A Second Opinion

Why China's super-apps might have the edge over Silicon Valley in healthcare AI

Introduction

OpenAI and Anthropic have just launched dedicated healthcare AI products, entering a market projected to exceed $100B globally by 2030, driven by millions of users turning to AI for health advice.

Anthropic has found breakout success with Claude Code, its command-line assistant that’s become the tool of choice for a growing slice of developers, and knowledge workers. OpenAI has pushed into search with ChatGPT’s browsing capabilities and is reportedly working on dedicated hardware with Jony Ive, the designer behind the iPhone.

But healthcare is the first vertical where both companies have launched dedicated, branded products at nearly the same time. Why?

The numbers explain the opportunity, and the urgency:

230 million people ask ChatGPT health questions weekly; 40 million daily

In areas 30+ minutes from a hospital, users send ChatGPT over 580,000 healthcare messages weekly

The US will face a deficit of 86,000 physicians by 2036

Physicians spend 27% of their office day on direct patient time and 49% on EHR (electronic health records) and desk work

43% of physicians report burnout; more than one-third of burned-out primary care physicians plan to stop seeing patients in the next one to three years

94% of patients experience delays in care due to prior authorizations; 78% abandon treatment altogether

Physicians complete an average of 39 prior authorizations weekly, spending 13 hours on the process

US healthcare administrative spending is approximately $1 trillion annually, now accounting for more than 40% of total hospital expenses

Sources: Stanford Medicine, American Medical Association, American Hospital Association, Commonwealth Fund, AJMC, PMC/NIH

Both frontier model companies are just getting started in the sector. OpenAI is running pilots with eight US hospitals, connecting patient portals, training physician-led testing groups on GPT-5. Anthropic is signing enterprise deals with pharma companies and health systems, building HIPAA-compliant (US healthcare privacy law) connectors, rolling out a beta to US subscribers. At this stage they are focused on making the connections, training the models, and learning the regulatory ropes, hoping to convert curious users into stable, habitual ones. International timelines are unclear. OpenAI excluded Europe from ChatGPT Health at launch, citing the EU AI Act and GDPR; Anthropic’s consumer features are US-only.

The Chinese healthcare system has its own unique challenges. The country will have 400 million people over 60 by 2035. Its AI healthcare market is projected to hit $19 billion by 2030. Hundreds of millions in rural areas without easy access, and those who could reach care often overwhelming hospitals with routine visits. So China’s tech giants started building the infrastructure over a decade ago: payment rails into hospitals, doctor networks for online consultations, digital insurance systems reaching half the population, accessible 24/7 to 800 million superapp users. Generative AI was the final piece.

Here’s why China’s super-apps might have the edge over Silicon Valley in healthcare AI

Healthcare is the Next Frontier for AI Automation

AI has already begun reshaping white-collar work. Legal services got hit first, with contract review that once took junior associates days now being completed in minutes. Due diligence, document discovery, and regulatory compliance are increasingly handled by AI systems that bill you per token, not by the hour. Law firms that initially resisted are now racing to adopt, with proponents arguing that the belief human legal work is irreplaceably complex is misguided. In reality, they say legal work primarily involves pattern recognition, structure, precedent matching, argument assembly, and risk framing. That’s exactly the territory where AI thrives (though issues remain).

The US legal services market alone is worth over $400 billion, according to economic data from the U.S. Census Bureau. Globally, legal services total roughly $1 trillion by industry estimates.

Healthcare is a different beast entirely.

The Market

Various estimates for the size of the global healthcare market put it at around $9 trillion. US healthcare spending alone reached $5.3 trillion in 2024, according to CMS, and is projected to hit $8.6 trillion by 2033. The administrative overhead in US healthcare (i.e. just the paperwork) is estimated at $1 trillion per year, roughly equal to the entire global legal services market.

