The China Round — May 22, 2026

China's Starship, Breaking Nvidia's Lock on AI Chip Wiring, and Robot Hands for Every Humanoid

The China Round is a weekly report tracking venture and strategic investment activity across China’s core technology sectors: AI, robotics, semiconductors, new energy and materials, aerospace and defense, and frontier tech.

Capital flows trace where talent is concentrating, where production capacity is being built, and which technologies will reach commercial scale first.

The China Round is free, published every Friday, and written for investors, operators, and founders tracking where China’s tech capital is moving and why it matters.

About the author: Dermot McGrath is Irish, based in Shanghai, a decade in China’s tech and investment ecosystem, fluent Mandarin. Co-founded a VC fund scaled to nine-figure AUM. Now running ZenGen Labs, a cross-border strategy studio covering AI, robotics, and deep tech.

The week’s largest disclosed round went to a rocket company, not an AI lab. After StepFun’s $2.5B Pre-IPO absorbed all the attention last week, capital spread wide and the most interesting deals turned up in the gaps: a Starship-architecture rocket in aerospace, a chip company building China’s answer to Nvidia’s NVLink, and a quantum computing angel round with SMIC’s foundry arm at the table.

Where the Money Went

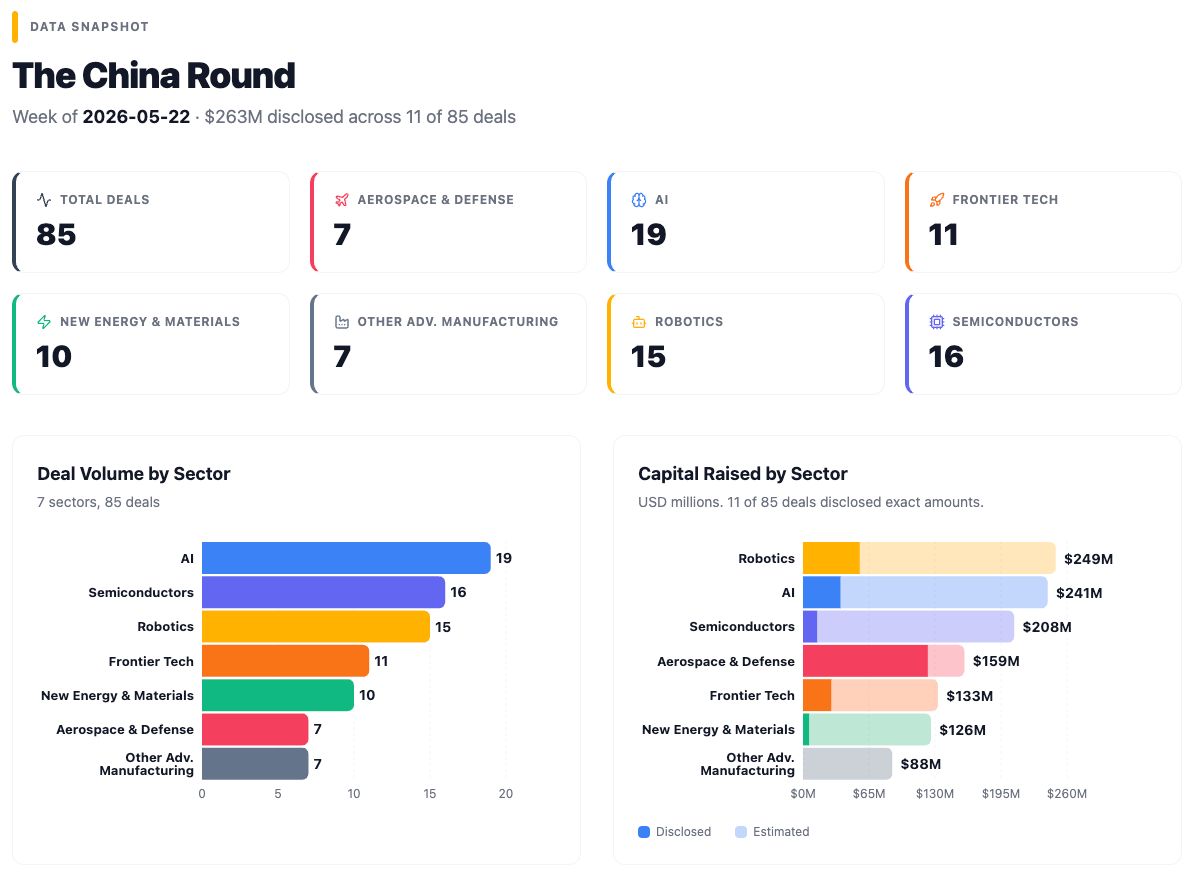

85 deals across seven sectors. 11 disclosed exact amounts totaling $263M (~¥1.9B). Aerospace, which recorded zero deals last week, came back with the week’s biggest disclosed round at ¥500M (~$69M). The stage distribution continues the 2026 barbell: seed and angel bets at one end, a handful of larger rounds at the other, and a thin middle where Series A and B capital would normally concentrate.

🧠 AI (19 deals)

The deals cluster around infrastructure: the systems that sit between raw GPU hardware and the AI models that consume it. OriginFlow (渊澈太初) raised hundreds of millions of RMB at Pre-A for electromyography data infrastructure, capturing the electrical signals from human muscles to train robots to replicate dexterous hand movements. Approaching.AI (趋境科技) raised at a similar scale for the compute-management layer that sits between raw GPU clusters and the AI companies that rent them, scheduling which jobs run on which chips, at what priority, and at what cost. The company claims to process over a trillion tokens per day for customers including Zhipu and Kimi. DeepCybo (深度机智) raised hundreds of millions at Pre-A for PhysBrain, a system that trains robots by watching video of humans performing tasks rather than requiring expensive real-robot training data. HiDream.ai (智象未来) completed a double close, Series B and B+, reportedly with Hefei government funds backing the company across both rounds.

⚡ New Energy & Materials (10 deals)

International stories dominate. Zendure (征拓), covered in Spotlight below, raised a Series B for home energy storage systems already selling across Europe. Yanhe Solar (炎和科技) raised a Series A+ for thin, flexible perovskite solar cells, a next-generation solar technology that works in low light and can be embedded directly into consumer electronics. Yanhe Solar’s cells are already shipping to Lenovo, Signify (the company behind Philips lighting), and Dreame across more than 50 countries. Shanghai Energy Bridge (能量桥) raised at Pre-A for superconducting power distribution, a technology that transmits electricity with near-zero resistance, targeted at AI data centers where power delivery is becoming the binding constraint on how many GPUs you can run.

🔬 Semiconductors (16 deals)

The largest sector by deal count after AI. Tanwei Chiplink (探微芯联), covered in Spotlight, raised hundreds of millions at Pre-A for GPU interconnect chips. WingSemitech (隼瞻科技) raised close to ¥100M (~$14M) at angel for a chip design platform built on RISC-V, the open-source processor architecture that Chinese companies can use without licensing from any American company. Shenzhen Rayhertz Technology (镭赫技术) raised a Series A for semiconductor inspection equipment, the tools that scan chips during manufacturing to catch defects. Four angel-stage semiconductor deals reflect continued seed-level capital formation across the supply chain, from materials to packaging to sensors.

🤖 Robotics (15 deals)

Components and platforms over complete robots. AGILINK (临界点), covered in Spotlight, raised at A+ for dexterous robot hands that supply multiple humanoid manufacturers. Botshare (擎天租) raised at A+ for a platform that rents industrial and service robots by the month rather than requiring factories and warehouses to buy them outright, valued at ¥7B (~$972M), reportedly five months after founding. SEAHI Robotics (世航智能) raised at A+ for maritime robots that clean ship hulls and inspect underwater infrastructure, with the Ministry of Industry and Information Technology’s National SME Development Fund classifying the company as strategic technology. RoboParty (萝博派对), reportedly founded by a 21-year-old, raised tens of millions of dollars at angel for an open-source humanoid robot with Xiaomi backing across multiple rounds.

💡 Frontier Tech (11 deals)

Three brain-computer interface companies raised in this week’s data. See The Bigger Picture below. Juliang Guangqi (矩量光启), covered in Spotlight, raised ¥200M (~$28M) at angel for superconducting quantum computing. NeuraInsight raised a Series A from MiraclePlus (奇绩创坛), the Y Combinator-affiliated accelerator, for a structured database of neuroscience research and brain-activity data used by AI labs studying how biological intelligence works. Three synthetic biology deals covered companies engineering microbes to produce proteins, nutrients, and specialty chemicals through fermentation, an industrial process that can replace petroleum-derived ingredients in food, cosmetics, and materials with bio-manufactured alternatives.

🚀 Aerospace & Defense (7 deals)

Back from zero deals last week. Astronstone (宇石空间), covered in Spotlight, raised ¥500M (~$69M) at Series A for a reusable rocket, the week’s largest disclosed round. TransFuture Aviation (华羽先翔) raised hundreds of millions at Pre-A for an electric vertical-takeoff aircraft, with Ant Group leading what is reportedly its first investment in the eVTOL sector. Beijing Interstellar Development (星际开发) raised a Series A for a reusable orbital cargo vehicle, eight years after founding and still without a first flight.

⚙️ Other Advanced Manufacturing (7 deals)

No single thread across seven deals spanning optical eyewear, 3D printing materials, water treatment membranes, and networking equipment. Shenzhen Zhongjian Technology (众见科技) raised tens of millions at Series A for optical eyewear, backed by SEE Fund and AfterShokz (the bone-conduction headphone company).

Spotlight

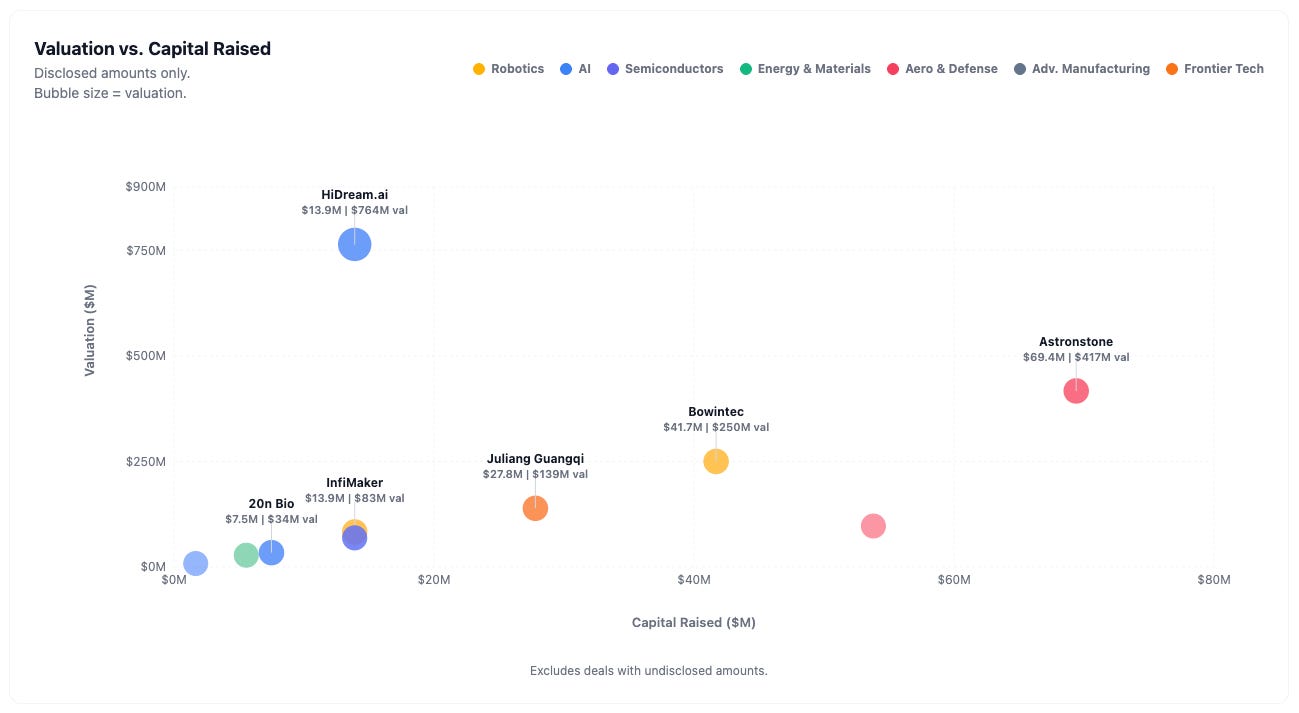

Astronstone (宇石空间)

Series A, ¥500M (~$69M), ¥3B (~$417M) valuation

The engineer who helped build China’s heaviest operational rockets is now building a private Starship analog with chopstick catch.

Astronstone is the second chopstick-recovery rocket company we’ve covered in three weeks. In the May 2 edition of The China Round, we spotlighted Cosmoleap (大航跃迁), which raised ¥500M (~$69M) at Series A for a 70-meter, 18-ton-to-LEO vehicle with tower-catch testing underway since November 2024. Now Astronstone has raised the same amount, at the same stage, for the same core architecture: stainless steel airframe, liquid oxygen and methane propellant, and tower-based chopstick recovery. Both target first flight in 2027. Two companies raising ¥500M Series A rounds within three weeks for the same technical approach is a signal that Chinese investors see the Starship architecture as proven enough to back with scale capital, not just one contrarian bet.

The architecture matters because each element solves a specific cost problem. Stainless steel is heavier than carbon fiber but dramatically cheaper to manufacture and more tolerant of the extreme temperatures during reentry. Methane burns cleaner than kerosene, reducing engine refurbishment between flights. Chopstick tower recovery, catching the returning booster with mechanical arms rather than landing it on legs, eliminates the weight penalty of landing gear. The combination makes rockets cheap enough to treat as reusable infrastructure rather than expendable hardware. What distinguishes Astronstone is the founder. Tang Wen (唐文) holds a PhD in aerospace engineering from Tsinghua University and spent years at the First Academy of China Aerospace Science and Technology Corporation (CASC), where he worked on propulsion and structural systems for the CZ-5 and CZ-7 launch vehicles. The CZ-5 is China’s heaviest operational rocket. The CZ-7 is the cargo workhorse that supplies China’s space station. Tang’s experience is in the specific engineering discipline, liquid rocket propulsion and structures, that a Starship-class vehicle demands. The company has raised ¥1B (~$139M) across four rounds in one year, with first flight targeted for the first half of 2027. Landspace (蓝箭航天), currently the furthest ahead among Chinese reusable rocket startups, flew its Zhuque-3 on a test mission in late 2025. SpaceX filed its S-1 on May 20 and is set to list in June at a reported valuation of $1.5 trillion to $2 trillion, the largest IPO in history. Two Chinese companies raising ¥500M each for the same core architecture in the same month that SpaceX prices its public offering leaves little ambiguity about where the technology stands.

Investors: Kunlun Capital (昆仑资本, co-lead), Gaorong Capital (高榕创投, co-lead), and 11 others including Xingxiang Capital (兴湘资本).

Tanwei Chiplink (探微芯联)

Pre-A, hundreds of millions RMB, ¥1.5B (~$208M) valuation

One of the first Chinese companies building a clean-room alternative to the high-speed links that let Nvidia’s GPUs talk to each other inside AI training clusters.

Tanwei Chiplink builds GPU interconnect chips. When companies train large AI models, they connect thousands of GPUs into a single cluster where each chip needs to communicate with every other at extreme speed. Nvidia dominates this layer through NVLink (the chip-to-chip protocol) and NVSwitch (the switching chip that routes traffic between GPUs), creating a lock-in that goes beyond the GPU itself. Even if a Chinese company builds a competitive AI processor, it still needs the high-speed fabric to connect them. Tanwei’s products, ACCLink and ACCSwitch, target this gap directly: the protocol IP delivers 50-nanosecond latency, fast enough that thousands of chips can coordinate without creating a bottleneck, and can scale to clusters of 4,096 GPUs, large enough to train frontier AI models. The team spun out of Tsinghua University’s Brain-Inspired Computing Research Center.

Inspur Information (浪潮信息), China’s largest AI server manufacturer, invested strategically, a real customer pulling the technology into its server product line. Inspur’s own statement cited “cooperation prospects on smart computing product lines” and noted that Tanwei’s product planning “benchmarks Nvidia’s NVLink+NVSwitch.” Three Beijing government funds, Capital Technology Development Group (首都科技发展集团), Zhongguancun Science City (中关村科学城), and Guozhong Capital (国中资本), all participated, treating GPU interconnect as AI sovereignty infrastructure. Tanwei is not alone in this race: Rongxin Zhiyuan (容芯致远) raised a separate angel round the same week for optical interconnect targeting the same layer, and Hygon (海光信息) published an open interconnect standard last year. But Tanwei is among the first dedicated pure-play chip companies attacking the problem, and Inspur’s strategic investment suggests real engineering engagement behind the capital.

Investors: ShenJing Jiacheng (盛景嘉成, lead), Zhengxuan Investment (正轩投资), Inspur Information (浪潮信息, strategic), iSoftStone (软通动力, strategic), Huagai Capital (华盖资本), Fengnian Capital (丰年资本), Capital Technology Development Group (首都科技发展集团), Zhongguancun Science City (中关村科学城), Guozhong Capital (国中资本), Jinpu Investment (金浦投资), and others.

Zendure (征拓)

Series B, hundreds of millions RMB, ¥1.5B (~$208M) valuation

A Chinese home energy company ranked first in France and first among independent brands in Germany.

Zendure builds home energy management systems, the hardware and software that let households store solar energy, sell electricity back to the grid during peak pricing, and manage their home’s power consumption automatically. According to company figures, Zendure ranks first in France by total energy storage sales, first among independent brands in Germany, and top three in the Netherlands. Per company, revenue has grown approximately 200% year over year. The company launched PowerHub in Dusseldorf on May 11, a plug-in hub that connects rooftop solar, battery storage, and household loads into one managed system, with shipping starting July 2026. Its ZenWave subscription service automatically buys electricity when wholesale prices drop and sells stored energy back when prices spike.

The round was co-led by Han’s Laser (大族激光), a Shenzhen-listed industrial laser and precision manufacturing company with a market cap exceeding ¥100B (~$14B), alongside DeLink Capital (德联资本). A strategic investment from a laser manufacturer points toward supply chain and hardware production cooperation.

The structural tailwind is European electricity volatility. Wholesale electricity prices rose across the EU in 2025, with widening intraday spreads between solar-generation midday and peak evening demand. That price gap is what residential storage monetizes, and Zendure’s software automates the arbitrage. The EU deployed 27.1 GWh of new battery storage in 2025, a 45% increase and the twelfth consecutive record year, yet over 90% of EU battery manufacturing capacity targets EVs, leaving residential storage largely open to Chinese manufacturers.

Investors: Han’s Laser (大族激光, co-lead), DeLink Capital (德联资本, co-lead).

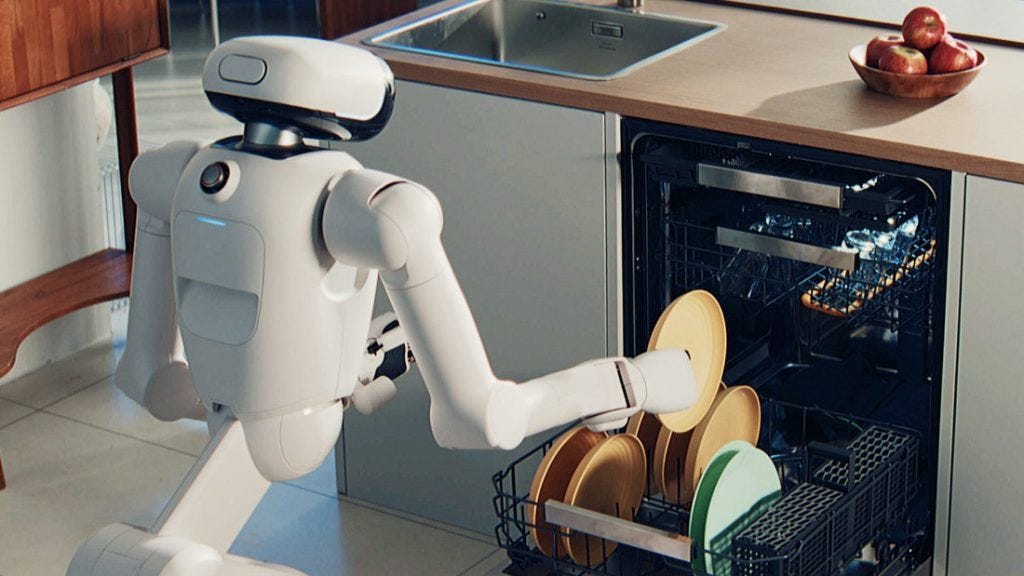

AGILINK (临界点)

Series A+, hundreds of millions RMB, ¥8B (~$1.1B) valuation

The company that makes the hands for China’s humanoid robots raised three rounds in 28 days and landed an LG design win at CES.

AGILINK makes dexterous robot hands, the multi-fingered grippers that allow humanoid robots to pick up objects, turn handles, and perform the kind of manipulation tasks that fixed industrial grippers cannot. The company was spun off from AgiBot (智元机器人) in January 2026, inheriting AgiBot’s existing hand product line and the engineering team behind it. The products it inherited and continues to produce include the OmniHand series: the OmniHand (10 active degrees of freedom, ¥9,800 or ~$1,360), the OmniHand Touch (10 degrees of freedom with tactile sensing, ¥14,800 or ~$2,060), and the OmniHand Pro (12 degrees of freedom). The company shipped thousands of units per quarter in 2025, per its fundraising materials. At CES 2026, LG’s first humanoid robot, CLOiD, used AGILINK’s hands as its core manipulation hardware, a design win that validated the “sell to every body maker” strategy.

AGILINK completed three rounds in 28 days, from founding on January 14 to closing its Series A on February 11. Better to bet on the hands that go into every humanoid robot than to pick a single body maker. As the humanoid sector matures, the market is pricing the component layer, the parts every robot needs, higher than many of the robot makers themselves. AGILINK is not the only company investors are backing at this layer. LinkerBot (灵心巧手), covered in the May 2 edition, has shipped over 10,000 dexterous hands and raised seven rounds in 18 months at a valuation above ¥15B (~$2.1B). The logic behind spinning out hands as an independent company is that humanoid robot makers are competing fiercely on price and form factor, and most will not survive the shakeout. But every survivor needs hands. A standalone hand company can sell to all of them without being locked to one body maker’s fate, and investors can back the category without picking a winner. AGILINK at ¥8B and LinkerBot at ¥15B+ both sit above multiple humanoid body companies that are their customers. The A+ round, recorded in mid-May, was not accompanied by a public announcement. The Series A in February was led by a major internet company, with co-investors including Baidu Ventures (百度风投), Yunfeng Capital (云锋基金), Synstellation Capital, and Joyson Electronics (均胜电子).

Investors (Series A, Feb 2026): Major internet company (lead, unnamed), Baidu Ventures (百度风投), Yunfeng Capital (云锋基金), Synstellation Capital, Joyson Electronics (均胜电子), and others.

Announcement (Series A, Feb 2026)

Juliang Guangqi (矩量光启)

Angel, ¥200M (~$28M), ¥1B (~$139M) valuation

A quantum computing startup raised one of China’s largest angel rounds with a semiconductor foundry’s venture arm at the table, and a team forged at Sandia National Laboratories.

Juliang Guangqi is building a full-stack superconducting quantum computer: not just the quantum processor chip but the entire system, including cryogenic control hardware that cools circuits to near absolute zero, error-correction algorithms that compensate for the fragility of quantum states, and a quantum operating system. Founded in mid-2025 by Yu Wenlong (于文龙), who holds a physics PhD from Georgia Tech and an applied physics degree from the University of Science and Technology of China (USTC), with post-doctoral work at Sandia National Laboratories, one of the US Department of Energy’s premier weapons and technology research facilities. A co-founder reportedly worked at NIST, the US National Institute of Standards and Technology, on superconducting chip processes. The company claims to have completed China’s first quantum chip produced on an 8-inch industrial wafer, the standard disk size used in high-volume semiconductor factories, a manufacturing milestone marking the shift from lab-built prototypes to factory-scale production.

¥200M (~$28M) is an unusually large angel round for quantum computing, a field where most Chinese startups raise single-digit millions at seed stage. The investor that matters most is SMIC Capital (中芯聚源), the venture arm of Semiconductor Manufacturing International Corporation, China’s most advanced chip foundry. Quantum computing chips require sophisticated semiconductor fabrication, and having the foundry’s own investment arm at the table opens a potential path to manufacturing access. The deal has drawn comparisons in Chinese press to a “Fairchild moment”, a reference to Fairchild Semiconductor, the 1957 startup whose manufacturing innovations became the fabrication backbone that other companies built on. The analogy is specifically about foundry access: the argument is that Juliang Guangqi’s SMIC-aligned quantum chip process could become the manufacturing standard other Chinese quantum companies depend on. It is an ambitious claim for a company less than a year old, but the combination of US national laboratory experience, Chinese university pedigree, and foundry alignment is the kind of team composition that makes investors pay up early.

Investors: Junshan Capital (钧山资本, co-lead), Heli Capital (和利资本, co-lead), SMIC Capital (中芯聚源), Yixin Investment (翌昕投资), Yirong Capital (翊荣资本), Qiancheng Capital (千乘资本), Detong Capital (德同资本).

