The China Round — May 15, 2026

StepFun's $2.5B Pre-IPO, State Capital Leads 30 Deals, and a Biotech Startup Buys a ¥900M Factory

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

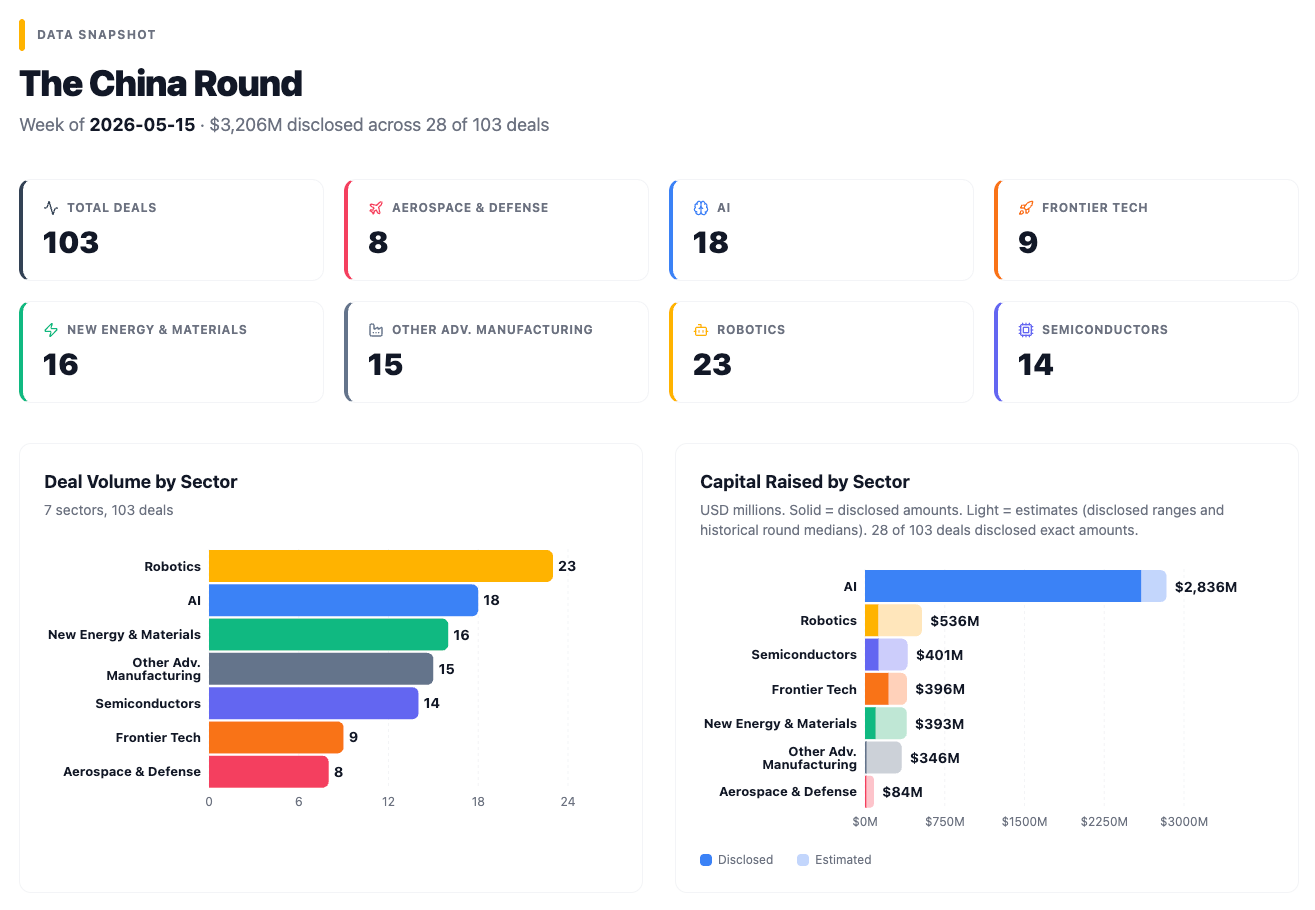

Where the Money Went

Last week’s 46 deals reflected the May Day holiday. This week brought 103 across seven sectors, confirming the Q2 2026 funding cycle is fully underway.

103 deals, 28 with disclosed amounts. Those 28 disclosed a combined $3.2B (~¥23.1B), dominated by StepFun’s ~$2.5B Pre-IPO, which alone accounts for 78%. Strip that out and the remaining 27 deals disclosed ~$706M (~¥5.1B). The true weekly total is higher. Most deals don’t publish amounts, and the disclosed figure understates actual capital deployed.

Stage distribution skews heavily early. Angel and seed rounds make up the majority across every sector, with few Series A or B companies and a handful of mega-rounds at the top. The barbell shape that has characterized China’s deep tech funding all year is intact.

🤖 Robotics (23 deals)

The week’s largest deal count, and the most fragmented. No single round dominates the way StepFun does in AI. Vbot (维他动力) raised the headline ticket at ~¥500M (~$69M) Pre-A for a consumer robot dog, but the 23 deals cover consumer companion robots, industrial embodied AI, construction robots, lawn mowers, kitchen robots, wearable exoskeletons, and component suppliers. Fourteen of the 23 were angel or seed-stage, five Pre-A or A, and four strategic or B+ transactions. One straggler: ZeroErr (零差云控, robot system core components, C+, close to ¥100M, ~$14M).

🧠 AI (18 deals, including 3 stragglers)

StepFun at ~$2.5B Pre-IPO dwarfs everything else in the sector. 奕行智能 (EVAS, RISC-V AI chips) took a strategic investment from China Mobile’s chain fund; Motion Brain (眸深智能) raised ¥300M (~$42M) Pre-A for an embodied AI brain targeting humanoid robots; ComNergy Tech (共绩科技) raised close to ¥100M (~$14M) Pre-A for idle GPU compute aggregation. Three AI stragglers were sub-¥10M angel rounds.

🔬 Semiconductors (14 deals)

SemiDrive headlines with a $100M (~¥720M) Series C. China’s most-deployed automotive SoC maker is now pivoting toward humanoid robots. 象帝先计算 raised hundreds of millions in a Series B as its near-death 2024 story converts to an IPO-prep 2026 story. RiVAI Technology (睿思芯科) closed a B+ for high-end RISC-V server processors. Fermion Technology (费勉仪器) closed a C+ for precision scientific instruments used in semiconductor and quantum research. Five of the 14 deals have disclosed amounts; government-affiliated funds led or co-led at least eight.

⚡ New Energy & Materials (16 deals)

The largest sector by deal count after robotics. Lithium Source (常州锂源) took ¥440M (~$61M) strategic investment for LFP cathode expansion. Xinta Green Energy (信塔绿能) raised ¥100M (~$14M) at angel. Multiple early-stage deals in solid-state batteries, power electronics, carbon nanomaterials, and hydrogen water tech. Greater Bay Technology (巨湾技研), the ultra-fast charging battery maker, took an undisclosed strategic round.

🚀 Aerospace & Defense (8 deals)

Zero last week, eight this week. All angel or early stage, with a combined $14M in disclosed capital. Beijing Hengxing Power (恒星力量) raised ¥100M (~$14M) at angel for space energy research; Cathay Innovation and 厚雪资本 co-led. Shenzhen Zhiyu Aerospace (执宇航天) raised tens of millions (~$7M+) at angel for small reusable launch vehicles. Shenzhen Qingwei Aviation (庆为航空) closed a Pre-A for fly-by-wire avionics and smart cockpit displays. Vision Aero (维新宇航) raised tens of millions (~$7M+) at angel for a 7-seat eVTOL targeting emergency response. Four additional deals covered satellite propulsion, aerospace electrical interconnects, and microwave remote sensing.

⚙️ Other Advanced Manufacturing (15 deals)

公大激光 / Gongda Laser headlines with a Series C, hundreds of millions RMB, for its green fiber laser technology, more on this in Spotlight. Yiktong (亦唐科技) raised hundreds of millions in a B+ for high-speed SMT pick-and-place equipment. KeenCool (云酷智能) raised close to ¥100M (~$14M) for liquid cooling equipment for AI data centers. One straggler: 时耘科技 (intelligent robots, angel).

💡 Frontier Tech (9 deals)

微元合成 / Microcyto leads with ¥1.5B (~$208M), a synbio startup that used the round to acquire a ¥900M+/year traditional factory. 雷鸟创新 / Rayneo, the global #1 AR glasses brand by unit volume, closed a C+ round of over ¥1B (~$139M) in January 2026, captured in this week’s data. Two quantum computing startups, Hangzhou Wuwen Quantum (无问清芯) and GGQuanta (国光量子), and a photonic computing chip startup, PhotonCore (光子芯力), raised angel rounds. Genlight (佳量脑科学) shows a C round at an implied ¥60B (~$8.3B) valuation and has no verifiable public presence.

