capital alongside a rental model that lowers the access barrier for SME buyers priced out of ¥300,000+ direct purchases.

The structure makes commercial sense at this stage of the technology. Humanoid robots are not yet at the cost and reliability level where a neutral financial investor can independently underwrite deployment risk. A major logistics operator, a battery materials manufacturer, or a manufacturing conglomerate has the operational environment, the data collection capacity, and the scale purchasing power to run a real robot program. The equity investment gives them preferred pricing, roadmap access, and upside if the company scales. The deployment contract gives the startup committed purchase volume, the hardest problem in early commercial robotics.

At this stage of the technology, commercial traction is better read from the lead investor’s operational relationship with the product than from valuation or benchmark position alone.

China’s Private Aerospace Week

China’s aerospace and commercial space sector raised ¥26.6B (~$3.81B) across 137 rounds in 2025, a record year. This week added $369M at the top.

Volant’s $300M is the largest round in Chinese passenger eVTOL history. The investor composition matters as much as the size: Futen Capital, backed by Shanghai State-owned Capital Investment Co., entered a crewed eVTOL OEM for the first time. Toyota’s $394M Series C investment in Joby Aviation in January 2020 established that a major industrial operator would commit strategic capital to the category; Futen’s entry serves the same function for Chinese eVTOL. Shanghai has publicly framed its ambition to become the world eVTOL capital, and Futen’s investment is the first direct capital commitment behind that public ambition.

CAAC’s eVTOL certification timeline (31 months versus 5-7 years in Western markets) is a structural advantage the capital markets are pricing in. With 1,900+ aircraft on Volant’s order book and Shanghai municipal state capital committed, the conditions for a national champion designation are visible.

Cosmoleap’s ¥500M (~$69M) Series A, covered by SpaceNews, is the launch side of the same story: a company founded February 2024 has raised approximately $83M in 18 months for a reusable rocket with tower-catch recovery. China’s private launch sector now has multiple companies at significant funding levels, with the gap to SpaceX-tier technology closing on the orbital reuse side.

Quantum Goes Commercial

China’s quantum sector saw investment in Q1 2026 approach full-year 2025 levels. TuringQ’s revenue trajectory (¥500,000 (~$69K) in 2022, ¥10M+ in 2023, ¥100M+ in signed orders in H1 2025) is the first genuine commercial curve to appear in photonic quantum computing. The 2025 World Internet Conference Leading Technology Award going to a quantum computing project for the first time is one signal; the national guidance fund entering directly is another.

The technology path TuringQ pursues, photonic chips operating as co-processors alongside classical systems at room temperature, sidesteps the cryogenic requirements that constrain superconducting quantum computers and puts early commercial applications within reach: financial risk modeling, materials simulation, and combinatorial optimization, problems where the solution space is too large for classical computers to search exhaustively. PsiQuantum, the most-funded photonic quantum company globally, has raised over $2B on the same architectural bet. TuringQ has reached ¥100M+ (~$14M) in customer orders at a fraction of that capital intensity, operating an integrated domestic chip production line.

The entrance of the National Venture Capital Guidance Fund’s Yangtze River Delta Fund into the B+ round is the policy signal that the commercial trajectory has been validated at the highest level. China’s 15th Five-Year Plan places quantum in the same “future industry” designation as semiconductors and AI. At this level of the state capital hierarchy, direct investment has historically preceded national champion designation in sectors from semiconductors to EVs. TuringQ is the first photonic quantum company in China to combine a national guidance fund investment, a ¥7B (~$970M) valuation, and a demonstrated ¥100M+ commercial order book.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete.