The China Round — May 8, 2026

Kimi Hits $20B, a Fusion Unicorn Emerges, and the Deals That Couldn’t Wait

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Where capital flows tells you where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

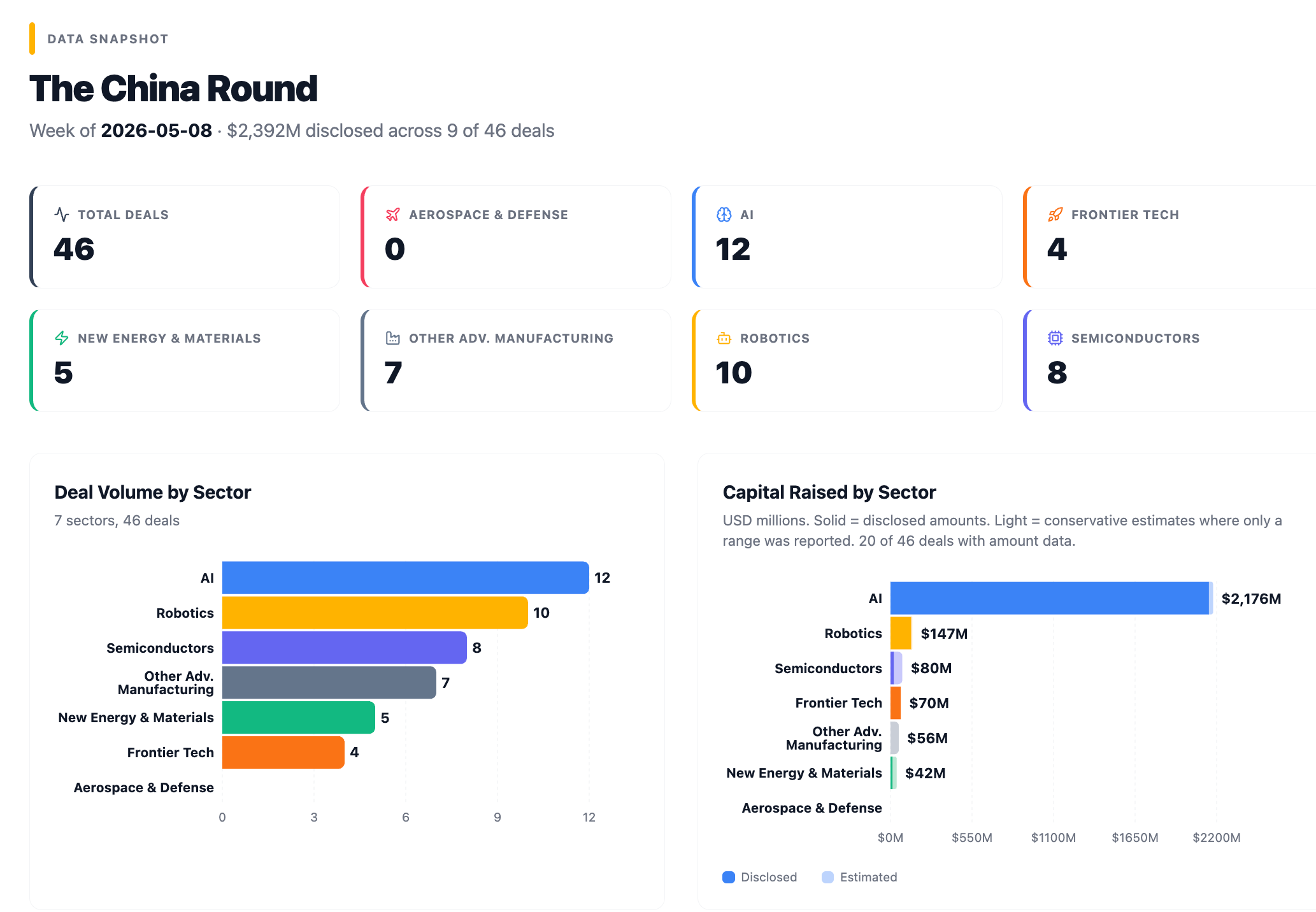

Where the Money Went

Whether you were celebrating Labor Day, Cinco de Mayo, or just enjoying a long weekend, China’s five-day May Day holiday (May 1-5) kept most dealmaking on hold.

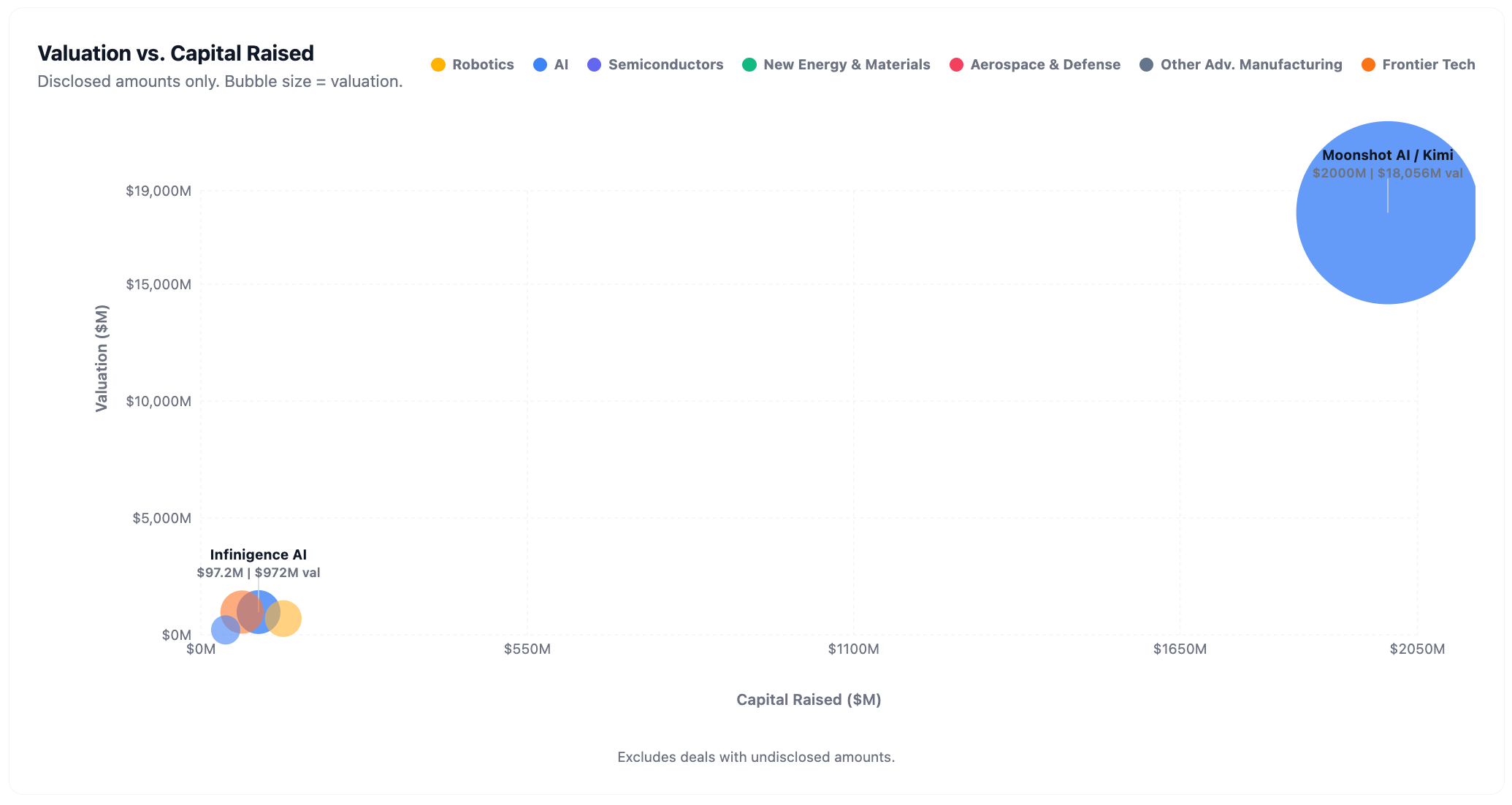

46 deals, $2.39B (~¥17.2B) in disclosed capital across nine of them. That number needs context: Kimi’s $2B D-round accounts for 84% of the total. Strip it out and 45 deals generated $390M (~¥2.8B). AI led on deal count at twelve, with robotics close behind at ten. No aerospace deals.

🧠 AI (12 deals)

One deal dominates the entire week: Kimi’s $2B (~¥14.4B) D-round at a ~$20B (~¥144B) valuation, the largest Chinese LLM startup round of 2026. Beneath that headline, two AI infrastructure companies raised a combined ¥1B+ (~$139M+) in the same week with identical “token factory” positioning: Infinigence AI at ¥700M+ (~$97M+) and Magik Compute at hundreds of millions. Nanochap took a ¥300M (~$42M) strategic round for biomedical chips targeting visual brain-computer interfaces, a medical device company tagged as “AI” on deal trackers. The remaining deals include PixelBloom’s C-round for its AiPPT product (30M+ registered users globally), a medical LLM angel (WiseDiag, ¥65M / ~$9M), a spatial intelligence platform strategic round (XGRIDS), and four late-reported deals spanning industrial cognitive AI, AI infrastructure cloud, and AI-driven drug discovery.

🤖 Robotics (10 deals)

RoboScience pulled the largest robotics round of the week at ¥1B (~$139M) for its VLOA embodied AI platform. The remaining main-window deals are earlier-stage: Eagle Vision raised a Pre-A for bionic flapping-wing flying robots with a consumer product targeting the global hobbyist market, Westlake Robotics for civilian quadruped robots, Knownobound for industrial embodied AI targeting ship maintenance and container logistics, and underwater robotics veteran Boya Gongdao closed a D+ round. Five late-reported deals brought the sector total to ten, including a Sequoia China-backed angel in smart robots and a strategic round in core robot components backed by iFlytek Ventures and Hillhouse.

🔬 Semiconductors (8 deals)

Eight deals spanning the full chip stack, from data center networking to automotive SoCs to photonic interconnects. Yunsilicon builds what it describes as China’s first 400Gbps RDMA data center networking chip, positioning it as the domestic alternative to Nvidia’s ConnectX; ByteDance and Inspur hold strategic equity stakes. Oritek closed a C-round for automotive zone controller SoCs, with SDIC Merchants participating in every round from B1 through C and eight listed auto companies as shareholders. Siminwei drew three top-tier VCs (Oriental Fortune Capital, GGV Capital, Detong Capital) to co-lead a seed at a ¥500M (~$69M) valuation for AI inference architecture, an unusually heavy syndicate for a seed. Rhinoptix raised for TFLN photonic chips, the post-copper datacenter interconnect technology covered in the April 10 issue. Sicred continues scaling SiC power devices with 100,000+ units shipped to aerospace and defense customers.

⚙️ Other Advanced Manufacturing (7 deals)

Tachin Tech raised a Pre-A for electronic skin targeting the humanoid robot market, with core technology from Zhenan Bao’s Stanford lab. Makera closed a Series A for consumer desktop CNC machines after raising $10.2M on Kickstarter. Three smaller deals: a smart lighting company in Shenzhen (Mingyuda, ¥30M HKD / ~$3.8M), a consumer electronics angel backed by Co-Creation Ventures, and a miHoYo-backed equipment investment. Two late-reported deals added a metal 3D printing angel and a high-speed SMT equipment strategic round.

⚡ New Energy & Materials (5 deals)

BYD invested directly in battery electrolyte materials maker Huasheng Xianghe (strategic, hundreds of millions RMB), continuing its vertical integration down the EV supply chain. Hebang New Materials raised a ¥100M (~$14M) A-round for bio-based composite materials certified to EU high-speed rail standards. Three late-reported deals added carbon-based energy storage materials and emerging energy tech to the tally.

💡 Frontier Tech (4 deals)

STARTORUS closed a ¥500M (~$69M) A+ for its fusion energy reactor, crossing the $1B (~¥7.2B) valuation mark. Greencloud, a subsidiary of listed Wangsu Technology, raised for immersion liquid cooling with partnerships across Intel, Dell, and BASF. Nanoloop took a seed for sports brain-computer interface wearables at ¥10M+ (~$1.4M+). One late-reported deal: Boyin Bio raised an A-round for biomaterials from Legend Capital, CAS Advanced Industry Fund, and Cornerstone.

Other sectors

No aerospace or defense deals this week.

Spotlight

Kimi (月之暗面)

Series D, $2B (~¥14.4B), ~$20B (~¥144B)

China’s best-funded independent LLM startup hits frontier parity and raises the largest Chinese AI round of 2026.

Kimi is an LLM platform built by Moonshot AI. K2.6, released April 2026, beats or matches GPT-5.4, Claude Opus 4.6, and Gemini 3.1 Pro across coding, reasoning, and agent benchmarks, topping the field on Humanity’s Last Exam, DeepSearchQA, and SWE-Bench Pro. The K2.5 launch in January triggered a subscription surge of over 8,000% in a single month. Annual recurring revenue broke $100M (~¥720M) by March 2026 and exceeded $200M (~¥1.44B) by April. Founder Yang Zhilin studied at Tsinghua and CMU, worked at Google Brain and Meta AI, and co-authored Transformer-XL and XLNet, two foundational papers in the architecture behind modern LLMs.

Meituan Longzhu, the venture arm of China’s largest local services platform, led with over $200M (~¥1.44B). Meituan operates food delivery, ride-hailing, hotel booking, and grocery for 700M+ annual transacting users. If Kimi becomes the AI layer inside those services, that means agentic AI embedded in hundreds of millions of daily purchasing decisions. China Mobile’s innovation fund and CPE Yuanfeng co-invested, adding state telco infrastructure and financial capital alongside commerce, each representing a different distribution thesis for the same model. The valuation jumped from $4.3B (~¥31B) in December 2025 to $20B (~¥144B) in six months, with approximately $3.9B (~¥28B) raised in that sprint.

Meituan Longzhu (美团龙珠, lead), China Mobile Innovation Fund (中移创新产业基金), CPE Yuanfeng (CPE源峰), and Shuimu Capital (水木资 本).

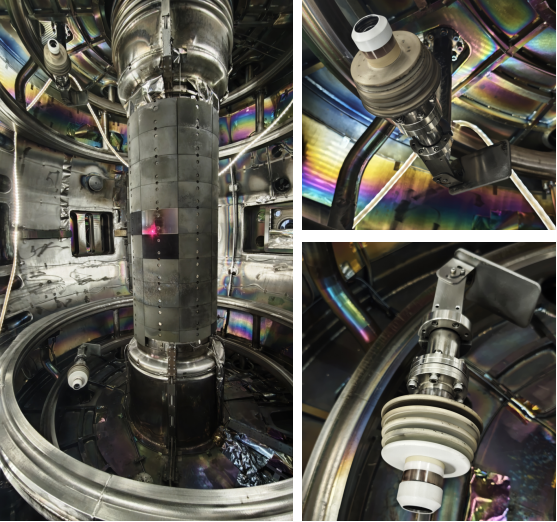

STARTORUS (星环聚能)

Series A+, ¥500M (~$69M), exceeded $1B (~¥7.2B+)

China’s latest fusion unicorn, building a reactor geometry no other company has attempted at commercial scale.

STARTORUS is building a compact fusion reactor: a spherical tokamak, which uses powerful superconducting magnets to contain hydrogen plasma heated to hundreds of millions of degrees inside a doughnut-shaped chamber. STARTORUS’s approach uses a plasma geometry called negative triangularity. In standard tokamaks, the edge of the plasma periodically erupts in instabilities that blast over 1 GW per square meter into the reactor wall, a problem that has plagued the field for decades. Negative triangularity reshapes the plasma cross-section to suppress these eruptions entirely, reducing wall damage and improving energy confinement. STARTORUS claims to be the first company building a commercial spherical tokamak natively around this geometry. (The University of Seville’s SMART research tokamak achieved first plasma with negative triangularity in January 2025, but as an academic device, not a commercial reactor.) The NTST device begins installation in September 2026 at the company’s Shanghai Jiading base, with the demonstration reactor 星环一号 (CTRFR-1) targeted for construction in 2028, design targets by 2029, and electricity output around 2032. Chief Scientist Tan Yi has spent over 20 years in fusion research since entering Tsinghua’s Department of Engineering Physics in 1999.

The A-round in January (¥1B / ~$139M, led entirely by Shanghai state capital) broke the domestic record for a single private fusion round. The A+ brought 11 new investors four months later, pushing cumulative funding past ¥2B (~$278M). At a valuation exceeding $1B (~¥7.2B+), STARTORUS joins NeoFusion (聚变新能) in a small club of Chinese private fusion unicorns, in a field where fusion energy generates zero watts commercially anywhere on Earth. Commonwealth Fusion Systems, TAE Technologies, and Helion have each raised more capital, but none uses negative triangularity. If NTST produces results in late 2026, STARTORUS enters a global race with technically differentiated physics.

Dachen Finance (达晨财智), Jinpu Investment (金浦投资), Shenneng Chengyi (申能诚毅, Shenergy affiliate), Sunshine Ronghui Capital (阳光融汇资本), Industrial Securities Capital (兴证资本), Songqing Capital (松青资本), Hongtai Fund (洪泰基金), Sanyuan Capital (三元资本), Jingming Capital (京铭资本), Yinggang Capital (盈港资本), and Feitu Ventures (飞图创投, returning from A-round).

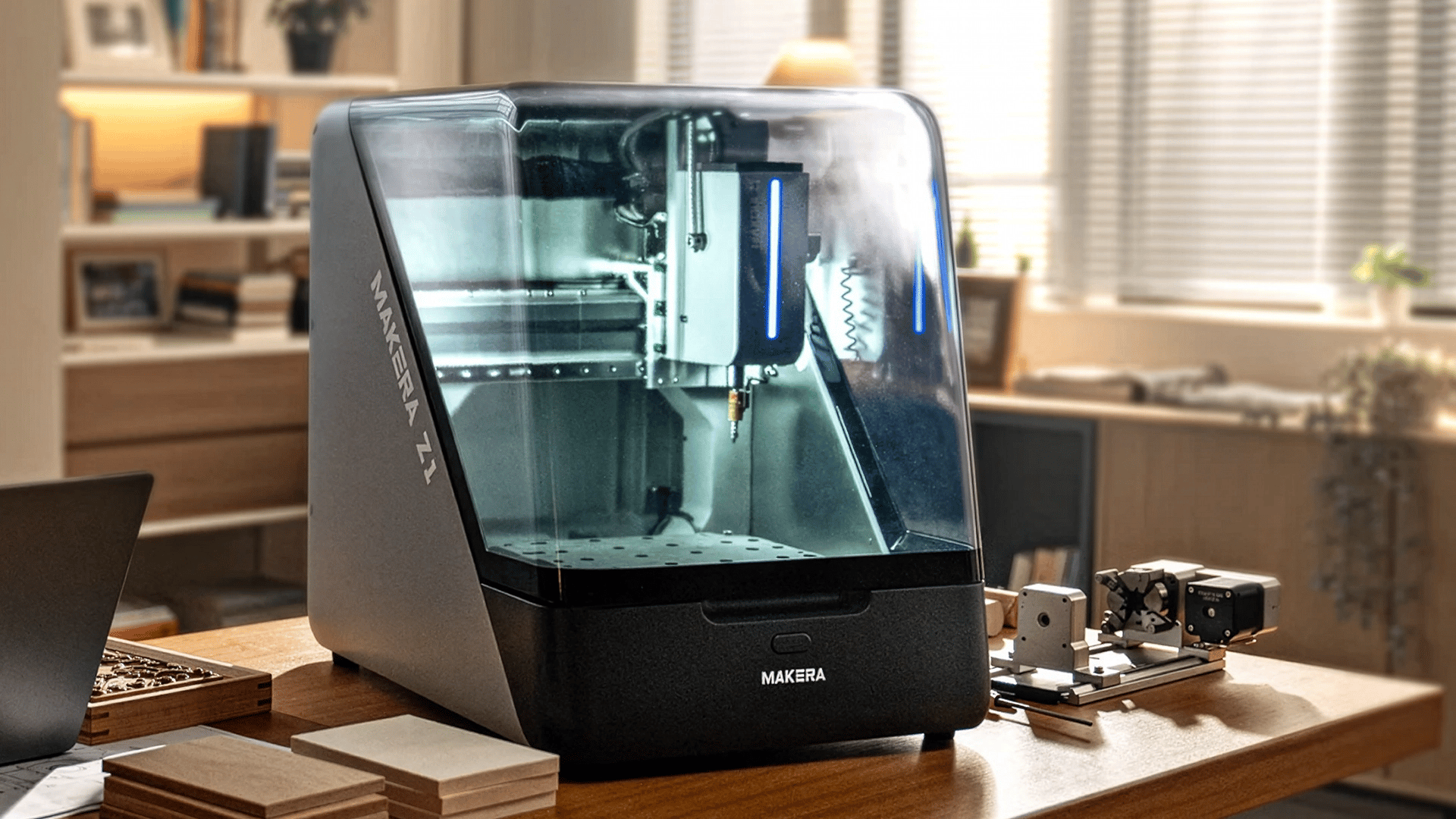

Makera (造物时代)

Series A, hundreds of millions RMB, ¥1.5B (~$208M)

$10.2 million on Kickstarter in 45 days. A Chinese consumer hardware brand built for the global maker market from day one.

Makera builds consumer desktop CNC machines that bring precision machining to workshops, research labs, and home studios. CNC machines carve, cut, and engrave materials using computer-controlled toolpaths; industrial units cost $50,000 or more. Makera puts comparable capability on a desktop for under $1,000. The Z1, launched on Kickstarter in late 2025, raised $10,245,134 from 6,927 backers in 45 days.

Its earlier products, Carvera and Carvera Air, held the top two spots among CNC campaigns on Kickstarter before the Z1 surpassed both. Products are used at MIT’s Center for Bits and Atoms and, per the company, at over 1,000 enterprise and university customers including Apple, Toyota, and Volkswagen. Full-year 2025 revenue grew over 400% and Q1 2026 is tracking nearly 300% year-on-year, per the company’s Series A announcement.

The Series A came less than eight months after Qiming Venture Partners’ Pre-A, with Qiming investing well above its proportional share of the round, a strong conviction signal from one of China’s top VCs. The co-lead is Beijing’s Municipal AI Industry Investment Fund, an unusual backer for consumer hardware, suggesting the fund sees the intelligent CAM software layer as part of its AI mandate. Makera was never a “China company going global.” It was born on Kickstarter, priced in dollars, and validated by Western makers before any domestic narrative. In a week dominated by AI infrastructure and robotics, Makera is the clearest evidence that China can build global consumer hardware brands, not just supply chains.

Meridian Capital (华映资本, co-lead), Beijing Municipal AI Industry Investment Fund (北京市人工智能产业投资基金, co-lead), Oriza Puhua (元禾璞华), CASIC Ventures (中科创星), TsingVenture (清科创投), and Qiming Venture Partners (启明创投, returning).

Infinigence AI (无问芯穹)

Series B, ¥700M+ (~$97M+), ¥7B (~$970M)

One of China’s best-funded AI infrastructure startups, betting that the token production layer becomes the durable moat in AGI.

Infinigence AI builds inference and training infrastructure that runs across multiple chip architectures simultaneously. Where most AI companies optimize for Nvidia GPUs, Infinigence orchestrates workloads across AMD, Huawei Ascend, Moore Threads, and seven other domestic chip families, turning heterogeneous hardware into a unified compute pool. The platform hosts over 160 models and serves enterprise clients whose daily token call volume has grown 20x year-on-year. The Tsinghua NICS lab spinout positions itself as a “token factory,” a framing its CEO used at a March 2026 industry forum: converting raw compute into AI tokens the way a refinery converts crude into usable fuel. Cumulative funding now exceeds ¥2.2B (~$306M), with 15 investors in this round alone.

The thesis is that AI models will commoditize, as DeepSeek’s open-source success suggests, but the logistics layer (scheduling across fragmented chips, optimizing for cost and latency, routing traffic between models) will not. This is the AWS argument applied to AGI: the largest cloud provider did not build the most applications; it built the best infrastructure for running them. The risk is equally visible. China’s hyperscalers (Alibaba Cloud, Baidu Cloud, Huawei Cloud) run their own inference platforms. ByteDance runs Doubao inference internally. The token factory thesis works for the long tail of agent startups and enterprise AI deployments. Whether it works against vertically integrated giants is the open question that ¥2.2B in cumulative capital is now testing.

Hangzhou High-Tech Capital (杭州高新金投, co-lead), Huiyuan Capital (惠远资本, co-lead), Guoxing Capital (国兴投资), Qinhuai Data (秦淮数据), and others. Returning: Legend Capital (君联资本), Shanghai Guotou Futeng (上海国投孚腾), Yuanzhi Future (元智未来).

RoboScience (机科未来)

Series A, ¥1B (~$139M), ¥5B (~$694M)

Founded in late 2024, Series A by May 2026 with no shipping hardware. The same architectural bet as Physical Intelligence in the US.

RoboScience is building an embodied AI platform centered on VLOA (Vision-Language-Object-Action), a model that learns to control robots the way language models learn language: absorb massive amounts of visual and manipulation data, then generalize to tasks it has never seen. Instead of programming a robot arm to pick up a specific object with a specific motion, you show it millions of examples and let it figure out the movements itself. The approach mirrors Physical Intelligence’s Pi model in the US. The company has accumulated over one million hours of manipulation data, growing at tens of thousands of hours per week. Co-founder Tian Ye was Apple’s AI platform technical lead after earning his MS at Stanford under Andrew Ng. Co-founder Lin Shao is an NUS assistant professor with a Stanford AI Lab PhD whose D(R,O)Grasp framework won the Best Paper Award for Robot Manipulation at ICRA 2025, the field’s top international conference.

¥1B for a company roughly 18 months old with no shipping hardware is aggressive, but within the norms of China’s embodied AI funding cycle; Galbot raised a comparable amount at a similar stage. The unnamed investor list, described only as “domestic and international industry giants and top financial institutions,” is its own signal: in China’s AI market, investor anonymity usually means either strategic sensitivities or credentials that don’t match the framing. Early investors include JD.com (angel lead, a company that operates one of China’s largest logistics networks), Merchants Capital, and SenseTime’s venture arm. JD.com’s involvement points to the deployment thesis: last-mile logistics as the proving ground for general-purpose manipulation. The question is whether VLOA’s data-scale approach produces generalizable robot intelligence faster than the task-specific approaches used by companies already shipping thousands of units.

JD.com (京东, angel lead), Merchants Capital (招商局创投), SenseTime Guoxiang Capital (商汤国香资本), Zero One Ventures (零一创投), Puhua Capital (普华资本, Pre-A lead), and others. Series A investors undisclosed.

Also on the Radar

Tachin Tech (途见科技) — Pre-A + Pre-A+, hundreds of millions RMB, ¥600M (~$83M)

Electronic skin for robots. 400 sensors per square centimeter detecting pressure, temperature, shear force, texture, and proximity. Founder Lai Jiancheng was a Stanford postdoc in Zhenan Bao’s lab, one of the world’s leading groups in flexible electronics. The haptic data collection glove is the clever wedge: sell the training data tool (human demonstrations converted to robot learning data) before the full-body robot skin market matures. Lenovo Star (联想之星) leads; Huakong Fund (华控基金) and Oriza Puhua (元禾璞华) co-invest.

Yunsilicon (云脉芯联) — B-round, hundreds of millions RMB (~$42M+), ¥7B (~$970M)

The YSA-100, which the company describes as China’s first 400Gbps RDMA data center networking chip, has been in mass production since 2024 and positions the company as a domestic alternative to Nvidia’s ConnectX series. CEO Liu Yongfeng previously led networking chip development at Cisco, Alibaba, and Huawei. ByteDance (8.42%) and Inspur (6.86%) hold strategic equity stakes. The reported investor list includes the National IC Fund, Shanghai IC Fund, and National AI Industry Fund. Three national-level semiconductor and AI funds in a single chip startup would be unusual; worth watching for public confirmation.

Oritek (欧冶半导体) — C-round, hundreds of millions RMB, ¥1.5B (~$208M)

Automotive SoC chips for third-generation electrical/electronic architecture, the “central computing + zone control” design that the entire global auto industry is migrating toward. Oritek’s Gongbu series zone controller chips are among China’s first domestic entries in this segment. Eight listed auto-industry companies are shareholders, including SAIC, Xingyu, AAC Technologies, and Sunny Optical. SDIC Merchants has participated in every round from B1 through C.

Nanochap (暖芯迦) — Strategic, ¥300M (~$42M), ¥1.5B (~$208M)

Biomedical chip company developing visual brain-computer interfaces competing with Neuralink’s Blindsight. R&D center in Melbourne, 13 international patents, and an EPC001 chip that reads ECG, PPG, EEG, and EMG signals simultaneously. Tagged “AI” on deal trackers but this is a medical device company at its core. The team holds dual degrees across electrical engineering and biomedicine, with veterans from major semiconductor companies.

Legend Capital (君联资本, lead), Guangfa Xinde (广发信德).

PixelBloom / AiPPT (像素绽放) — C-round, undisclosed, ¥250M (~$35M)

AI presentation generation tool with 30M+ registered users across 180+ countries, ranked #4 globally in the AI PPT vertical and #1 among startups in China. Founded in Singapore in 2018, making it a genuinely global-first product rather than a China-domestic pivot. The modest C-round valuation suggests either an undervalued global product or a structured round.

CASIC Capital (国科投资, co-lead), Guoxiang Capital (国香资本, co-lead), Cornerstone Ventures (基石创投).

Rhinoptix (犀里光电) — Pre-A, tens of millions RMB, ¥150M (~$21M)

Thin-film lithium niobate (TFLN) photonic chips for data center optical interconnects. Founder Prof. Wang Cheng co-invented TFLN electro-optic modulators at Harvard and holds a Tsinghua undergrad. TFLN switches light signals roughly 10x faster than silicon photonics, the leading candidate for post-copper datacenter connections as AI clusters push past 1.6 terabits per second. Founded January 2025 and already raising, a pace that reflects strong VC confidence in the technology.

Lenovo Ventures (联想创投), Oriza Origins (元禾原点).

Sicred (至信微电子) — B-round, undisclosed, ¥150M (~$21M)

SiC MOSFETs (silicon carbide power switches that handle high voltage more efficiently than traditional silicon) for aerospace, defense, and industrial power conversion. 100,000+ units shipped at 1200V/7mΩ with over 90% yield. Founder Zhang Aizhi previously worked at STMicroelectronics and Huarui Micro, bringing 20+ years in power device design. SiC is a critical technology for global EV and industrial electrification, and Sicred’s shipping volume at B-round stage is unusual.

China Venture Capital (中国风投), Tianhu Fund (天互基金).

Greencloud (绿色云图) — A-round, undisclosed

Immersion liquid cooling for AI data centers, claiming a PUE of 1.049, meaning 95% of energy goes to compute and only 5% to cooling. Subsidiary of listed Wangsu Technology (603000.SH). Strategic partnerships with Dell (2023), Intel co-development (2024), and a BASF joint lab for biodegradable coolant (2025). As AI training clusters demand increasing power density, the thermal management layer is becoming infrastructure, not an accessory.

Yunze Capital (云泽资本).

Eagle Vision (鹰瞰智翼) — Pre-A, tens of millions RMB, ¥150M (~$21M)

Bionic flapping-wing flying robots and a proprietary fluid simulation engine. Consumer product “Dante” targeting global hobbyist and enthusiast markets with stunt flying capabilities, with a Kickstarter campaign for global distribution. Core team from Shanghai Jiao Tong University with PhD-level backgrounds in robotics and control. A left-field entry in a week dominated by humanoid robots and LLMs.

Oriza Origins (元禾原点).

Hebang New Materials (禾邦新材) — A-round, ¥100M (~$14M), ¥500M (~$69M)

Bio-based composite materials from plant biomass, specifically extracting high-purity lignin from agricultural straw using an enzymatic process the company describes as a world first in commercialization. 25% carbon intensity reduction versus petroleum-based epoxy. Certified to EN45545 (EU high-speed rail fire safety standard) and UL94 V-0. Applications: aerospace, transportation, and high-end equipment. Sustainable materials with real certifications, not just a green narrative.

Changjiang Capital (长江资本), Hefei Innovation Investment (合肥创新投资).

The Bigger Picture

Two Token Factories, Same Week, Same Pitch

Two companies raised ¥1B+ combined on the same thesis within 48 hours of each other: the data center as “token factory.”

Infinigence AI (¥700M+ B-round) and Magik Compute (魔形智能) (hundreds of millions Pre-A) both position themselves as “token factories,” middleware layers that convert raw compute from heterogeneous chip pools into AI inference tokens at scale. Infinigence is the Tsinghua spinout profiled in Spotlight above; Magik Compute, founded June 2024 by former Alibaba Cloud and Bitfusion executives, is building software-hardware co-optimized compute clusters for the same market from a different angle.

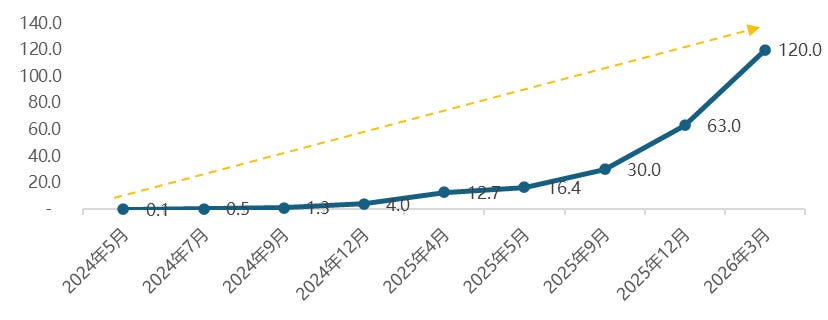

The demand side supports the bet: China’s daily AI token call volume hit 1.4 quadrillion in March 2026, a 1,000x increase in two years per Xinhua, citing official data. Kimi’s own capacity crunch in early 2026, documented by TMTPost, saw users turned away because inference supply could not meet demand.

But the composition of that demand matters. ByteDance’s Doubao alone accounts for 1.2 quadrillion tokens per day as of March 2026, roughly 86% of the national total, all served on ByteDance’s own Volcengine infrastructure. The token factories are not competing for that volume. ByteDance, Alibaba, and Zhipu AI build their own inference infrastructure and monetize spare capacity through their own platforms. Kimi solved its shortage internally with software optimization rather than outsourcing. The token factory thesis holds for the long tail: agent startups, enterprise AI deployments, and smaller model companies that lack the scale to justify proprietary GPU clusters. Whether that long tail produces durable revenue before China’s hyperscalers expand downmarket is the bet that ¥1B+ in same-week capital is now testing.

Built Global, Not Going Global

Three companies in this week’s batch illustrate different modes of global competitiveness, none following the traditional Chinese playbook.

Makera raised $10.2M on Kickstarter for a desktop CNC machine, with a predominantly Western backer base. PixelBloom’s AiPPT serves 30M+ registered users across 180+ countries from a Singapore-incorporated entity. Both were global products before they became Chinese tech stories, built for foreign users from day one. Kimi’s path is different. K2.6 competes directly with GPT-5.4 and Claude Opus 4.6 on the benchmarks that define the global AI frontier, even though Kimi’s revenue comes overwhelmingly from Chinese users.

The traditional model is “先做国内再出海” (build at home first, then go overseas). A newer pattern is emerging: companies that set up overseas operations from inception and validate product near end users without a domestic-first phase. TechNode’s Born Global 2026 Awards and CGTN’s analysis of China’s next-gen global enterprises cover the same shift. Chinese companies’ overseas revenue ratio stood at 16.7% in 2024 per CICC, with Goldman Sachs projecting 20.6% by 2028. Companies like Makera and PixelBloom are part of the reason.

Why These Deals Couldn’t Wait

46 deals versus 100-plus in normal weeks. The May Day break (May 1-5) shut the marginal deals down, but the rounds that closed during the holiday all had reasons they couldn’t pause.

Commercial breakout on a clock. Kimi’s ARR doubled in a single month. When revenue is accelerating that fast, every week of delay means a higher valuation for incoming investors. Meituan closed at $20B before the next step-up. Makera’s revenue was tracking 300% year-on-year post-Kickstarter, and Qiming wanted to load up before the metrics cooled.

Construction deadlines. STARTORUS needs capital before the NTST device installation begins in September 2026. The 11 new A+ investors closed in four months because fusion reactor construction schedules do not care about national holidays.

Category definition races. Infinigence AI and Magik Compute both announced within 48 hours, racing to establish the “token factory” category. When two companies pitch the same thesis to the same investor base, whoever closes first sets the narrative. Waiting a week means the other company’s press coverage defines the category for you.

The 50-plus deals that did not happen this week were the ones that could afford to. What closed: AI infrastructure, frontier energy, and globally validated products.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.