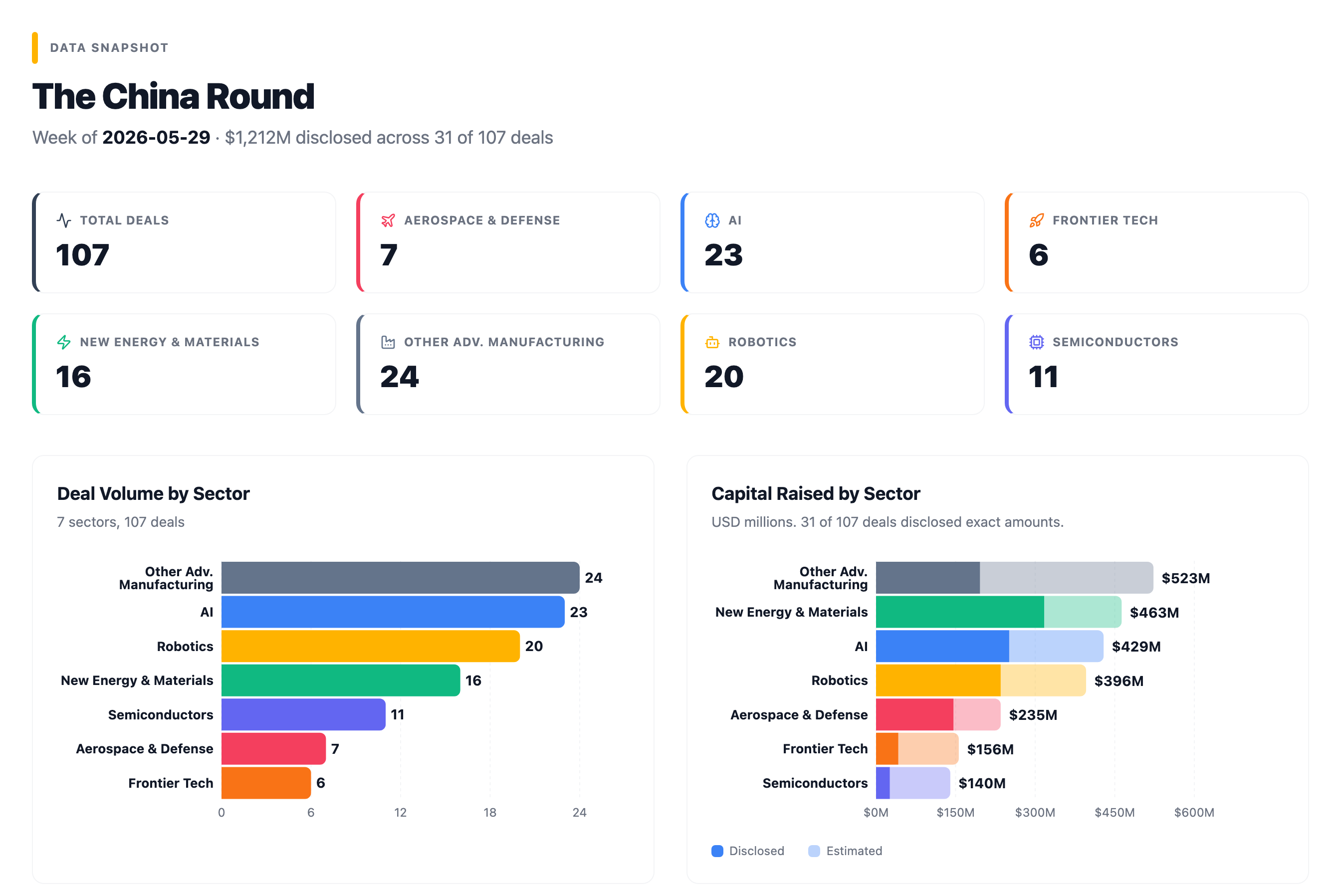

The China Round — May 29, 2026

Money chasing reactors, fusion, and cheaper chips while a battery maker raises at a discount

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

Two moods showed up in the same week. Investors poured early money into nuclear fusion and small modular reactors, frontier energy bets priced at valuations that assume a decade of patience, while one of China’s mid-tier battery makers raised a down round at a third below its prior valuation. Long-patience bets at the frontier, a squeeze in the commodity middle.

Where the Money Went

107 deals crossed the wire this week. Of those, 31 disclosed a dollar figure, for a combined total of roughly $1.21 billion (~¥8.7 billion). Treat that as a floor, not a ceiling: most Chinese rounds, especially the early ones, never publish an amount, so the real number is well above what the disclosed deals add up to.

🧠 AI (23 deals)

The busiest sector by deal count, and the one where chips, not models, drew the money. Several rounds converged on one idea: make AI computing cheaper by routing around Nvidia rather than trying to match it head-on. Sparse-computing chipmaker Moffett AI took ¥1 billion (~$139M); its chips skip the math the network does not need, since most of the numbers flowing through a neural network are zeros that contribute nothing, so the chip does more useful work per watt. A cluster of smaller chip startups raised on the same cost-per-answer logic. Disclosed AI capital came to about $251M (~¥1.8B).

⚡ New Energy & Materials (16 deals)

The week’s largest disclosed pool, about $317M (~¥2.3B), spread across battery materials, solid-state electrolytes, and specialty materials. The standout was a markdown rather than a milestone (see Spotlight), but capital also kept flowing toward the next battery chemistry rather than today’s.

🔬 Semiconductors (11 deals)

Mostly early and mostly cheap, around $26M (~¥187M) disclosed, but strategically dense: memory-maker-backed inference chips, compute-in-memory designs (chips that compute where data is stored, avoiding the memory-to-processor shuttling that is one of the largest energy costs in AI hardware), and chip-making equipment. Listed component suppliers showed up as investors, buying a window into the startups building around them.

🤖 Robotics (20 deals)

Money concentrated in components, not finished robots. Force sensors, robot hands, the interchangeable tools a robot arm swaps at its wrist, and the data used to train machines all drew more capital than any finished humanoid. The largest disclosed robotics round, ¥1 billion (~$139M), went to a force-control arm maker rather than a humanoid brand. Disclosed robotics capital was about $235M (~¥1.7B).

💡 Frontier Tech (6 deals)

Small in count, outsized in ambition: two nuclear-fusion startups, a small modular reactor designer, a neutral-atom quantum company (one of the leading approaches to a practical quantum computer, trapping individual atoms with laser beams as the basic units of calculation), and a brain-spine implant maker. Pre-revenue, pre-prototype, and priced like proven leaders. Disclosed capital was only about $42M (~¥300M), but here the headline figures are the valuations, not the cash in.

🚀 Aerospace & Defense (7 deals)

Electric air taxis and satellite laser-communication startups led here, about $146M (~¥1.05B) disclosed. The biggest was a ¥1 billion (~$139M) round for a maker of passenger electric aircraft that take off vertically like a helicopter but run on battery motors.

⚙️ Other Adv. Manufacturing (24 deals)

The catch-all sector and the second busiest, about $196M (~¥1.4B) disclosed: industrial lasers, 3D printing, optical and inspection equipment, and consumer hardware. A ¥900 million (~$125M) raise for an industrial-laser business was the largest.

Spotlight

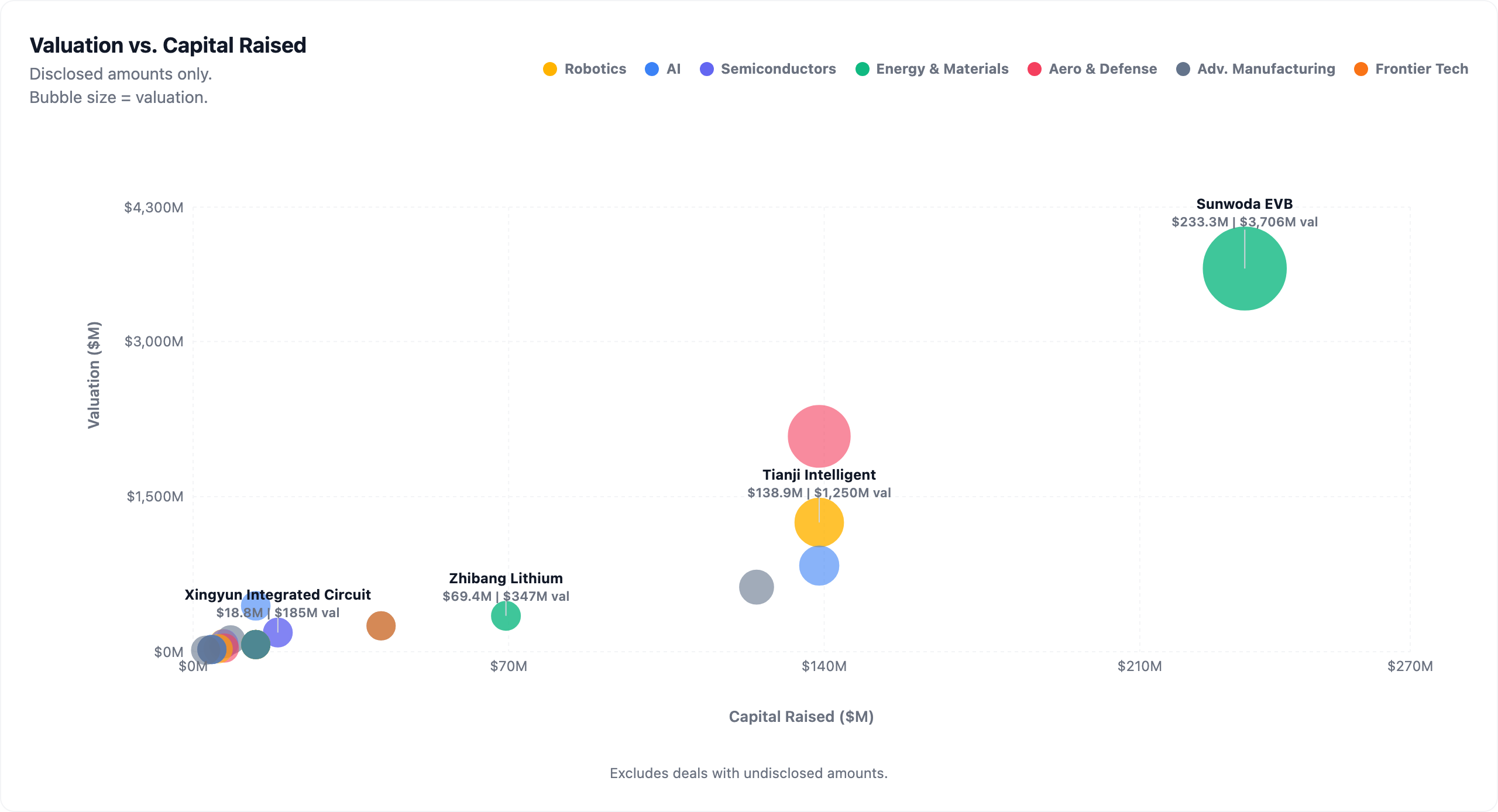

Sunwoda EVB (欣旺达动力)

Series C, ¥1.68 billion (~$233M), ¥25 billion (~$3.5B) pre-money valuation

The power-battery arm of a listed cell maker, raising at a steep discount.

Sunwoda EVB is the electric-vehicle battery subsidiary of Shenzhen-listed Sunwoda Electronic, and one of China’s larger EV-battery makers, ranked sixth domestically by installed volume in 2025. This week it raised ¥1.68 billion from 13 investors at a pre-money valuation of ¥25 billion. The prior round valued the business at roughly ¥36.4 billion, so this round prices it about 31% lower.

The decline maps the broader battery correction. China makes far more battery capacity than its cars and grid can absorb, and a multi-year price war has crushed margins for everyone outside the two giants, CATL and BYD, which together still hold about two-thirds of the domestic market. Sunwoda EVB ran up roughly ¥8.8 billion (~$1.2B) in cumulative losses across 2021 to 2025, and turned its first quarterly profit, a thin ¥13 million (~$1.8M), only in the first quarter of 2026. The investor rotation matters as much as the valuation cut: the round is led by the investment arms of state banks (ICBC, ABC, and China Post), while the carmaker investors from its 2022 round, NIO, Xpeng, Li Auto, SAIC, and GAC, do not appear among the new backers. State capital stepping in where strategic carmakers stepped out is the shape of a sector correction on a single cap table.

Investors: ICBC Capital (工银资本), ABC International (农银投资), and China Post and Shenzhen state vehicles, among 13 total.

Zhibang Lithium (智邦锂电)

Strategic round (de-facto Series A), ¥500 million (~$69M), ¥2.5 billion (~$347M) valuation

A two-year-old solid-state battery materials startup, and a billionaire’s first hard-tech battery bet.

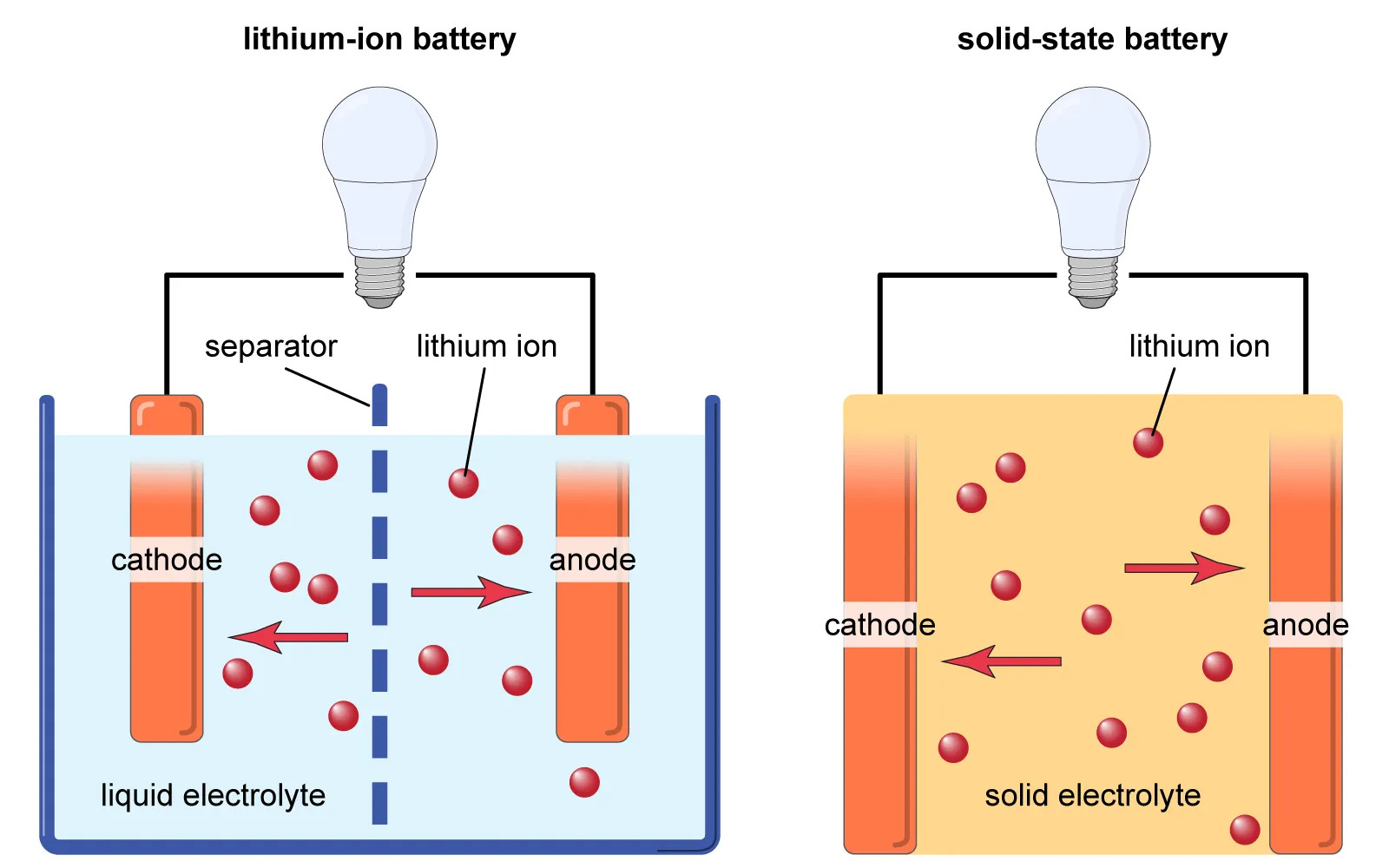

Zhibang Lithium, founded in Quzhou, Zhejiang in March 2024, makes solid-state electrolytes, the component that replaces the flammable liquid inside a normal lithium battery with a solid one, which is the central unlock for safer, denser next-generation batteries. It works across all three competing chemistries (oxide, polymer, and sulfide). It raised ¥500 million at a ¥2.5 billion valuation. The money comes through a fund whose largest backer, at about 82%, is Yangshengtang, the holding company of Zhong Shanshan, the bottled-water billionaire behind Nongfu Spring.

This is Yangshengtang’s first bet on a hard-tech battery-materials company, and it arrives while commodity cell makers like Sunwoda EVB raise at markdowns: capital with no battery history is chasing the chemistry that comes next. The technical anchor is the team. The company’s chief technologist, Xu Xiaoxiong, was chief scientist for solid-state battery research at Ganfeng Lithium, one of the world’s largest lithium players, where he built the program from 2017. With solid-state still years from mass production, this is a wager on where the battery industry goes next.

Investors: Kunshan Gewuzhizhi Fund (昆山格物致知, Yangshengtang-backed), with Quzhou state capital and Xianfeng Changqing (险峰长青).

Xingyun Integrated Circuit (行云集成电路)

Pre-A rounds, over ¥400 million (~$56M) cumulative, latest tranche led by Biwin

A Beijing chip startup trying to make AI answers cheap by dropping the most expensive memory.

Xingyun, founded in Beijing in 2023, designs chips for AI inference, the act of running a trained model to answer a query, as opposed to the far heavier work of training it in the first place. Its pitch is a cost end-run. High-end AI chips like Nvidia’s rely on high-bandwidth memory (HBM), fast, costly memory stacked right on top of the processor to feed it data quickly enough to keep it busy, and US export controls now largely deny China access to it. Xingyun instead builds around commodity memory, the cheaper LPDDR and NAND chips found in phones and storage drives. Those chips are slower, but inference draws on memory in shorter, more predictable bursts than training does, so the company claims the trade buys a memory-cost reduction of one to two orders of magnitude. Its all-in-one inference box, called Brown Ant (褐蚁), already runs open models like Alibaba’s Qwen3. This week listed memory-maker Biwin (佰维存储) extended its backing, bringing Xingyun’s Pre-A funding to over ¥400 million.

Ji Yu (季宇), the founder, came out of Huawei’s “Genius Youth” recruitment program, holds a Tsinghua doctorate, and worked on the compiler and architecture for Huawei’s Ascend AI chips, the most developed homegrown alternative to Nvidia’s chip-and-software stack. Biwin’s continued backing shows a listed memory company building around the thesis that cheap Chinese AI compute will run on the memory it already sells, not the HBM it cannot buy.

Investors: Biwin (佰维存储); earlier Pre-A tranches led by 5Y Capital (五源资本), SAIF Partners (赛富投资), and Primavera Capital (春华资本).

Lightwheel (光轮智能)

Latest round (labeled Series A+), hundreds of millions of RMB, led by Ant Group

The simulation-data supplier behind some of the world’s best-known robots.

Lightwheel, based in Beijing, builds synthetic training data for robots and self-driving systems: photorealistic virtual worlds where a robot can practice picking up a cup or folding a towel millions of times before it touches the real object, far faster and cheaper than physical trials. This week it raised a new round, reported in the hundreds of millions of RMB and led by Ant Group, with China Renaissance (华兴资本) as financial adviser. The company reached unicorn status (a valuation above $1 billion) in an earlier round this spring; this round’s valuation was not disclosed.

Synthetic training data is infrastructure robot builders need regardless of which hardware wins, provided training in simulation transfers reliably to real machines, and Lightwheel’s customer list suggests the industry has made that bet. It is global and blue-chip: Nvidia names it a partner and connects it to GR00T, Nvidia’s general-purpose robot-brain model, software pre-trained to handle a wide range of physical tasks that robot builders adapt rather than build from scratch, and Lightwheel’s simulated worlds are part of what GR00T trains inside. Nvidia also lists Google DeepMind and Figure among Lightwheel’s users, and the company reports over ¥100 million (~$14M) in revenue and, per its own announcement, around $100 million in first-quarter orders. CEO Xie Chen (谢晨) previously ran autonomous-driving simulation at Nvidia, directed simulation at Cruise, and led it at NIO. Lightwheel is one of the few Chinese startups selling this layer to Western robot leaders, not only Chinese ones.

Investors: Ant Group (蚂蚁集团, lead), CCB Investment (建投投资); China Renaissance (华兴资本) as financial adviser. Reported customers beyond those Nvidia confirms (1X, Toyota Research Institute, Bosch) are company-stated.

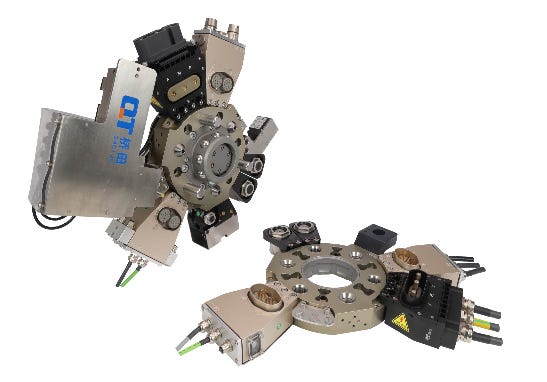

Qiaotian Intelligent (桥田智能)

Series A+ (second A+), around ¥100 million (~$14M), led exclusively by the National Machine Tool Fund

Not a humanoid, the quick-change tooling that robot factories run on.

Qiaotian, founded in Shanghai in 2016, makes robot end-effectors and the hardware around them: the quick-change “wrists” that let a robot arm swap tools in seconds, magnetic die-change systems, grippers, and industrial connectors. It is unglamorous, essential plumbing for any automated production line. This week it raised around ¥100 million in its second Series A+ round, and the investor is the whole point. The National Machine Tool Industry Investment Fund (国家工业母机产业投资基金), a roughly ¥150 billion state fund created to reduce China’s dependence on foreign precision-manufacturing equipment, took the round on its own.

A national fund whose mandate is the machine tools that make everything else, writing an exclusive check into an end-effector maker, treats quick-change tooling as strategic industrial infrastructure, and it fits the week’s broader pattern of state vehicles leading in hard tech. The company says its core business grew 30 to 40% year over year in early 2026, with customers including Geely; the business is profitable, low-profile, and now state-anointed.

Investors: National Machine Tool Industry Investment Fund (国家工业母机产业投资基金, exclusive).

Junhe Atomic (钧合原子)

Angel round, hundreds of millions of RMB, ~¥2 billion (~$280M) valuation

A startup designing small nuclear reactors, founded by the man who sold China’s flagship reactor abroad.

Junhe Atomic, based in Shanghai, designs small modular reactors (SMRs): compact, factory-built nuclear reactors meant to be cheaper and faster to deploy than the giant gigawatt plants, and increasingly pitched worldwide as a clean answer to the electricity demand of AI data centers. The company raised an angel round of hundreds of millions of RMB from more than a dozen investors, with funds earmarked for the conceptual design of its first reactor and team building. The roughly ¥2 billion valuation comes from investor databases and is not confirmed in the announcement; treat it as an early indication on a concept-stage company, not a verified figure.

The founder is why this round attracted more than a dozen investors. Tian Jiashu (田佳树) spent 30-plus years in China’s nuclear industry, served as a deputy chief engineer at both of the country’s nuclear giants, CNNC and CGN, and ran Hualong International Nuclear Power, the joint venture created to sell China’s flagship Hualong One reactor abroad. SMRs are where Western startups like Oklo and X-energy have drawn heavy investor and government backing; China’s are mostly state-run, which makes a privately funded SMR designer with this pedigree rare. A near-term catalyst sits in the background: the state-built Linglong One, the world’s first commercial land-based SMR, is targeting commissioning in 2026, which would de-risk the regulatory path for private players too.

Investors: Lingang Sci-Tech (临港科创), Eastern Bell Capital (东方富海), and Cohesion Capital (聚合资本), among more than a dozen.

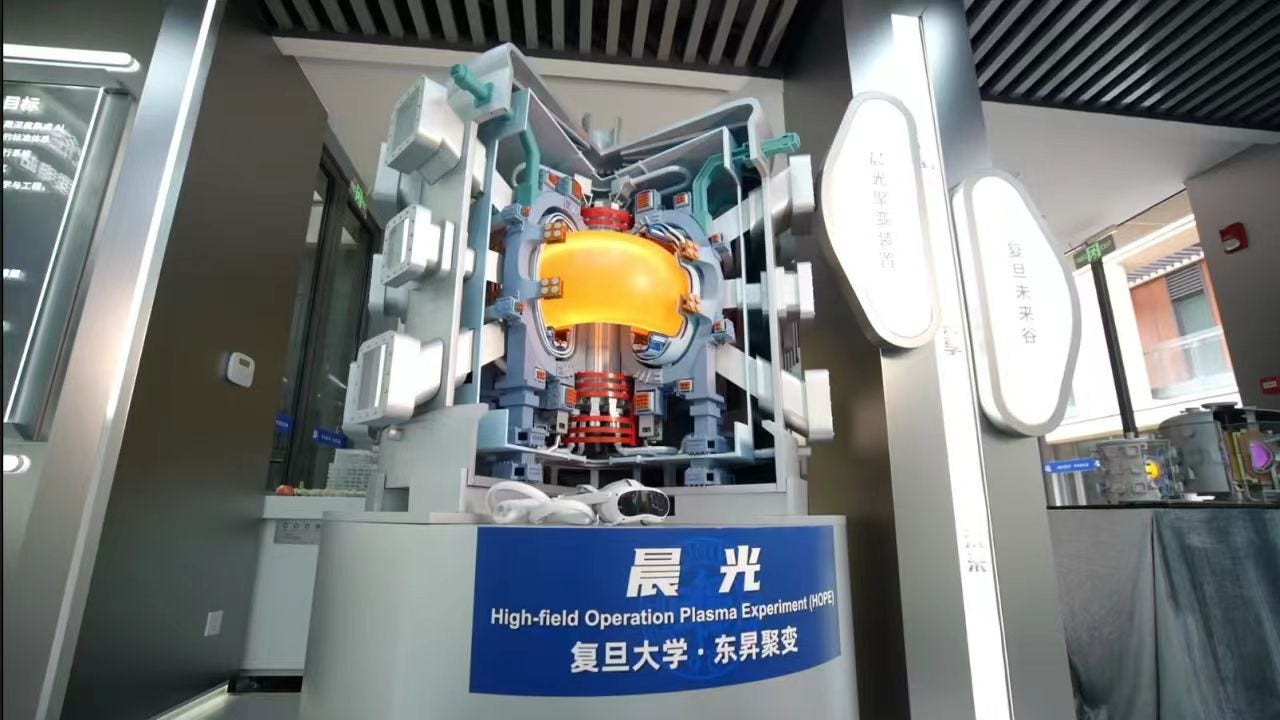

Dongsheng Fusion (东昇聚变)

New round (labeled Pre-A), hundreds of millions of RMB, co-led by CMC Capital’s carbon-neutrality fund

A fusion startup chasing the cleaner, harder reaction, incubated at a top Shanghai university.

Dongsheng Fusion, based in Shanghai and incubated by Fudan University’s Institute of Modern Physics, is pursuing a particularly ambitious flavor of nuclear fusion. Most fusion efforts fuse deuterium and tritium, which throws off torrents of neutrons that damage the reactor and make it radioactive. Dongsheng targets a deuterium-helium-3 reaction that produces almost no neutrons, which in principle allows a smaller machine that could sit closer to a city. It uses high-temperature superconducting magnets and AI-driven plasma control, and runs an experimental device named Chenguang (晨光). This week it raised a new round, reported in the hundreds of millions of RMB, co-led by the carbon-neutrality fund of CMC Capital.

The deal is a study in how China is pricing frontier science. The founder, Fudan fusion physicist Xu Min (许敏), was recruited in 2025 specifically to build this team; the company was founded only in mid-2025 and raised its angel round in January 2026, drawing a syndicate of Sequoia China, IDG Capital, and Hillhouse. Investor databases put this round’s valuation near ¥3 billion, but no announcement confirms it, and for a company with no demonstrated plasma result and barely a year of history, that figure reflects the team’s pedigree, not any measure of technical progress. Fusion is the highest-conviction, longest-duration bet on this list.

Investors: CMC Capital (CMC资本) carbon-neutrality fund (co-lead); angel backers Sequoia China (红杉中国), IDG Capital (IDG资本), Hillhouse (高瓴), and Fudan Science Park (复旦科创).

Also on the Radar

Tianji Intelligent (天机智能). Series B, ¥1 billion (~$139M). Force-control robot arms; one of the week’s largest robotics rounds, co-led by Meituan and Hillhouse, signaling a delivery giant positioning to own the arms behind its automation. Valued at ¥9 billion (~$1.25B).

Moffett AI (墨芯人工智能). Series C, ¥1 billion (~$139M). AI chips built on “sparse computing,” which skips the zero-value math in a neural network to do more work per watt. Valued at ¥6 billion (~$833M).

Beijing Link-Touch (蓝点触控). Series C+, hundreds of millions of RMB. Six-axis force sensors, the touch-sensitive joints that let robots handle delicate objects. Backed this round by carmaker and chip-industry strategics including SAIC. Valued at ¥6 billion (~$833M).

Volant Aerotech (沃兰特航空). Series C+, ¥1 billion (~$139M). Passenger electric vertical-takeoff-and-landing aircraft (air taxis). Among the better-funded Chinese eVTOL makers, valued at ¥15 billion (~$2.08B).

Shenfu Jianxing (神复健行). Angel, ¥300 million (~$42M). Implantable brain-spine interface aiming to restore movement after paralysis by rebuilding the signal path between brain and spinal cord. Led by Cathay Capital.

MatriQ (原子矩阵). Series A, hundreds of millions of RMB. Neutral-atom quantum computing, one of the leading hardware approaches to a useful quantum machine. Backed by Monolith and Vertex.

HeyGears (黑格科技). Series C, ¥300 million (~$42M). Industrial 3D printing, with a strong dental-printing position and a majority of revenue from overseas markets.

Xiandao Laser (先导激光). Series A, ¥900 million (~$125M). The laser-systems business of industrial group Xiandao; one of the week’s largest manufacturing rounds, funded by its parent.

Shuowei Photonics (烁威光电). Pre-A, ¥100 million (~$14M). Perovskite solar cells engineered for spacecraft. Perovskite can be made as thin, lightweight films rather than the rigid silicon wafers in normal panels, generating more power per gram, which matters when every kilogram sent to orbit costs a fortune.

Vefan Intelligent (维泛智能). Seed, hundreds of millions of RMB. Brain-inspired chips meant to be a robot’s onboard “brain,” pairing standard processing with spiking neural networks that fire in pulses only when something changes, the way an eye reacts to motion, using a fraction of the power of always-on chips.

The Bigger Picture

The battery glut reaches the cap table

China’s battery industry became the go-to example of its manufacturing scale. This week showed the other side of that scale. Sunwoda EVB, the sixth-largest domestic battery maker by 2025 installed volume, raised at a valuation about 31% below its prior round, with state banks in and the 2022 carmaker investors out.

The underlying problem is overcapacity. In the first eight months of 2024, China produced 419.7 GWh of power batteries but installed only 219.2 GWh in vehicles, an installation rate of just 52%, meaning roughly half the batteries made that year sat in warehouses rather than cars. That gap between output and demand is what forces prices down: factories keep running to cover their fixed costs, inventory piles up, and cell makers cut prices to move it. Prices fell accordingly: as the price of lithium carbonate, the key raw material, collapsed through 2024, battery-cell prices dropped with it. For a manufacturer whose costs are mostly fixed plant and equipment, a sustained price cut on every cell sold can erase a year of profit fast. The pain is not evenly shared. CATL and BYD together still held about 65% of China’s installed volume in 2025, and run their plants at 80 to 90% utilization with healthy margins. The second tier runs at 60 to 70%, and by early 2026 several were near breakeven or in the red on their battery divisions, carrying debt above 60% of assets.

That gap is why this week’s two battery deals point in opposite directions. The commodity-cell maker takes a markdown and a state-bank backstop. The two-year-old solid-state startup, with no revenue, attracts a billionaire’s first battery bet at a ¥2.5 billion valuation. Capital is shifting away from the part of the market that has become a commodity and toward the chemistry that might reset the game. The battery sector is the clearest case of what happens when production outruns demand: output keeps growing, prices fall, and only the leaders with utilization high enough to absorb it stay profitable.

China’s race to build a non-Nvidia compute stack

Xingyun builds inference chips around cheap commodity memory instead of HBM; others raised this week on sparse computing and compute-in-memory designs. The common thread is cost: do AI computing more cheaply, and do it without the parts the US will not sell.

That instinct has a powerful tailwind. US export controls that took effect in late 2024 cut China off from the leading-edge high-bandwidth memory that high-end AI chips depend on, turning memory substitution from a clever idea into a structural necessity. And Huawei is building the rest of the alternative stack in public. In August 2025 it open-sourced CANN, the software layer that lets developers program its Ascend AI chips. That is a direct answer to Nvidia’s CUDA, the programming environment Nvidia has spent nearly two decades turning into the default language of AI development; because nearly every AI tool and library was written for CUDA first, moving to a rival chip has meant rewriting that whole software stack, which is the real lock-in. Opening CANN lets any developer adapt it, the first step toward building the same kind of gravity. In March 2026 Huawei took its Atlas 950 supercomputing system to MWC in Barcelona, its first global showcase of a cluster built entirely on Huawei silicon, interconnect, and in-house memory.

The startups raising this week sit downstream of that push. They do not need to beat Nvidia on raw performance; they need to make Chinese AI workloads run acceptably on parts China can actually obtain and afford. Inference, the day-to-day work of answering queries, is far less memory-hungry than training, which is exactly why a wave of startups is attacking it with cheaper memory and novel architectures. The bet across the sector is the same: in a market walled off from the best imported hardware, the winner is whoever produces acceptable inference at the lowest cost on parts China can actually source.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.