Spotlight

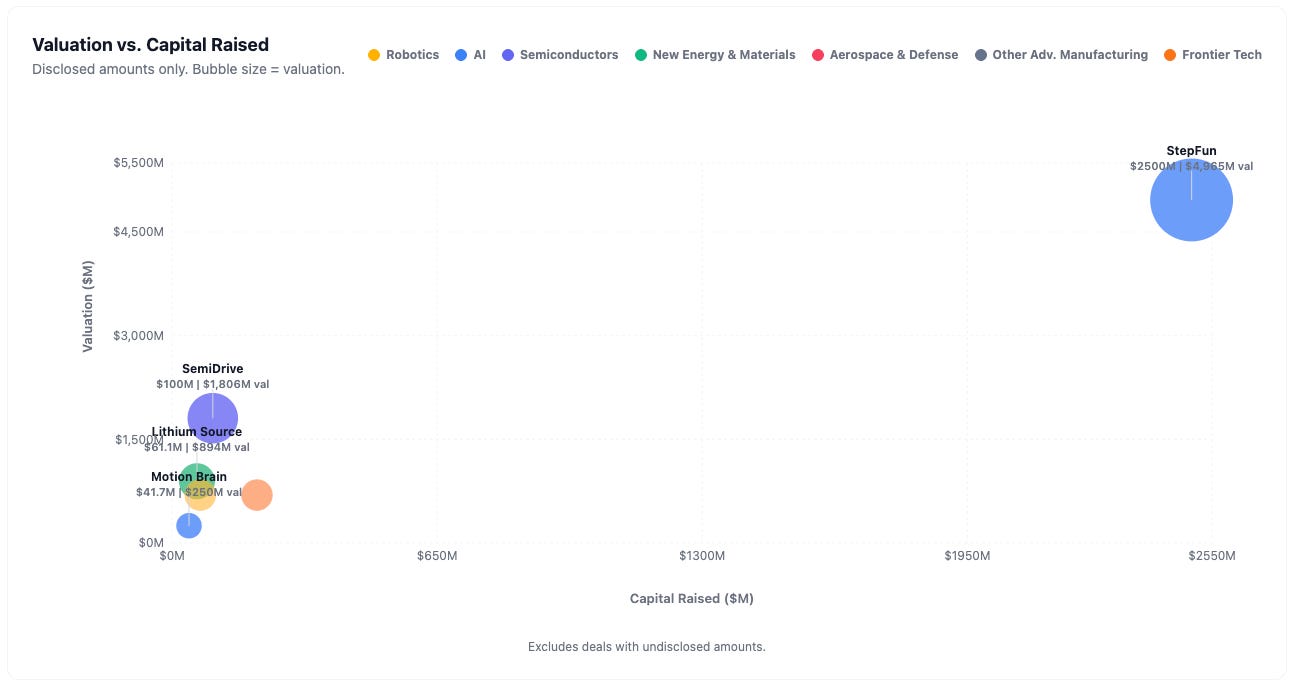

StepFun (阶跃星辰)

Pre-IPO, ~$2.5B (~¥18B), valuation undisclosed

China’s most aggressive LLM fundraiser is heading for Hong Kong, and the companies betting on it build the phones.

StepFun builds large language models, the AI systems behind tools like ChatGPT and DeepSeek, developing everything from the training infrastructure to the final products. Founder Jiang Daxin (姜大昕) spent 16 years at Microsoft Research Asia, the Beijing lab that trained a generation of China’s AI researchers, before leaving in 2023 to start the company. He holds a PhD from SUNY Buffalo and spent a year as an assistant professor at Nanyang Technological University in Singapore before joining Microsoft. His 2008 best application paper at SIGKDD, one of computer science’s top data mining conferences, on query suggestion was one of the earliest works showing that user behavior data could improve search in ways no engineer could manually design. StepFun’s core products include Step-2, a language model with over a trillion parameters (the internal connections that determine what a model knows and how well it reasons), using a mixture-of-experts design that routes each query to the most relevant specialist sub-networks rather than running every parameter on every question, dramatically reducing cost; Step-Video-T2V, a 30-billion-parameter video generation model that was the best-performing in its class at its February 2025 release; and Step-Audio, a 130-billion-parameter model that handles the full speech pipeline from understanding spoken language to generating natural speech. The company publishes its model code freely on developer platforms, letting anyone download and build on them to lock in developer adoption before the IPO.

The Pre-IPO round closed at approximately $2.5B (~¥18B), with a filing target for Hong Kong by end of June and a year-end listing expected. In January 2026, the company raised a ¥5B+ B+ round led by Shanghai State Capital Pioneer Fund (上国投先导基金), with Tencent following on. Yin Qi (印奇), who co-founded facial recognition company Megvii (旷视科技) and navigated it through a multi-year sanctions saga to a Hong Kong listing, became chairman that same month, suggesting StepFun is treating the IPO as its primary near-term mission. Huaqin Technology (华勤技术) and Longcheer Technology (龙旗科技), the contract manufacturers that design and build most of the world’s Android phones for brands like Samsung and Xiaomi, both invested in the Pre-IPO. ZTE, a major Chinese telecom infrastructure company, also joined and has already embedded StepFun models in mass production inside the Nubia Z80 Ultra. All three manufacture or assemble the devices that would distribute StepFun’s models at scale. If StepFun’s AI ends up embedded in hundreds of millions of handsets, these companies want equity exposure before the IPO.

StepFun’s Pre-IPO, with smartphone ODMs as investors, reflects a broader sorting in China’s LLM cohort. Companies that can scale toward public listings are moving to do so, while those that can’t are pivoting to narrower applications or device-level partnerships.

Investors (Pre-IPO): Huaqin Technology (华勤技术), Longcheer Technology (龙旗科技), ZTE (中兴通讯), and others. B+ round (January 2026): Shanghai State Capital Pioneer Fund (上国投先导基金, lead), Tencent.

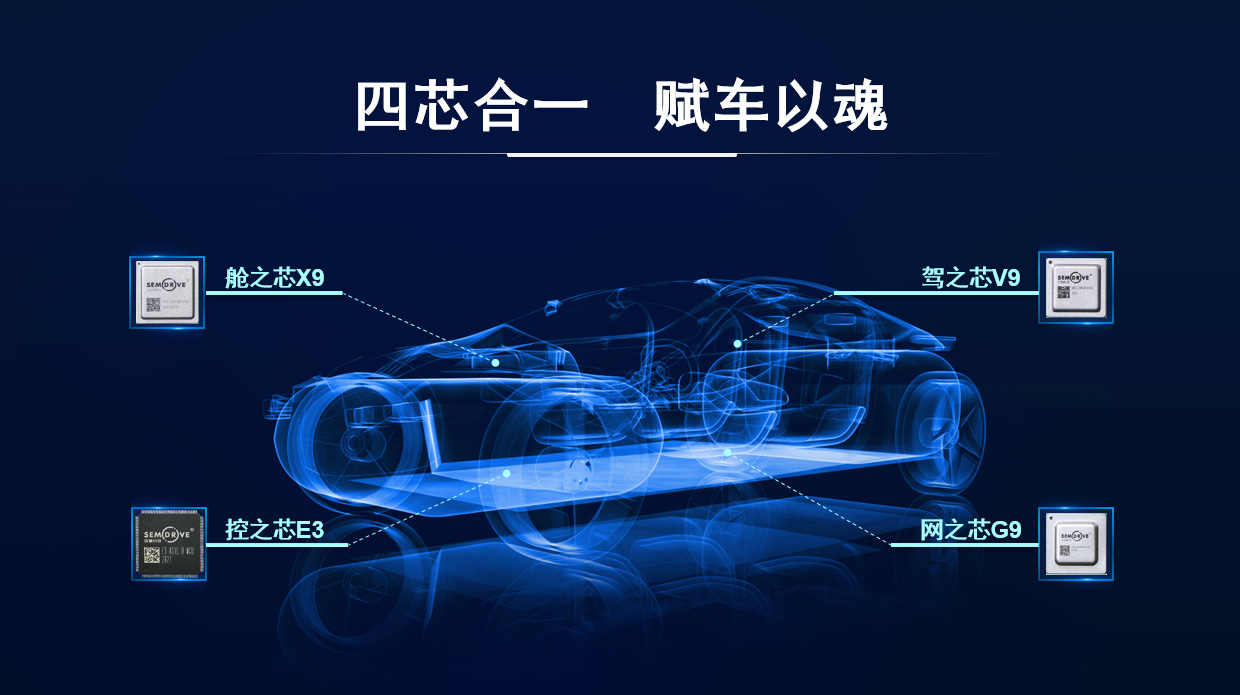

SemiDrive (芯驰科技)

Series C, $100M (~¥720M), ~¥13B (~$1.8B) valuation

China’s most widely deployed automotive chip maker closes its C round and starts talking to humanoid robot OEMs.

SemiDrive makes the chips that run China’s car cabins, gateways, and control systems. Its X9 series handles what the auto industry calls intelligent cockpit: the dashboard screens, voice assistants, and multi-display environments inside modern cars. Its G9 series manages vehicle gateway functions, routing signals between different vehicle subsystems. Its E3 microcontroller handles smart control tasks like power management and sensor coordination. Together, the product family covers the vehicle’s full electrical and electronic architecture, the hardware spine that connects every sensor, screen, and control system in a modern car. The company has shipped 12 million units, built 100+ mass-production vehicle models into its customer base, and holds relationships with over 260 customers, including 90%+ of China’s domestic automakers and a selection of international automakers. It was founded in 2018.

The Series C was led by Suzhou State Investment (苏产投), with Beijing Yizhuang National Investment (亦庄国投), 京国瑞, and three other investors co-investing. Shaanxi Heavy Truck (陕汽集团) subsidiary 陕汽鸿德投资 joined as a new strategic shareholder, a truck maker integrating up the supply chain. The round values the company at approximately ¥13B (~$1.8B). SemiDrive’s D-series chips are now targeting humanoid robot applications. Automotive-grade chips, tested for vibration, temperature extremes, and long-life reliability in ways consumer electronics chips are not, are a natural fit for industrial robots that operate in harsh real-world environments. The company that supplies cockpit silicon to 90%+ of China’s car makers is positioning for the same role in the robot market.

Investors: Suzhou State Investment (苏产投, lead), Yizhuang National Investment (亦庄国投), 京国瑞, Beijing Municipal Advanced Manufacturing Fund (北京市先进制造基金), Xi’an Finance Group (西安财金), 益中亘泰. Financial advisor: 多维资本.

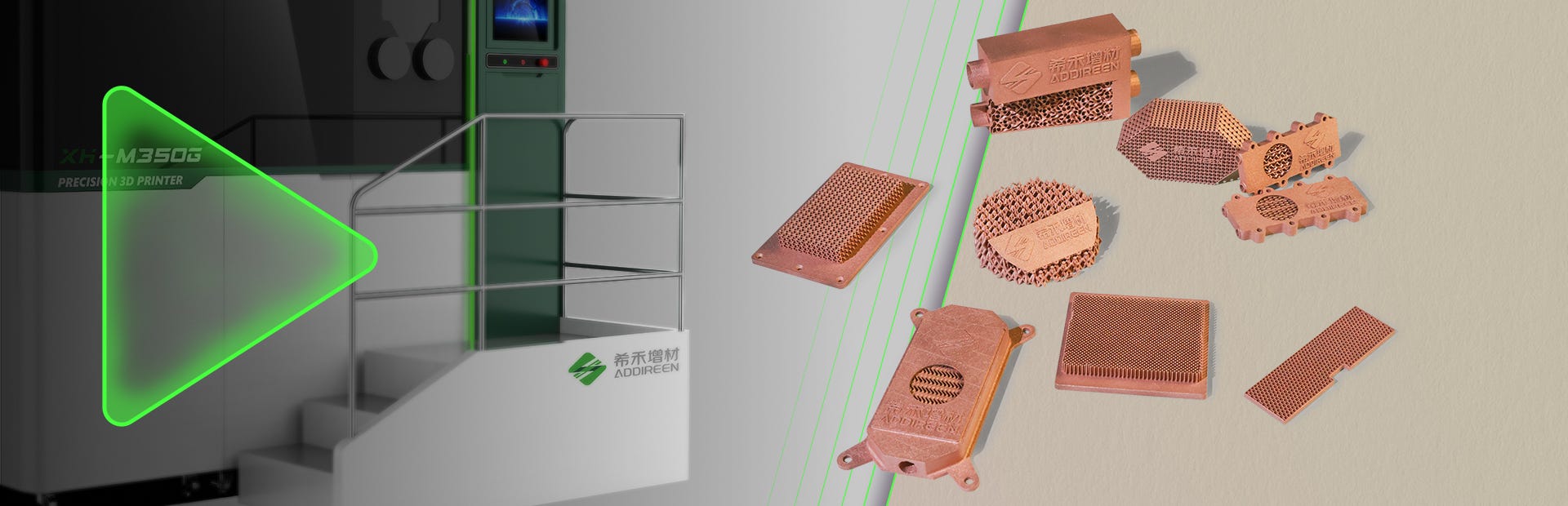

Gongda Laser (公大激光)

Series C, hundreds of millions RMB (~$28M+), ¥1.5B (~$208M) valuation

The company that makes China’s most powerful green fiber lasers just found a second market in the cooling systems inside AI data centers.

Gongda Laser makes short-wavelength fiber lasers, specifically green lasers, which operate at wavelengths that infrared fiber lasers cannot reach. Green light is what you need when you’re welding copper, cutting lithium battery electrodes, or processing silicon in semiconductors, because copper and silicon absorb green wavelengths far more efficiently than infrared. Founded in 2019 by Zhang Fan (张帆), a PhD with 16 years in fiber laser research, the company claims over 80% of the domestic green fiber laser market, a figure repeated in trade press interviews. Per its Series C announcement, it has developed a 4kW continuous green fiber laser, enough power to cut and weld industrial copper at production speed, a level that no known Chinese or Western competitor has reached in this wavelength and form factor. (IPG Photonics, the global fiber laser leader, tops out at around 100W in green; Trumpf offers 3kW at green wavelengths via a disk laser, a different architecture at a different price point.) Revenue exceeded ¥100M in 2023.

Gongda’s sub-company 希禾增材 (Xihe Additive) uses copper-based metal 3D printing to manufacture cooling structures and heat spreaders for AI data center hardware. Copper conducts heat better than aluminum, but it’s harder to process, which is where a high-power green laser becomes essential.

The company has deployed over 100 copper 3D printing units commercially. 禾创致远, affiliated with Zhongji Innolight (中际旭创), Nvidia’s primary manufacturer of optical transceivers, the components that handle high-speed data transmission between servers in AI data centers, invested alongside 华胥基金 (affiliated with Sany Heavy Industry / 三一重工). Dazheng Capital (达晨财智) and Photosynthesis Ventures (光合创投) co-led.

Investors: Dazheng Capital (达晨财智, co-lead), Photosynthesis Ventures (光合创投, co-lead), 禾创致远 (Zhongji Innolight / 中际旭创 affiliated), 华胥基金 (三一集团 affiliated), 力合科创. Huachuang Capital (华创资本) continued from prior rounds.

Microcyto (微元合成)

New financing round, ¥1.5B (~$208M), valuation undisclosed

A synthetic biology startup used its ¥1.5B financing round to acquire a sugar alcohol factory generating nearly ¥1B in annual revenue.

Microcyto uses microbial fermentation to manufacture bio-based compounds, essentially programming microorganisms to act as chemical factories, producing sugar alcohols, natural pigments, and functional ingredients from biological feedstocks rather than petroleum or chemical synthesis. Founded in December 2021 by Dr. Liu Bo, who did his doctorate at the CAS Institute of Microbiology, the company has developed a one-step fermentation pathway to allulose, a rare sugar with minimal calories, that China’s National Health Commission approved for commercial sale in 2025, making it the first company in China with regulatory clearance for this production method. Its fermentation process for mannitol, a sugar alcohol widely used in food and pharmaceuticals, converts 99% of the raw input material into product at 99.9% purity.