This is where AI comes in. Integration has been slower, with higher stakes and stricter regulations, but the market is irresistible. McKinsey estimates AI could generate $200-360 billion in annual savings in US healthcare alone, representing 5-10% of total spending. PwC projects the global AI healthcare market could reach $868 billion by 2030.

Money and talent are following the trend. US digital health startups raised $14.2 billion in 2025, the highest since 2022, with AI companies capturing 54% of total funding, up from 37% the year before.

Abridge, which turns patient conversations into clinical notes, raised $550 million across two rounds at a $5.3 billion valuation. Hippocratic AI, building healthcare AI agents, hit $3.5 billion. Ambience Healthcare pulled in $243 million for its AI operating system. Adjacent spaces are heating up too: longevity tech saw NewLimit (Brian Armstrong) raise $130 million, while Retro Bio (backed by Sam Altman) is reportedly chasing a $5 billion valuation.

OpenAI also recently acquired Torch, a health records startup, for a reported $100 million in January, and in December poached Albert Lee, who ran M&A for Google Cloud and DeepMind and worked on over $50 billion in deals, to lead corporate development. A clear signal that more acquisitions are coming.

For founders and investors watching this space, the message is clear. Health data infrastructure and AI-native healthcare plays are where the capital is flowing, both in VC funding and tech acquisitions. (For what this means outside the US, see "What This Means for Builders" below.)

The technology is already being deployed. Nearly 80% of healthcare organizations surveyed by McKinsey report using AI in at least one function, though adoption varies dramatically by region. North America leads, with an anticipated AI healthcare potential of $479 billion by 2030. Asia Pacific follows at $186 billion, though that figure may undercount China, where the market is moving faster than many Western analysts tend to track.

China’s healthcare market is already substantial. According to China’s National Health Commission, total healthcare spending reached 9.09 trillion RMB (~$1.26 trillion USD) in 2024, roughly 6.7% of GDP. The country has 5.08 million licensed physicians serving 1.4 billion people, and logged over 10 billion outpatient visits last year alone.

The Diagnosis

The U.S. and China suffer from different healthcare ailments.

The American problem is overhead.

The doctors, hospitals, and infrastructure all exist but between the patient and the care is an enormous bureaucratic apparatus.

According to the American Medical Association, physicians complete 39-45 prior authorizations per week, spending 13-14 hours on the process.

That’s a full quarter of a work week devoted to asking insurance companies for permission to treat patients.

The AMA found that 93% of physicians say prior authorization delays care, and 82% say it sometimes leads to patients abandoning treatment altogether. The system costs an estimated $35-55 billion annually in administrative overhead, according to Health Affairs. And when patients or providers do appeal denied claims, nearly half are overturned, per KFF, suggesting insurers routinely reject claims they know are valid.

These inefficiencies ultimately fall on patients. Three in ten Americans with chronic conditions skip doses or don’t fill prescriptions because of cost (KFF). Among the uninsured, 75% forgo needed care entirely (Commonwealth Fund). The system spends more than any other in the world, yet that spending often adds administrative complexity, not better outcomes.

Healthcare is now carrying the US labor market. In 2025, the sector added 713,000 jobs. Stripped of healthcare and social assistance, the broader market would have posted net job losses. But adding bodies alone won’t solve a structural problem.

The Chinese problem is overflow.

On paper, China’s healthcare system is substantial: 5.08 million physicians, over 10 billion outpatient visits annually, $1.26 trillion in spending. But the numbers that matter aren’t the ones that exist today but the ones that are coming. According to China’s National Health Commission, the country currently has 220 million people over 65, about 15.6% of the population. By 2035, that number will exceed 400 million, more than 30%.

By 2030, an estimated 200 million Chinese will live in single-person households, many of them elderly, which has led to a wave of youth anxiety. In January, a $1 app called 死了么 (”Are You Dead Yet?” - a play on food delivery app 饿了么, “Are You Hungry?”) hit #1 on China’s iOS charts. It’s quite literally a dead man’s switch, where you check in daily or your emergency contacts get alerted. A nifty app, apparently vibe coded in a month.

In China, patients are generally free to seek care directly at any level of the system, including large hospitals, without first seeing a local doctor. Primary care clinics exist, but they do not control access to hospitals - which are often seen as more trustworthy, even for routine care.

This contrasts with healthcare systems in the US and much of Europe, where most patients begin with a local primary care doctor / GP, who decides whether hospital or specialist care is necessary. In those systems, it is uncommon to access hospital outpatient care for routine issues without a referral.

China has half the GPs per capita of the US, and patients routinely skip them anyway. As a result, 48% of visits happen at hospitals, compared to 18% in the US.

The Prescription: Enter the AI Doctors

OpenAI and Anthropic

OpenAI and Anthropic are building different solutions for different slices of the American healthcare crisis.

ChatGPT Health is patient-facing, and seems to initially be tackling fragmentation. It connects to patient portals like MyChart and wellness apps like Apple Health, letting users ask questions about their lab results or get plain-language explanations of medical terms. The portals themselves already let you schedule appointments and pay bills, but only within one hospital system. ChatGPT aggregates across systems, but in doing so becomes read-only. It can help you understand your records but, at least for the moment, it can’t book an appointment or pay a bill.

Anthropic’s Claude for Healthcare is enterprise-facing, providing tools to accelerate administrative workflows for health systems and pharmaceutical companies. For health systems, it connects to the CMS coverage database and medical coding systems, pulls coverage requirements, checks clinical criteria against patient records, and proposes a determination for human review. For pharma, it accelerates clinical documentation. Novo Nordisk, the maker of Ozempic, reports that clinical study report writing time dropped by 90% using Claude. These are real efficiency gains, but Claude is also read-only. It accelerates workflows but can’t execute them.

Between them, OpenAI and Anthropic are addressing real problems: patients struggling to understand their health data, and enterprises drowning in paperwork. But neither changes the underlying system. Without deeper integration - payment infrastructure, doctor networks, integrated pharmacy - they risk remaining a read-only AI layer on top of a fragmented system.

China’s AI Healthcare Landscape

China’s AI healthcare market is crowded. Ping An Good Doctor, backed by one of China’s largest insurers, has over 400 million registered users and has been around for a decade. JD Health, the healthcare arm of e-commerce giant JD.com, serves 172 million annual active users and recently launched over 1,000 AI doctor specialists through its Jingyi AI platform. Tencent Health reaches 95 million monthly users through WeChat, connecting them to 38,000 medical institutions. Baidu Health leverages the search giant’s AI capabilities across 360,000 doctor services. These are all serious players building real products.

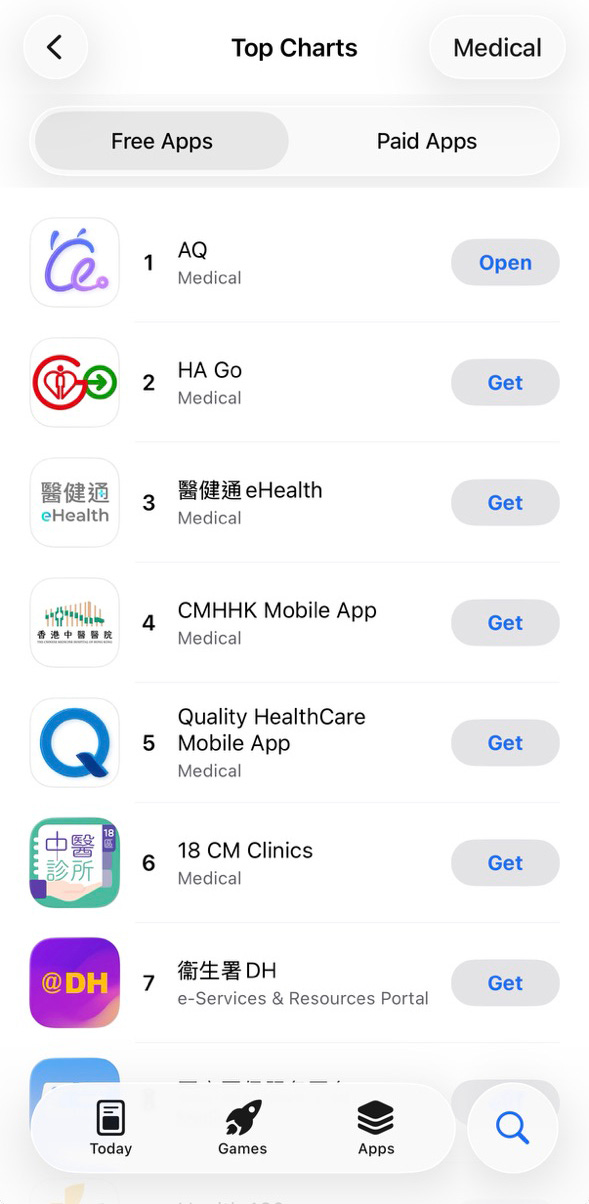

And then there’s AQ (阿福). Ant Group launched it as a standalone app in June 2025. It hit 15 million monthly active users by December, then doubled to 30 million in January following a rebrand and feature upgrades. China Daily called it “China’s largest AI healthcare app.”

I’ll focus on AQ for three reasons.

First, it’s AI-native.

The other platforms predate generative AI. They’re telemedicine services, e-commerce platforms, or search products that added AI capabilities on top of existing businesses. AQ launched in June 2025 as a generative AI product from the start. When AI is the product rather than a feature, you can build around what agents actually need (proactive interventions, multimodal input, voice-first interfaces for elderly users) instead of retrofitting it into legacy UX.

Second, architecture.

Tencent Health runs as a WeChat Mini Program, which grants access to 1.3 billion users but imposes technical constraints. Mini Programs can’t reliably send proactive push notifications. A diabetes management agent needs to nudge “check your glucose” at 8am whether or not the user opened the app yesterday. Inside WeChat, the AI can only speak when spoken to.

AQ uses Alipay’s infrastructure (identity verification, payment rails, user acquisition) but runs as a standalone native application. This allows it to deploy heavy-compute AI agents, integrate with Apple Health and Huawei wearables at the OS level, and own the notification layer for proactive health interventions. This is important for an AI that’s supposed to actively manage your health, not just answer questions.

Third, international potential.

The other platforms are bounded by domestic infrastructure: PAGD’s insurance business, JD’s pharmacy logistics, Tencent’s WeChat ecosystem. AQ has already proven its AI can travel - launching in Hong Kong and Macau in late 2025. The international version is currently Q&A only; full-stack integration with Alipay hasn’t arrived yet. But there’s precedent: in July 2025, Ant launched “Voyager,” an AI travel agent embedded directly in partner wallets like GCash and TrueMoney across Southeast Asia. AQ could follow the same path. For readers watching the AI healthcare race from outside China, Ant is the player to watch.

Anatomy of an Integrated Model

The difference between answering a health question and acting on it is infrastructure. But infrastructure alone isn’t the moat since OpenAI could partner with Stripe for payments or Epic for records. The real advantage comes from owning the entire patient journey and learning from it.

Outcome data, not just symptom data.

Most healthcare AI trains on medical literature or anonymized records, but Ant processes 70% of China’s medical payments, according to CTO He Zhengyu, which means they see the full arc: symptom, diagnosis, treatment, payment, follow-up, outcome. ChatGPT can suggest what might be wrong, but it never learns whether its advice actually helped because the patient leaves to book and pay elsewhere. Ant’s DiagAgent, trained on this closed-loop data, showed a 15% improvement in diagnostic accuracy over models like GPT-4o in end-to-end clinical simulations.

Cross-system visibility.

Chinese hospitals don’t share data well with each other, but AQ connects to over 5,000 hospitals and 300,000 doctors, allowing patients to upload and consolidate records from multiple providers in one place. In the US, Epic only sees Epic hospitals, and even with partnerships, each system stays siloed.

Physical presence.

In March 2025, Ant unveiled on-premises “All-in-One Large Model Machines“ built with Huawei and Alibaba Cloud, now deployed in seven leading hospitals including Shanghai Renji and Zhejiang Provincial People’s Hospital, running behind hospital firewalls to solve data sovereignty concerns that cloud-based AI can’t address. Once installed, switching costs are high, and hospitals become co-developers rather than just customers.

None of this was built overnight.

The DL on AQ

Ant Group’s healthcare play grew out of their payments infrastructure. I’ve written about their broader evolution from fintech to tech giant here:

But they’ve been in healthcare longer than most realize. Hospital appointment booking in 2014, China’s first online medical insurance payouts in 2019, an AI assistant handling 50 million interactions in Zhejiang by 2023. A decade of building payment rails, insurance integrations, and hospital connections before generative AI arrived.

This is in line with their broader strategy of democratization. The same logic behind their AI credit scoring for unbanked farmers and digital insurance for first-time policyholders. AI for inclusion is part of their core mission.

AQ sits at the front of the healthcare system for questions that don’t need a doctor, and handles the entire flow when they do.

The product has three layers:

Health Q&A lets users ask questions in natural language and analyze photos of, e.g. skin conditions or test reports.

AI Health Companion tracks health goals, integrates with wearables from Apple and Huawei, and lets family members monitor elderly parents remotely.

Integrated Services connects users to 300,000 doctors for online consultations, books appointments at 5,000+ hospitals, processes payments, and gets instant insurance claims through China’s medical insurance e-certificate via Alipay (700 million users), all without leaving the app.

But the most interesting feature is the AI Doctor Agents. Over 500 physicians have built digital replicas using Ant’s AI Doctor Agent platform, each trained on that doctor’s consultation patterns, diagnostic approach, and communication style. The doctors own these agents; Ant provides the technology.

Some doctors have even contributed voice recordings so their agent can respond in their actual voice. For elderly users in lower-tier cities who struggle with typing, this voice-to-voice interaction has proven especially popular. It also solves a common family frustration: aging parents often dismiss health advice from their children but will listen to a doctor. An AI that speaks in a trusted physician’s voice carries authority that a generic chatbot doesn’t. In a phone call-like UI, you describe your symptoms out loud, and a nationally recognized specialist answers in their own voice. These AI Doctor Agents answered 27 million health inquiries in 2025.

Early results from OpenAI and Anthropic have been promising, but the published examples focus mostly on administrative efficiency: faster documentation, streamlined workflows e.g. Novo Nordisk. Patient-facing outcomes at scale are harder to find. Here’s a striking one from AQ:

From 10,000 Patients to 3.68 Million

Mao Hongjing is the Deputy Director of Hangzhou Seventh People’s Hospital and a nationally recognized sleep specialist. Before AQ, he could treat roughly 10,000 patients per year in person.

Ant built an AI Doctor Agent based on his clinical approach:

Trained on 100 hours of his patient conversations

His diagnosis records

Relevant medical literature in his specialty

The results, according to Ant:

3.68 million users in its first year

Platform-wide: 500+ AI Doctor Agents have collectively answered 27 million health inquiries

Dr. Mao isn’t paid per AI consultation, but he gains reach, research data, and the ability to focus his in-person time on complex cases. Patients who would have waited hours for reassurance now get it instantly, without clogging the system.

The Global Picture

The US and China are building healthcare AI for different problems. OpenAI is going after patients with ChatGPT Health, while Anthropic is focused on enterprises - selling to hospitals and pharma. But both Western players are read-only: they help you understand information or speed up workflows, without the transactional layer to actually book, pay, or deliver. The Chinese approach centers on the patient too, but with full-stack execution: answer questions at scale, triage before the system gets involved, route people to the right level of care, and handle everything that comes after.

While OpenAI and Anthropic remain US-focused, Ant is moving the other direction. AQ launched in English in Hong Kong and Macau in December 2025, reaching #1 in the App Store’s free medical category. The international version currently offers Health Q&A only - integrated booking and payments may follow.

Where the Models Could Travel

Not every market looks like the US, and not every market looks like China. But most lean one way or the other.

Southeast Asia shares China's structural challenges: fragmented hospitals, weak primary care, large rural populations, smartphone adoption outpacing healthcare infrastructure. The region's healthcare delivery market is $71 billion and growing 15% annually. Indonesia, the Philippines, and Vietnam all have physician densities below 1 per 1,000. Ant's Alipay+ already operates here.

Africa presents the starkest version of these structural challenges. Most countries have fewer than 0.5 doctors per 1,000 people, making it the most physician-constrained region globally. Yet mobile infrastructure is advancing rapidly: M-Pesa demonstrated populations can leapfrog traditional systems, and smartphone penetration continues to climb. No dominant healthcare platform has emerged. The structural dynamics resemble what enabled China's integrated health solutions.

Southern Europe is aging faster than its healthcare systems can adapt. Italy, Spain, Portugal, and Greece have universal coverage but long wait times. The enterprise-first approach of OpenAI and Anthropic might fit better here, assuming they can navigate EU AI Act compliance.

Latin America is mixed. Brazil and Mexico have overwhelmed public systems alongside private systems for the wealthy. Mobile penetration is high, trust in institutions is low, out-of-pocket spending is significant. A consumer-facing health app could find traction but would need local partnerships.

What This Means for Builders

OpenAI and Anthropic have the models but not the infrastructure. Ant has the infrastructure but not the healthcare brand (yet) outside China. That gap is the opportunity.

If you’re building in Southeast Asia, Latin America, or Southern Europe, the playbook isn’t competing with frontier models but building the connective tissue they’ll need when they arrive: payment integrations with local insurers, record aggregation across fragmented hospital systems, pharmacy delivery networks, insurance claim APIs. The unsexy stuff that takes years of local relationships to get right.

The exit path is clear: OpenAI and Anthropic are signing enterprise deals but have no consumer infrastructure internationally and have already begun investing and acquiring. The startups that own the patient journey in their region, even without a frontier model, become strategic assets.

Europe is particularly interesting. OpenAI excluded it from ChatGPT Health at launch. Anthropic is US-only. The EU AI Act creates compliance overhead that US giants may prefer to outsource. Startups that have already navigated GDPR and built hospital integrations become obvious partners or acquisition targets. Jutro Medical (Warsaw, €36M raised) and XUND (Vienna, €6M raised) are building exactly this.

Southeast Asia has similar dynamics. Halodoc (Indonesia, $135M raised) has built the full stack: 20,000 doctors, 3,300 hospitals, 4,900 pharmacies. Jio Health (Vietnam, $20M raised) is building smart clinics and an omni-channel ecosystem. VinBrain built AI diagnostics in Vietnam and was acquired by NVIDIA in December 2024 (terms undisclosed, but Vingroup had invested $126M prior). These are the companies building the pipes before the giants arrive.

Conclusion

OpenAI and Anthropic have the best models but not the pipes. ChatGPT can help you understand your lab results, but it can’t book the follow-up, pay the bill, or get your prescription filled. Ant has both: a decade of healthcare infrastructure and now AQ on top, serving 30 million monthly active users who can go from question to diagnosis to payment to prescription without leaving the app.

The US market will be fought over by OpenAI and Anthropic, and they’re well-positioned for a $5 trillion market where they understand the regulatory landscape. But most of the world looks more like China than America: fragmented hospitals, physician shortages, aging populations, and healthcare systems that can’t scale fast enough. For those markets, Ant has structural advantages. Whether they can translate that into brand recognition outside China, and whether OpenAI and Anthropic can build the infrastructure they lack, remains to be seen. For founders building healthcare infrastructure in underserved markets, that gap is the opportunity.