Also on the Radar

Botshare (擎天租). Series A+, hundreds of millions RMB, ¥7B (~$972M) valuation. A robot rental platform that sells access to industrial and service robots by the month rather than requiring factories and warehouses to buy them outright. Previously featured in the May 2 edition at Pre-Series A and ¥4.2B (~$580M) valuation with four rounds in 105 days. Now at ¥7B and reportedly six rounds since December 2025. The company reportedly launched an international rental platform in 13 countries in April 2026, with overseas rental prices reportedly running six times the domestic rate.

Yanhe Solar (炎和科技). Series A+, hundreds of millions RMB, ¥1B (~$139M) valuation. Thin, flexible perovskite solar cells that work indoors at low light levels, embedded into consumer electronics rather than competing with rooftop solar panels. Products shipping in 50+ countries across 100+ brand supply chains, including Lenovo, Signify, and Dreame. CES 2026 showcase included solar-powered e-paper displays, smart glasses, and cameras. A 100MW production line has been operational in Changde, Hunan since August 2025.

HiDream.ai (智象未来). Series B+, ¥100M (~$14M), ¥5.5B (~$764M) valuation. An image generation model, the kind of AI that creates pictures from text descriptions, large enough to compete with Midjourney and DALL-E. A Series B followed by a B+ in close succession, reportedly with Hefei government funds across both rounds. Per company materials, over one million monthly global users.

TransFuture Aviation (华羽先翔). Pre-A, hundreds of millions RMB, ¥1.5B (~$208M) valuation. Electric vertical-takeoff aircraft. Ant Group (蚂蚁集团) led the round, reportedly its first eVTOL investment. A fintech company with no prior aerospace history moving into air mobility suggests the sector is being repriced from deep-tech moonshot to near-term infrastructure play. Investors: Ant Group (蚂蚁集团, lead), Fosun Venture (复星创富), Bian’an Shidai (彼岸时代).

SEAHI Robotics (世航智能). Series A+, undisclosed amount, ¥3.5B (~$486M) valuation. Maritime robots for ship hull cleaning and underwater inspection. Previously featured in the May 2 edition with simultaneous A+ and A++ rounds and proprietary thrusters rated for 10,000 operational hours versus a 300-400 hour industry standard. The National SME Development Fund, a MIIT-backed policy instrument, entered this round. Investors: GSR Ventures (金沙江创投), Shanghe Dynamics (上河动量), Vertex Ventures (祥峰投资), and others.

OriginFlow (渊澈太初). Pre-A, hundreds of millions RMB, ¥1.5B (~$208M) valuation. Electromyography data infrastructure for training robot manipulation. The company captures electrical signals from human muscles during tasks like grasping and assembly, then converts those signals into training data for robot arms and hands. Investors: BlueRun Ventures (蓝驰创投), Vitalbridge (绿洲资本), and seven others.

RoboParty (萝博派对). Angel, tens of millions USD (~¥144M+), ¥1.95B (~$271M) valuation. Open-source humanoid robot. The founder is reportedly 21 years old. Xiaomi (小米) has reportedly backed the company across multiple rounds. Over $40M (~¥288M) raised pre-revenue for a company whose strategy is to publish its robot design openly, letting a global developer community build applications on top and train the robot’s AI with real-world footage from thousands of users. Investors: Shunwei Capital (顺为资本, lead), Xiaomi Group (小米集团).

DeepCybo (深度机智). Pre-A, hundreds of millions RMB, ¥1.5B (~$208M) valuation. PhysBrain 1.0, a system that trains robots from egocentric human video, meaning the robot learns by watching footage shot from a person’s perspective rather than requiring expensive real-robot demonstrations. Reportedly three rounds in three months and heavily oversubscribed. Investors: Zhongguancun Development Group (中关村发展集团), Puhua Capital (普华资本), Oriental Fortune Ocean (东方富海), and others.

InfiMaker (无限工坊). Series A, close to ¥100M (~$14M), ¥600M (~$83M) valuation. Consumer desktop CNC machines, the kind of precision cutting and carving tools that let hobbyists and small manufacturers work with wood, metal, and plastic at home. The founding team are reportedly DJI alumni. Backed by Meituan (美团) and Kunlun Capital (昆仑资本).

Brainsmart Technology (脑思科技). Angel, tens of millions USD (~¥72M+), ¥325M (~$45M) valuation. Brain-computer interface electrodes and neural decoding systems. One of three BCI companies that raised in this week’s data. See The Bigger Picture. Investors: Kangju Capital (康君资本, co-lead), BlueRun Ventures (蓝驰创投, co-lead), Fosun Health Capital (复健资本).

The Bigger Picture

China Approved the World’s First Commercial Brain Implant, and the Capital Followed

Three brain-computer interface companies raised funding in this week’s data, the downstream effect of a regulatory and policy cascade that compressed months of dealmaking into a sprint.

On March 13, 2026, China’s National Medical Products Administration granted the world’s first commercial approval for an implantable brain-computer interface, a coin-sized wireless electrode array made by Neuracle Medical Technology (神络医疗) that reads signals from the brain’s motor cortex and restores hand movement in paralyzed patients. Two days later, the National Healthcare Security Administration assigned the product an insurance reimbursement code, opening the payment pathway that had blocked hospital adoption. Approval on a Monday, insurance coding by Wednesday. Brain-computer interfaces were reclassified from research bet to healthcare market in a single week.

In August 2025, the Ministry of Industry and Information Technology and six other agencies published a national BCI roadmap targeting major technical breakthroughs by 2027 and a complete domestic supply chain by 2030. In March 2026, the Government Work Report explicitly named BCI as a “future industry” to be cultivated alongside quantum computing and 6G. By Q1 2026, the sector had recorded 17 deals totaling ¥3.8B (~$528M), already exceeding the total deal value for all of 2025 in a single quarter.

The global comparison is instructive. Neuralink has implanted more patients and its N1 chip goes deeper into the brain, using intracortical electrodes that penetrate brain tissue rather than sitting on the surface. Its Blindsight vision-restoration implant received FDA Breakthrough Device designation in 2024. But Neuralink remains in clinical trials with no commercial approval, no insurance pathway, and no hospital distribution channel. China’s NMPA moved first, the investment followed across three companies in one week, and the sector is accelerating.

The Component Layer: When the Picks-and-Shovels Companies Outprice the Miners

When you don’t know which gold miner will strike it rich, sell shovels. That logic is playing out across this week’s data in both robotics and AI infrastructure, and the market is pricing the shovel companies aggressively.

AGILINK makes the dexterous hands that go into humanoid robots from multiple manufacturers. Tanwei Chiplink builds the interconnect chips that let GPUs communicate inside AI training clusters. OriginFlow captures electrical signals from human muscles and converts them into training data for robot arms. Three companies, three different technical layers, one shared positioning: they supply critical components to an entire category rather than competing as a finished product.

AGILINK, shipping thousands of hands per quarter with an LG design win at CES, commands a ¥8B (~$1.1B) valuation. That sits above multiple humanoid robot body companies that are its customers. The logic is straightforward: if five humanoid makers each capture 20% of the market, a component supplier embedded across all five captures 100%. AGILINK’s CES partnership with LG proves the strategy works internationally, not just within China’s robotics supply chain.

Tanwei Chiplink applies the same logic one layer deeper. Nvidia controls the AI training stack not just through GPUs but through NVLink and NVSwitch, the high-speed interconnect fabric that lets those GPUs coordinate. Chinese AI chip companies can build competitive processors, but without a domestic interconnect layer, every Chinese AI cluster still depends on Nvidia’s communication backbone. Tanwei’s ¥1.5B (~$208M) valuation at Pre-A, with Inspur investing strategically, prices it as AI sovereignty infrastructure.

OriginFlow sits at the data layer. Training a robot to grasp objects, fold towels, or assemble components currently requires either expensive physical demonstrations with real robots, or simulation environments that don’t fully capture how human hands actually move. OriginFlow’s approach, strapping sensors to human arms and recording the electrical signals muscles produce during real tasks, creates a scalable data pipeline that any robotics company can use.

The proto supply chain visible in this week’s data reads: data acquisition (OriginFlow) to compute scheduling (Approaching.AI) to manipulation hardware (AGILINK) to finished robots. Capital is concentrating at each layer independently rather than flowing to vertically integrated robot companies, a pattern that echoes how the smartphone supply chain matured: TSMC, Qualcomm, and Corning became more valuable than most of the phone brands they supplied.

Deal data compiled from Chinese corporate announcements, financial news, and investment databases. Amounts and valuations are as reported and may be incomplete. For informational purposes only. Not investment advice. Verify all figures independently before acting on them.