Part of the ¥1.5B (~$208M) financing is long-term bank debt from Xingye Bank’s (兴业银行) Beijing branch. Banks size credit facilities against physical assets and revenue, so the loan itself is a form of due diligence on the factory being acquired. The money is buying Yusweet (豫鑫糖醇), an Anyang, Henan manufacturer of xylitol, erythritol, and related sugar alcohols operating since 1996 that generated approximately ¥919M in revenue in 2024. Per the company’s announcement, Yusweet is among the world’s leading xylitol producers. Yusweet chairman Zhang Qibin (张其宾) co-invested in Microcyto as part of the deal, becoming a shareholder in the company buying his factory and aligning incentives across the transition.

Synthetic biology companies in China have historically either built new factories from scratch or partnered with contract manufacturers for pilot batches. Microcyto is acquiring an existing industrial asset and upgrading it with bio-manufacturing technology. The factory provides immediate scale; the technology provides margin improvement and the ability to expand into new products that chemical synthesis cannot access.

Investors: Zhang Qibin (张其宾, Yusweet chairman), Xingyin Investment (兴银投资, Xingye Bank’s ¥100B AUM investment subsidiary), Tan Ruiqing (谭瑞清, former Longbai Group vice chairman, 30+ years in chemical manufacturing).

Vbot (维他动力)

Pre-A, ~¥500M (~$69M), valuation undisclosed

The ex-Horizon Robotics team that built autonomous driving chips for cars is now shipping autonomous robot dogs to consumers, having just raised the largest single ticket in Chinese consumer robotics history.

Vbot makes consumer robot dogs. The founding team assembled three of the people who built Horizon Robotics, the company that supplies AI chips to Chinese automakers: CEO Yu Yinan (余轶南) was Horizon’s VP and a founding member since 2015; CTO Song Wei (宋巍) was chief architect of Horizon’s software platform; co-founder Zhao Zhelun (赵哲伦) was head of intelligent driving products at Li Auto. The trio left and applied autonomous driving engineering discipline to a product for the home. The Vbot大头BoBo, their first product, runs 128 trillion operations per second of onboard computing power, a level normally found in self-driving car systems rather than consumer gadgets, and does not require a remote control, using vision and AI to navigate independently.

The company was founded in late 2024 and is already shipping. The first 500 units came off the production line and into customers’ hands on May 8th. May’s target is 1,500 total; June’s production target is 2,500+ units per month. The Pre-A of close to ¥500M (~$69M) is, per the company and multiple Chinese tech publications, the largest single financing ticket raised by any consumer robotics company in China. The round had eleven institutional investors, including investors who were present at the seed round continuing with conviction. Xinhua, China’s state news agency, published an editorial this week titled “Capital Accelerates Into Embodied AI, Delivery Capability Becomes Valuation Anchor” (资本加速涌入具身智能,交付能力成估值锚点), with Vbot’s round and shipping timeline as a central example.

The company is separately building a full-size humanoid robot, led by newly hired VP Qin Hailong. The software and hardware architecture overlaps significantly with the robot dog, and the AI stack is designed for reuse across form factors. Deployment data from the robot dog fleet feeds directly into humanoid development. More units in the field means more real-world situations to learn from, the same compounding data advantage that powers Tesla’s self-driving improvements.

Context on the market: Unitree (宇树科技), the domestic leader in quadruped robots, shipped approximately 23,700 units in 2024, representing roughly 69.75% of the global market by unit volume, per GGII, a Chinese robotics industry research firm. Vbot is entering a market that Unitree currently dominates, at a consumer price point (sub-¥10,000, or under $1,400) designed to expand the category rather than compete directly for Unitree’s existing industrial and research customers.

Investors: Dongfang Jiafu (东方嘉富, lead), Huatai Zijin (华泰紫金, lead), Fosun Ruizheng (复星锐正), SAIC-affiliated Shangqi Capital (尚颀资本), 明荟致远. Continuing from prior rounds: Hillhouse Creative Ventures (高瓴创投), Cathay Innovation (凯辉基金), Today Capital (今日资本), BV Baidu Ventures (百度风投), Corsair Capital (渶策资本), 柏睿资本. Financial advisor: Kaihui Capital (高鹄资本).

Also on the Radar

Rayneo (雷鸟创新) — C+, >¥1B (~$139M+), ¥8B (~$1.1B) valuation. Augmented reality glasses that overlay digital information onto the wearer’s real-world view. Global #1 by unit volume (per Counterpoint Research 2025: ~32% global market share, 3.8x overseas sales growth in 2025, Time Magazine Best Inventions 2025 Special Mention). China Mobile (中国移动链长基金) and China Unicom (中国联通联创创新基金) co-invested, the first time two state telecoms have jointly backed the same smart glasses company.

EVAS / 奕行智能 — Strategic, hundreds of millions RMB (~$28M+), ¥10B (~$1.4B) valuation. AI chips built on RISC-V, an open-source chip architecture that frees Chinese chipmakers from US licensing dependencies. Epoch series in mass production since January 2026. China Mobile’s industry chain fund, which invests in companies building out its supply chain, made the strategic investment this week, following a Series B led by four Beijing government AI funds earlier in 2026.

Ola Dimensions (欧拉万象) — Angel, hundreds of millions RMB (~$28M+), ¥1B (~$139M) valuation. Founded March 2026. Two rounds in 60 days. Sole founder Zhou Shunbo: former Huawei “genius recruit” (华为天才少年), company-level chief expert in robotics, first Chinese recipient of a best paper honor from IEEE, the world’s largest engineering professional society, in robotics and automation. A deliberate counter-thesis to the perfectionism in consumer robotics: ship an imperfect version one, collect real-world data, iterate rapidly. Two rounds backed by China Merchants Group Ventures (招商局创投) and SAIF Partners (赛富投资基金), among others.

Lumos Robotics (鹿明机器人) — A1+A2 (announced together), hundreds of millions RMB (~$28M+), ~¥3B valuation. Mitsubishi Electric China led both consecutive rounds. The company’s FastUMI Pro, a tool that captures the movement data robots need to learn tasks, cuts training data collection time by 5x and cost by 80% according to the company, and is claimed to be in use by two-thirds of global robotics AI research labs. A Japanese industrial giant securing access to Chinese robotics AI training tools through back-to-back equity stakes.

XDXCT / 象帝先计算 — Series B, hundreds of millions RMB (~$28M+), ¥9B (~$1.25B) valuation. A domestic maker of high-performance GPUs, the processors that train and run AI models. Near-death in 2024: accounts frozen in August, hundreds of employees laid off, an investor protection clause triggered that penalizes the company for missing performance targets. Rescued by a new investor (Anfu Technology) in February 2025. Now: stock restructuring planned for H2 2026, IPO advisor signed. The 40% valuation haircut from peak was the price of survival.

Fangshi Robot (方石机器人) — Series A, close to ¥100M (~$14M), ¥500M (~$69M) valuation. Construction robots: spray-coating, floor tile laying, ground leveling. Seven years old. 500+ projects completed, 15M+ square meters covered. Deployed in 10+ countries across the Middle East, Southeast Asia, and East Asia. Fortune 500 construction companies as customers. Only now taking its first institutional round.

Picocom (比科奇微电子) — C+, ¥100M (~$14M), ¥500M (~$69M) valuation. Chips that handle the core signal processing in 5G cell towers, built for open radio access networks, an architecture that lets mobile operators mix equipment from different vendors instead of buying locked-in systems from a single supplier. President Peter Claydon’s prior company Picochip dominated the market for small cell base stations, the compact antennas that extend mobile coverage inside buildings and dense urban areas, holding approximately 70% global market share before its $75M acquisition. Beijing and Bristol R&D centers. Now expanding into broadband terminals for low-earth orbit satellite networks like Starlink and China’s equivalent constellations.

Changyao Innovation (长曜创新) — A+, tens of millions RMB (~$7M+), ¥150M (~$21M) valuation. Lawn mower robots that navigate without buried boundary wires, using six cameras and a depth sensor. Its AIRSEEKERS TRON raised $2.2M from approximately 1,400 backers on Kickstarter in 30 days. US and Europe offices established. Midea-system investor Yingfeng Environment (盈峰环境) led this round. Born on Kickstarter, sold to Western buyers before any domestic launch narrative.

Greater Bay Technology / GBT (巨湾技研) — Strategic, undisclosed, ¥15B (~$2.1B) valuation. Batteries that can fully charge in 5-15 minutes while storing enough energy per kilogram to power a full-size passenger car, not just a scooter. Production customers span GAC’s passenger lineup (Aion, Trumpchi, Hycan), commercial truck makers including Shaanxi Auto and FAW Jiefang, and EHang’s electric vertical-takeoff aircraft. Five-region manufacturing strategy underway.

Motion Brain (眸深智能) — Pre-A, ¥300M (~$42M), ¥1.8B (~$250M) valuation. AI software that gives humanoid robots the ability to generate fluid movements, understand the 3D space around them, and run complex AI models directly on the robot’s own hardware rather than relying on cloud servers. Founded by Professor Chen Tao of Fudan University’s Deep Learning Lab and Zhang Yimin, former Chief Scientist at Intel China.

Stragglers

One straggler cleared the notable bar: ZeroErr (零差云控) (robot system core components, C+, close to ¥100M, ~$14M, backed by 华控基金, 同创伟业, and 国泰海通), a component supplier positioning for the robot supply chain buildout.

The Bigger Picture

State Capital Is the Lead Investor in China’s Hardware Sovereignty Push

Government guidance funds, the state-backed investment vehicles China uses to direct capital into strategic industries, usually appear in venture deals as co-investors alongside private firms, filling gaps rather than setting terms. This week, state capital led or co-led at least 30 of the 103 transactions. In semiconductors and aerospace specifically, government funds were the named lead investor in nearly every deal with a disclosed lead.

SemiDrive’s Series C was led by Suzhou State Investment (苏产投). EVAS (RISC-V AI chips) was led, in its prior B round, by four Beijing government AI funds simultaneously, with China Mobile’s chain fund adding a strategic this week. Fangshi Robot’s Series A included AECC Aviation Fund (航发基金), the investment arm of China’s state aero-engine corporation, and Beijing Science & Technology Innovation Fund (北京科创基金). Of the eight aerospace deals this week, most involved government-affiliated funds as leads or sole investors.

In December 2025, Beijing announced a national venture capital guidance fund seeded with ¥100B (~$14B) in central government capital, structured to mobilize ¥1T (~$138B) over 20 years through 600+ sub-funds targeting integrated circuits, quantum technology, aerospace, and biomedicine with a mandate to put at least 70% into seed and early-stage companies, per the NDRC launch announcement and reported by Caixin. Five months later, this week’s deals are early evidence of that system deploying.

The broader system has been building for a decade. China’s government guidance fund network now comprises over 2,000 funds with a confirmed total of more than $500B raised. State capital now provides the majority of the money backing China’s venture and private equity funds. In effect, the government is the biggest investor in the investors. The semiconductor-specific vehicle, the “Big Fund” (国家集成电路产业投资基金), has escalated in each phase: ¥98.7B in 2014, ¥204B in 2019, ¥344B (~$47.5B) in its third phase launched May 2024, now fully operational with Phase III focused specifically on equipment and materials, the parts of the chip supply chain most vulnerable to US export controls.

SemiDrive is the domestic alternative to NXP and Renesas in automotive chips. EVAS is building AI chips on an open architecture that no US company can sanction. Fangshi Robot deploys into construction sites across the Middle East and Southeast Asia. In each case, government capital is backing companies that reduce Chinese dependence on foreign suppliers.

China’s Big Model Endgame: The Device-Embedded AI Race

The framing that has dominated analysis of China’s large language model startups, often called the “six small tigers” (六小虎), is no longer useful. It describes a 2024 world that has already reorganized.

The company raised approximately $2.5B (~¥18B) at a valuation targeting around $10B for its Hong Kong IPO, expected before year-end. Huaqin Technology and Longcheer Technology, the two largest contract manufacturers of Android smartphones globally, joined the Pre-IPO round. ZTE, which builds China’s domestic telecom infrastructure, also invested and has already embedded StepFun models in mass production inside the Nubia Z80 Ultra.

The chatbot and API subscription model that defines Western LLM revenue is a difficult path in China. The domestic market for consumer AI subscriptions is competitive and price-sensitive. The more durable model, and the one that smartphone manufacturers are betting on, is embedding AI at the device level, where models run directly on the phone’s own processor and manufacturers pay for licensing or co-development rather than end-users paying per query. Frost & Sullivan estimates the global on-device AI market at ¥1.2T (~$167B) by 2029, growing at 39.6% per year. Vivo, which shipped 103.9 million phones in 2025 per IDC, has already built a 3-billion-parameter AI model running directly on the phone’s own processor into its device lineup; ByteDance’s Doubao AI assistant runs as part of the phone’s operating system rather than as a standalone app, making it available across everything the user does on the device.

The smartphone manufacturers investing in StepFun’s Pre-IPO make the devices that would embed its models at scale. Equity exposure before a successful IPO is cheaper than negotiating licensing terms after one.

The cohort, as it now stands: Zhipu AI listed in Hong Kong in January 2026. MiniMax is IPO-bound. StepFun is filing by end of June. Kimi raised $2B at a $20B valuation last week. Baichuan AI has pivoted to medical AI. 01.AI has contracted its pre-training team. Benchmark leaderboard competition has given way to a race for device distribution and manufacturer licensing.

Synthetic Biology’s Industrial Graduation

Synthetic biology has spent a decade in China promising to replace petroleum chemistry with biological manufacturing. Most of that promise has lived in pilot plants, research institutes, and funding decks. The Microcyto deal this week suggests the sector may be crossing that gap, through acquisition of existing industrial infrastructure.

The ¥1.5B (~$208M) financing includes long-term bank debt from Xingye Bank’s Beijing branch. Banks size credit facilities against physical assets and revenue. For the loan to clear, the fermentation tanks, processing lines, and distribution relationships of 豫鑫糖醇 had to stand as collateral.

Yusweet (豫鑫糖醇) has been producing xylitol and related sugar alcohols in Anyang, Henan since 1996, with nearly ¥1B in annual revenue. Microcyto brings fermentation-process manufacturing at higher efficiency and purity than chemical synthesis, with the ability to expand into new products (allulose, rare sugars, functional ingredients) that traditional manufacturers cannot produce. Its one-step fermentation route to allulose received National Health Commission regulatory approval in 2025, the first in China. Yusweet chairman Zhang Qibin co-invested in Microcyto, taking equity upside from the technology transformation of his own company.

China’s biomanufacturing sector produces over 70% of global bio-fermentation output and generates approximately ¥1.1T (~$153B) in annual market value, growing at 30% per year since 2015. China’s 15th Five-Year Plan, the government’s top-level economic blueprint for 2026-2030, designates biomanufacturing as one of seven “future industry” priority tracks, the same tier as quantum technology and brain-computer interfaces. The government has funded 43 pilot plant projects nationwide and issued dedicated support programs in 20+ provinces.

For decades, legacy industrial companies acquired synthetic biology startups for technology access. Microcyto reversed the direction, buying the factory and bringing the biology to upgrade it.

Further context from Xinhua on China’s biomanufacturing industrial strategy, February 2026.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.